EU CONSUMER CYCLICALS: Coty: S&P to neg. outlook (x2)

(COTY; Ba1/BBB- Neg/BBB-)

Not much new from S&P. Re. Wella stake (valued at $1b) it still sees Coty committed to divesting it - simply delayed given macroeconomic environment. It is a powerful source of deleveraging powder - against net debt of $3.8b could move leverage -1.1x from current (unadj) low 4-handle (or co reported 3.5x to 2.5x - within its target 2-3x).

It has only been in IG for a year now but has not issued over that span - that is despite having $1.2b coming due in April across a dollar and euro line.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 52W BILL AUCTION: HIGH 3.760%(ALLOT 56.68%)

- US TSY 52W BILL AUCTION: HIGH 3.760%(ALLOT 56.68%)

- US TSY 52W BILL AUCTION: DEALERS TAKE 38.62% OF COMPETITIVES

- US TSY 52W BILL AUCTION: DIRECTS TAKE 4.81% OF COMPETITIVES

- US TSY 52W BILL AUCTION: INDIRECTS TAKE 56.57% OF COMPETITIVES

- US TSY 52W AUCTION: BID/CVR 2.85

FED: US TSY 52W AUCTION: NON-COMP BIDS $1.116 BLN FROM $50.000 BLN TOTAL

- US TSY 52W AUCTION: NON-COMP BIDS $1.116 BLN FROM $50.000 BLN TOTAL

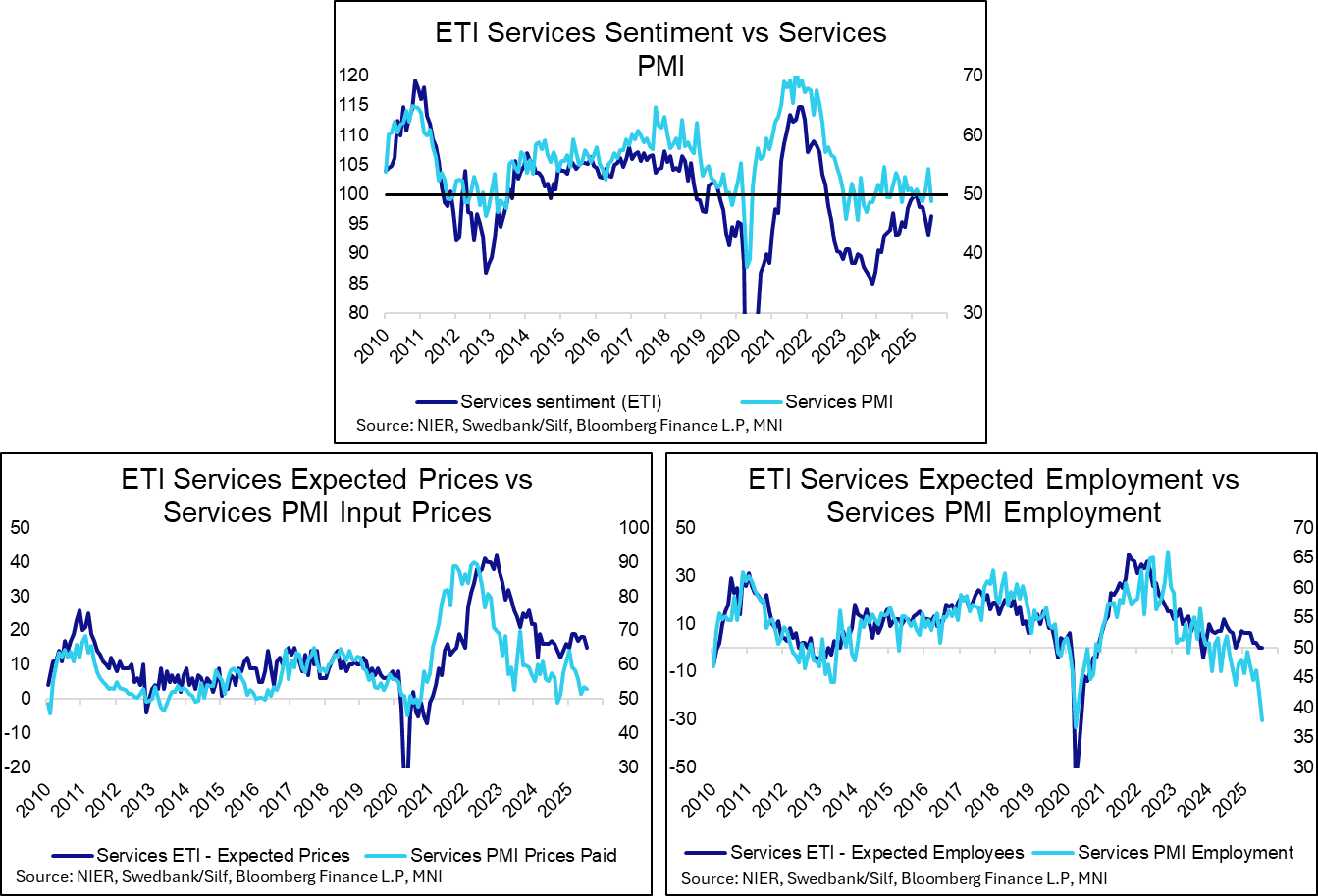

SWEDEN: Weak July Services PMI Keeps An August Rate Cut Possible

This morning’s services PMI was weak, falling 5.5 points to 48.8 – the largest one month drop since April 2020. While less closely followed than the Economic Tendency Indicator, the PMI has still contributed to a 1.6bp fall in 2-year SEK swap rates today.

- Thursday’s flash July CPI report will be key in determining the likelihood of a Riksbank August rate cut. Markets currently price just a 20% implied probability of such a move, but we have noted for several weeks that a cut cannot be ruled out before seeing the inflation data, particularly with activity signals still weak.

- Although new orders (51.5 vs 59.5 prior) and production (50.1 vs 57.3 prior) PMI components remained in expansionary territory in July, the falls relative to June were sharp.

- More alarmingly, the employment component fell to a 5-year low of 37.8 (vs 36.7 prior). The downward trend is more volatile than, but still broadly consistent with, the signal from the Economic Tendency Indicator’s services employment series.