EU CONSUMER CYCLICALS: Coty: 1Q Results

(COTY: Ba1/BBB- Neg/BBB-)

Seeming refusal to disclose Gucci license contribution to earnings makes us somewhat nervous. Reminder no brand >10% of sales but speculation is if it could be a larger contributor on EBIT. On sales it is lagging market by 5-8ppt even on sell-out (i.e. ignoring retailer inventory right sizing actions). Potential asset sales are being lined up to help delever balance sheet - Wella sell-down in particular we would see as credit positive while mass cosmetics and Brazil business would depend on sale multiple achieved.

3m to Sept:

- Sales $1.6b, -8% LFL. Net of FX -6%.

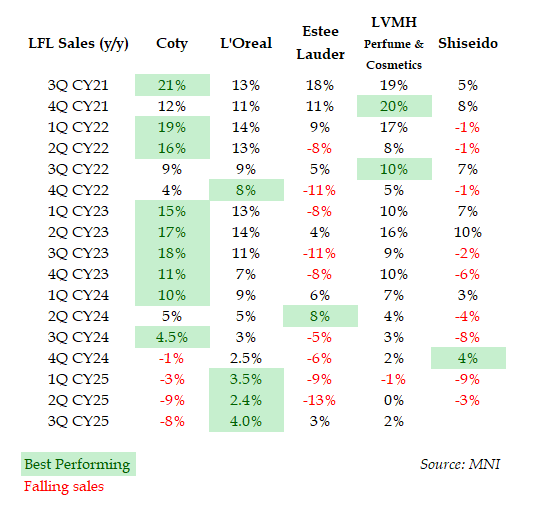

- prestige $1.1b -6% (sell-out +1%, market +6%), consumer $0.5b -11% (sell-out -6%, market +2%)

- Americas $0.65b -6%, EMEA $0.8b -9%, APAC $0.2b -9%

- Notes small China prestige exposure did well; sell-out +15%, >2x market growth

- Gross margin 64.5%, -100bps

- Adj. EBIT $241m, -21% y/y

- Statutory $185m, -22% y/y. Gap on $39m in amortisation and $15m stock compensation, similar to last yr and both non-cash

- Cash flows were similar to last year

- Net debt $4.1b, levered 3.7x vs. 3.4x LY

- The $900m new 31s alongside Q2 FCF will be used to pay down all of this years $1.2b wall

- 25.8% stake in hair-care brand Wella valued at $1b (unch)

- "actively pursuing the monetization of Wella" to delever

On Gucci License and strategic review:

- Would not comment on an analyst asking about a lawsuit filed by Coty against Kering for breach of contract

- On Gucci exposure refused to give more detail outside reiterating no brand makes up >10% of sales and adding that the rest of portfolio (85% of sales) in 7y+, perpetual or owned licenses/brands.

- On strategic review: $400m in sales Brazil business is painted as strong performer and "very profitable" and it implies this will be sold and likely soon. The colour cosmetics side ($1.2b in sales) it wants to attempt to fix earnings before evaluating options.

- reminder the colour cosmetics business may be FCF negative

2Q Guidance largely unch:

- LFL sales now at better end of prev. -3-5% range

- FX tailwind in low to mid-single digit

- 2Q EBITDA down low to mid teens (i.e. -13-16%) (unch)

- 1H FCF > $350m (vs. $411m LY) (unch) (seasonally positive only in 1H)

Continues to expect both to turn to growth in 2H driving:

- $1b in EBITDA (vs. $1.1b LY)

- Leverage at 3.5x (unch y/y)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Pierces Key Resistance

- RES 4: 152.31 High Feb 19

- RES 3: 151.78 2.0% 10-dma envelope

- RES 2: 151.62 61.8% retracement of the Jan 10 - Apr 22 bear leg

- RES 1: 151.21 High Mar 28 & Oct 07

- PRICE: 151.17 @ 16:39 BST Oct 7

- SUP 1: 149.05 Low Oct 6

- SUP 2: 148.10/147.67 20- and 50-day EMA values

- SUP 3: 146.59 Trendline support drawn from the Apr 22 low

- SUP 4: 145.49 Low Sept 17

A bullish theme remains intact in USDJPY following Monday's strong start to the week. The move higher has resulted in a breach of resistance at 149.96, the Sep 26 high and a key short-term resistance. This has exposed the key medium-term resistance at 150.92, the Aug 1 high. It has been pierced, a clear break of it would confirm a resumption of the bull leg that started Apr 22. Monday’s intraday low at 149.05 is first support.

EURGBP TECHS: Monitoring Support At The 50-day EMA

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8769 High Jul 28 and the bull trigger

- RES 1: 0.8751 High Sep 25

- PRICE: 0.8685 @ 16:38 BST Oct 7

- SUP 1: 0.8673/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8633 Low Sep 15

- SUP 3: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 4: 0.8540 Low Jun 30

Short-term weakness in EURGBP appears corrective and the trend condition is bullish. The cross traded lower on Monday. Initial firm support to watch lies at 0.8673, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement. Note that the key trend support lies at 0.8597, the Aug 14 low. A breach of this level would instead reinstate a bearish threat. For bulls, key resistance and the bull trigger is 0.8769, the Jul 28 high.

PIPELINE: Corporate Bond Update: $1.15B TD Synnex 2Pt Launched

$7.85B total to price Tuesday:

- Date $MM Issuer (Priced *, Launch #)

- 10/07 $2.5B *Bank of England 5Y +8a

- 10/07 $1.75B *CPPIB 3Y SOFR+39

- 10/07 $1.75B #Angola $1B +5Y 9.25%, $750M 10Y 10.125%

- 10/07 $1.15B #TD Synnex $550M +3Y +75, $600M 10Y +118

- 10/07 $700M *Türkiye Garanti Bankası 10.5NC5.5 7.625%