GBPUSD TECHS: Corrective Pullback

* RES 4: 1.3726 High Sep 17 and a key resistance * RES 3: 1.3661 High Sep 18 * RES 2: 1.3607 2.764 p...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Bull Flag Formation

- RES 4: 1.3471 High Oct 17

- RES 3: 1.3452 50.0% retracement of the Sep 17 - Nov 4 bear leg

- RES 2: 1.3416 High Oct 21

- RES 1: 1.3385 High Dec 04

- PRICE: 1.3333 @ 16:26 GMT Dec 10

- SUP 1: 1.3268 50-day EMA

- SUP 2: 1.3241 20-day EMA

- SUP 3: 1.3180/25 Low Dec 2 / Low Nov 26

- SUP 4: 1.3038/10 Low Nov 20 / Low Nov 4 & 5 and the bear trigger

The latest pause in GBPUSD appears to be a flag formation - a bullish continuation signal. This reinforces the current uptrend. The breach of the 50-day EMA undermined a recent bearish theme and highlights a stronger reversal. Scope is seen for a climb towards 1.3452, a Fibonacci retracement point. Initial firm support is seen at 1.3241, the 20-day EMA. A move below this average would be a bearish development.

US TSY OPTIONS: BLOCK: Feb'26 10Y Call Spread Buyer

- +10,000 TYG6 112.5/113 call spds, 12 vs. 112-07.5/0.10% at 1312:25ET, another 4,000 on screen.

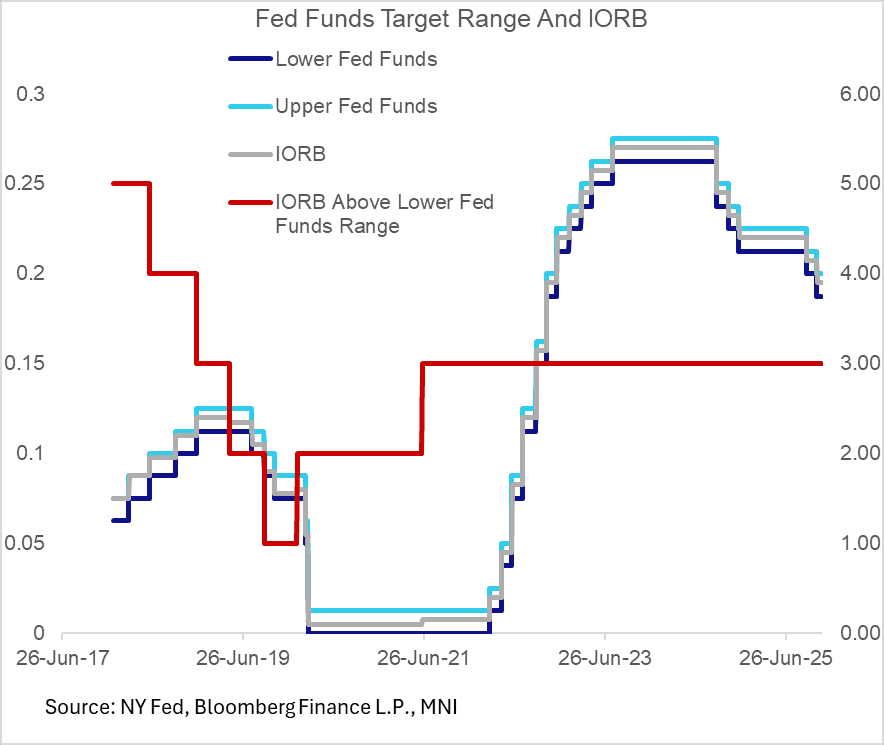

FED: IORB Tweak, Reserve Management Buy Announcement Unlikely - But In Focus

On the administered rates front, there has been increasing speculation that the interest rate paid on reserve balances (IORB) could be lowered relative to other policy rates as soon as today's meeting, with potential temporary market operations (TOMOs) announced alongside.

- The Fed has lowered interest on reserve balances (now called IORB, previously referred to as IOER) relative to the Funds range in previous episodes as it navigated a pullback in reserves. The FOMC ratcheted the administered rate lower by 5bp relative to the policy rate in each of June and Dec 2018, and May and Sep 2019, from 25bp above the lower bound to just 5bp above it, before increasing it again in 2020-21 back to 15bp.

- The FOMC may well have been discussing this change: KC Fed Pres Schmid in November mentioned lowering IORB, a technical adjustment which would see repo rates fall and in theory allow the Fed to hold fewer reserves than it otherwise would: "Another possible action could be to lower the interest rate that the Fed pays on reserves within the target band. Currently this rate is 15 basis points above the bottom of the band. Lowering the rate within the band would allow more space for other interest rates to move before bumping up against the top of the band. This would allow for a greater range of private intermediation of reserve demand before the Fed would feel the need to take action."

- With no mention of such a technical move in the October meeting minutes, however, and no clear signal from Fed leadership, prospects of an IORB change as part of today's decision are seen to have diminished.

- Meanwhile, reserve management purchases (probably in bills) are expected to start in the first half of 2026 as the Fed rebuilds its balance sheet to meet the underlying growth in liability demand. There is some speculation an announcement could be made at this meeting for a January start (BofA: "We expect the Fed to announce reserve management purchases (RMPs) ... for start in Jan at a pace of $45b per month. We are out of consensus early and in size.") but that’s not MNI’s base case.

- On TOMOs being launched particularly to meet year-end pressures, we think the Fed is more inclined to encourage takeup of the standing repo facility - it would be a surprise if they announced something on this front today though if they did Powell would probably emphasize that it's a merely pragmatic move and not indicative of any shift in policy (as with RMPs).

- Whatever's announced today, we hope Powell gets asked on the latest updates on all these fronts at the press conference.