GBPUSD TECHS: Corrective Pullback

- RES 4: 1.3753 High High Jul 2

- RES 3: 1.3681 High Jul 4

- RES 2: 1.3636 76.4% retracement of the Jul 1 - Aug1 downleg

- RES 1: 1.3595 High Aug 14

- PRICE: 1.3465 @ 16:12 BST Aug 20

- SUP 1: 1.3461 Low Aug 20

- SUP 2: 1.3449 50-day EMA

- SUP 3: 1.3400 Low Aug 11

- SUP 4: 1.3346 Low Aug 7

The latest pullback in GBPUSD, for now, appears corrective and a bullish condition remains intact. Recent gains resulted in a breach of resistance at 1.3589, the Jul 24 high. This signals scope for a climb towards 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1. Clearance of this level would strengthen the S/T bull theme. Initial firm support to watch is 1.3449, the 50-day EMA. A clear break of it would signal a possible reversal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Bear Cycle Remains In Play

- RES 4: 1.3835 High Oct 20 2021

- RES 3: 1.3800 Round number resistance

- RES 2: 1.3681/3789 High Jul 04 / 01 and the bull trigger

- RES 1: 1.3519 20-day EMA

- PRICE: 1.3494 @ 17:00 BST Jul 21

- SUP 1: 1.3365 Low Jul 16

- SUP 2: 1.3335 Low May 20

- SUP 3: 1.3245 Low May 19

- SUP 4: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

Prices rallied Monday, prompting GBPUSD to entirely reverse the weakness off Friday highs. This kept the pair clear of any test on recent lows. Nonetheless, last week’s extension lower resulted in a breach of trendline support currently at 1.3470 - drawn from the Jan 13 low. The breach strengthens a bearish threat, exposing 1.3335 next, the May 20 low. On the upside, initial firm resistance to watch is 1.3519, the 20-day EMA. A clear break of this average is required to highlight a potential base.

ECB: Macro Since Last ECB - Labour: Wages Still Expected To Cool

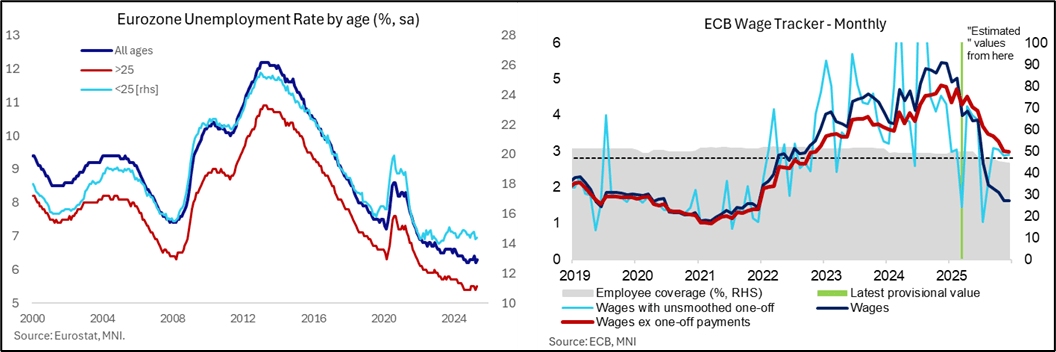

- The unemployment rate was a tenth higher than expected in May at 6.3% as it increased off historical lows of 6.2% in April. It doesn’t change the story, having averaged 6.3% since mid-2024.

- It’s a release that hasn’t been commanding much market attention but President Lagarde has regularly cited this relative resilience of the labour market.

- The more up to date German unemployment rate series from the Bundesbank meanwhile pointed to some further stabilization in June, with a fourth month at 6.3% having ended 2024 at 6.1%, 2023 at 5.8% and 2022 at 5.5%.

- On the wage side, there were slight upward revisions to the ECB's forward looking wage tracker compared to the April vintage, but the broader theme of softening compensation pressures remains intact. The tracker excluding one-off payments is seen at 3.082% in 4Q25 (vs 3.024% in the April iteration).

- On the envisaged moderation from 4.5% in 1Q25, the ECB writes: "The downward trend of the forward-looking wage tracker for the remainder of 2025 partly reflects the mechanical impact of large one-off payments (that were paid in 2024 but drop out in 2025) and the front-loaded nature of wage increases in some sectors in 2024."

- Recall that the ECB projects compensation per employee growth at 2.8% by the last quarter of this year, down from 3.8% in Q1.

- More recently, the Indeed wage tracker for May eased to 2.5% Y/Y (vs 3.2% prior) for the lowest rate since late 2021. The smoother three-month average rate meanwhile was steady at 3.0% Y/Y, revealing a broadly consistent message to that of the ECB’s forward-looking tracker.

ECB: Macro Since Last ECB: Growth - Retail Sales Disappoint In May, Tepid PMIs

- Highlighting some of the more recent monthly hard data, Eurozone real retail sales were weak in May as they slipped -0.7% M/M (cons -0.6) after a downward revised 0.1% M/M (initially 0.3%). All the main categories fell and there was broad-based weakness by countries with Spain the strongest of the “big four” at 0.2% M/M.

- Going against this, Eurozone industrial production was much stronger than expected in May albeit with a likely Irish volatility caveat. Production rose 1.7% M/M (cons 1.0) after -2.2% M/M in April (revised up from -2.4% initial), following a particularly volatile period with Q1 production support by US tariff front-running and April then weighed down by Liberation Day-induced uncertainty.

- GDP for back in Q1 was revised up to 0.6% Q/Q non-annualised and 1.5% Y/Y but that’s now hugely stale. The flash Q2 GDP release is on July 30.

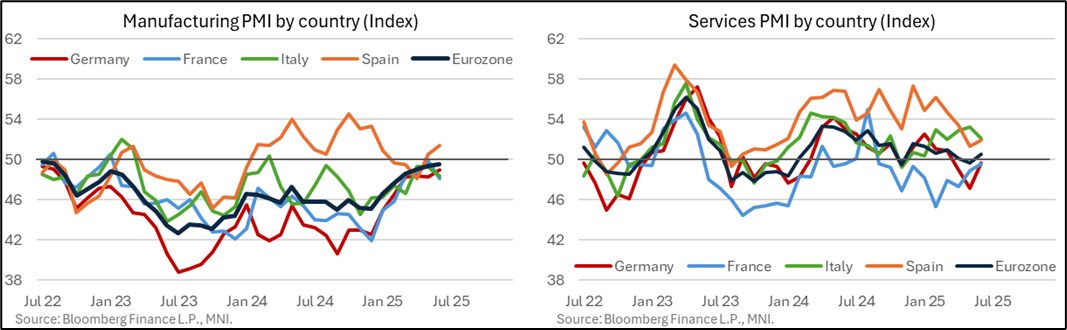

- As for softer data, June manufacturing PMI at 49.5 consolidated May’s relative improvement for its highest since Aug 2022, albeit having remained in contractionary sub-50 territory the entire time.

- The services PMI meanwhile increased to 50.5 in June (better than the 50.0 expected) from 49.7 in May, what had been its lowest since Jan 2024. This level remains below the 51.0 averaged in Q1 prior to reciprocal tariffs and is only just in expansionary territory.

- The composite PMI at 50.6 remains just about in expansionary territory as well, painting a similar picture to the 50.2 in May, 50.4 in April and 50.4 in Q1. The preliminary July PMIs are released on the morning of the ECB decision this week.