EURGBP TECHS: Corrective Phase

- RES 4: 0.8840 High Nov 20

- RES 3: 0.8818 High Nov 26

- RES 2: 0.8802 High Dec 2 and a key near-term resistance

- RES 1: 0.8766 20-day EMA

- PRICE: 0.8737 @ 16:30 GMT Dec 10

- SUP 1: 0.8721 Low Dec 8

- SUP 2: 0.8706 76.4% retracement of the Oct 8 - Nov 14 bull leg

- SUP 3: 0.8670 Low Oct 21

- SUP 4: 0.8656 Low Oct 8 and a key support

A corrective bear cycle in EURGBP remains intact - for now. The cross has breached the 50-day EMA, currently at 0.8752. The break highlights a stronger reversal and a bear threat, plus scope for a deeper retracement, towards 0.8706, a Fibonacci retracement. Initial firm resistance to watch is unchanged at 0.8802, the Dec 2 high. Clearance of this hurdle would be a bullish development and signal a resumption of the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Bullish Structure

- RES 4: 0.8865 1.764 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8848 1.618 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 2: 0.8835 High May 3 2023

- RES 1: 0.8830 High Nov 5

- PRICE: 0.8779 @ 16:13 GMT Nov 10

- SUP 1: 0.8763 Low Nov 3

- SUP 2: 0.8754 20-day EMA

- SUP 3: 0.8716 50-day EMA

- SUP 4: 0.8656 Low Oct 8 and a key support

A bullish condition in EURGBP remains intact and recent gains reinforce current conditions. The move higher has confirmed a resumption of the uptrend and maintains a bullish price sequence of higher highs and higher lows. Sights are on 0.8835, the May 3 2023 high. Initial support lies at 0.8763, the Nov 3 low and just above the 20-day EMA, at 0.8755. Note that the trend is overbought, a pullback would be considered corrective.

PIPELINE: Corporate Bond Update: Near $20B to Price Monday

$19.95B To Price Monday:

- Date $MM Issuer (Priced *, Launch #)

- 11/10 $11B #Verizon: $2B +7Y +90, $2.25B +10Y +100, $1.5B 20Y +110, $3.25B 30Y +120, $2B 40Y +130

- 11/10 $1.65B #Enterprise Products Op $300M 3Y Tap +43, $600M 5Y Tap+73, $750M 10Y tap +93

- 11/10 $1.6B #Caterpillar $1.05B 3Y +37, $550M 3Y SOFR+58

- 11/10 $1.5B #LyondellBasell $500M 5Y +145, $1B 10Y +185

- 11/10 $900M *Mosaic $500M +3Y +77, $400M 5Y +92

- 11/10 $750M #Flex $150M 7Y +105, $600M 10Y +130

- 11/10 $750M #Plains All American $300M 5Y +102, $450M 10Y +142

- 11/10 $700M Carpenter Tech 8.25NC3.25 5.75%

- 11/10 $600M #AutoNation +3Y +90

- 11/10 $500M #Illumina WNG 5Y +105

- 11/10 $2.35B Applied Digital 5NC2 investor call, expected to launch Thursday

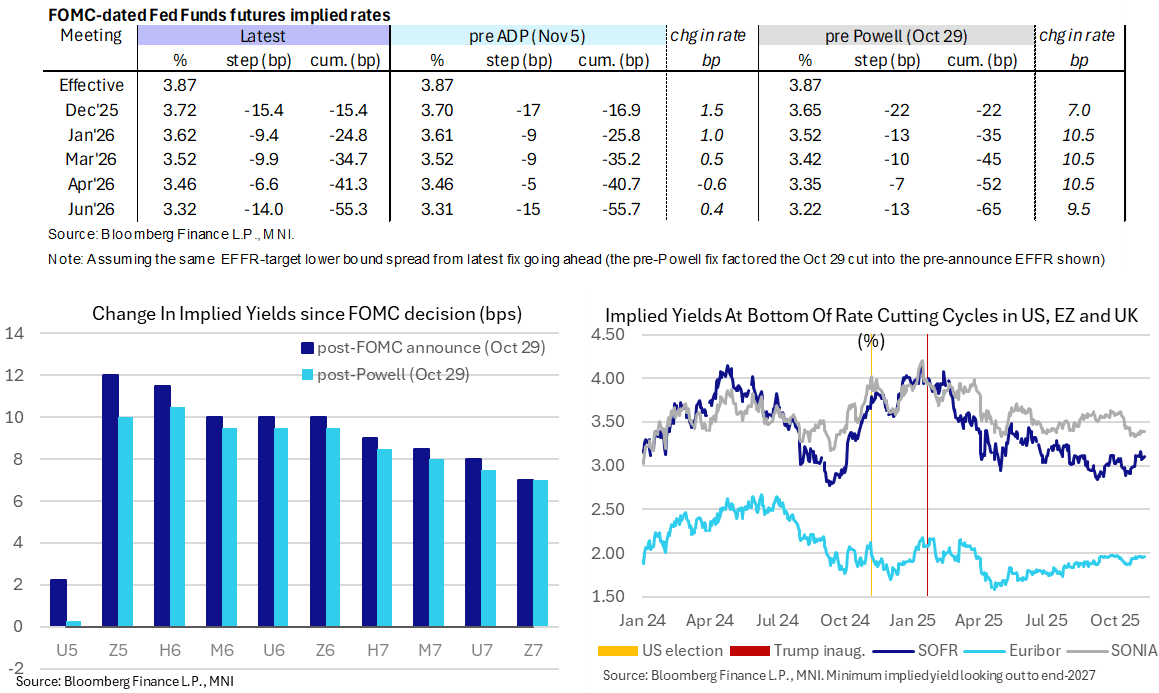

STIR: Fed Rates Await A New Driver As End Of Shutdown Looks More Likely

- Fed Funds implied rates hold the day’s increase, 1-2bp higher from Friday’s close, on the back of improved optimism around the government shutdown ending and talk of $2k tariff dividends.

- Cumulative cuts from 3.87% effective: 15.5bp Dec, 25bp Jan, 34.5bp Mar, 41.5bp Apr and 55.5bp Jun.

- SOFR futures meanwhile have marginally pared some of their overnight losses (sitting up to 3.5 ticks lower) despite equity futures extending gains through the session.

- The terminal implied yield is at 3.105% (H7, +3.5bp) as it holds off Wednesday’s 3.16% which marked the highest close since late July (following beats for ADP and ISM services before weaker alternate labor data and consumer sentiment over Thu-Fri).

- We recapped the wide array of labor indicators for October, which have held greater than usual sway on markets recently, in our shadow Employment Report published earlier today: https://media.marketnews.com/US_Shadow_Employment_Report_Nov_docx_cceb084370.pdf

- Improved odds of the shutdown ending see a greater likelihood that the BLS nonfarm payrolls report for back in September is released in the next week or so.