US LNG: Corpus Christi Files for Feedgas Approval

Oct-24 20:00

Corpus Christ filed with FERC requesting approval to introduce feedgas and refrigerants to cold ends of Midscale Train 4 of the Stage 3 project.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Reversal Lower Extends

Sep-24 19:56

- RES 3: 95.960 - High Apr 7 (cont.)

- RES 2: 95.875 - High Jul 2 (cont.)

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.625 @ 20:42 BST Sep 24

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading lower. It is still possible that the move down is a correction. Near-term resistance to watch is 95.780, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.875, the Jul 2 high on the continuation chart. On the downside, key short-term support has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

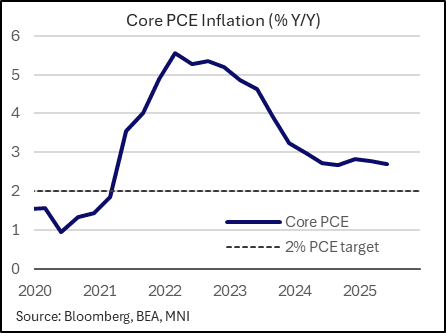

US PREVIEW: PCE, GDP Due For Annual Revisions Thursday

Sep-24 19:53

Thursday (0830ET) sees the third release for Q2 national accounts covering GDP and PCE amongst other components.

- GDP growth is expected to be unrevised at 3.3% annualized although personal consumption could be revised up to 1.7% from 1.6% annualized according to a limited early sample of analysts. Final domestic demand (or PDFP per Fed Chair Powell’s terminology) will be watched after being revised up to a second consecutive quarter at 1.9% annualized in the second Q2 release, still down from the 3% averaged through 2024.

- Note as well that this release comes with the BEA's annual update, which rather than just altering the prior quarter will see changes going back to 1Q20. That should see greater focus on a third release than would usually be the case, including when it comes to the recent core PCE profile.

- Previous editions have led to fairly meaningful revisions in core PCE, with various factors being incorporated including new seasonal adjustments, and CPI / PPI historic series revisions.

- For example, the annual CPI revisions made with January 2025 data haven't yet been reflected in the PCE series through 2024, while seasonal adjustment and PPI revisions will be incorporated throughout. This will have an impact on Y/Y and M/M for this year as well as past years.

- It's difficult to estimate what the revisions will be, and as such difficult to gauge consensus for the impact: Nomura writes that "Available data point to revisions of -5bp to +4bp in monthly core PCE inflation due to annual revisions, resulting in an upward revision of around 10bp to y-o-y core PCE inflation". In short, they write, the revisions "have the potential to materially change the monthly profile of core PCE".

US TSYS: Chicago Fed Goolsbee Uncomfortable W/ Frontloading Rate Cuts

Sep-24 19:45

- Treasuries look to finish near late Wednesday session lows, extending the decline late after hawkish comments from Chicago Fed Goolsbee FT interview headlines aired: "UNCOMFORTABLE OVERLY FRONTLOADING RATE CUTS" while we "STILL HAVE MOSTLY STEADY, SOLID JOBS MARKET...AT THE SAME TIME, INFLATION IS GOING THE WRONG WAY".

- Currently, the Dec'25 10Y trades -7 at 112-21 (yld 4.1447% +.0385) vs. 112-20 low - nearing technical support at 112-205/112-155 (Low Sep 22 / High Aug 5 and 14). Resistance above at 113-12/29 High Sep 18 / High Sep 11 and the bull trigger. Curves mildly steeper: 2s10s +2.868 at 54.666, 5s30s +.195 at 105.129.

- Tsys were under pressure from pre-auction short sets vs. $70B 5Y Tsy note auction and rate locks vs. ongoing heavy corporate issuance (Oracle $18B 7pt). The latest $70B 5Y note auction (91282CPA3) tailed slightly: 3.710% high yield vs. 3.709% WI; 2.34x bid-to-cover vs. 2.36x prior.

- The greenback has been steadily appreciating, resulting in the USD index rising above last week’s post-Fed recovery highs. The next level for the DXY resides at the 50-day EMA, intersecting today just below the 98.00 mark. Despite a fleeting surge above this average in late July, daily closes above have been rare since February this year.

- Main focus is on Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims.