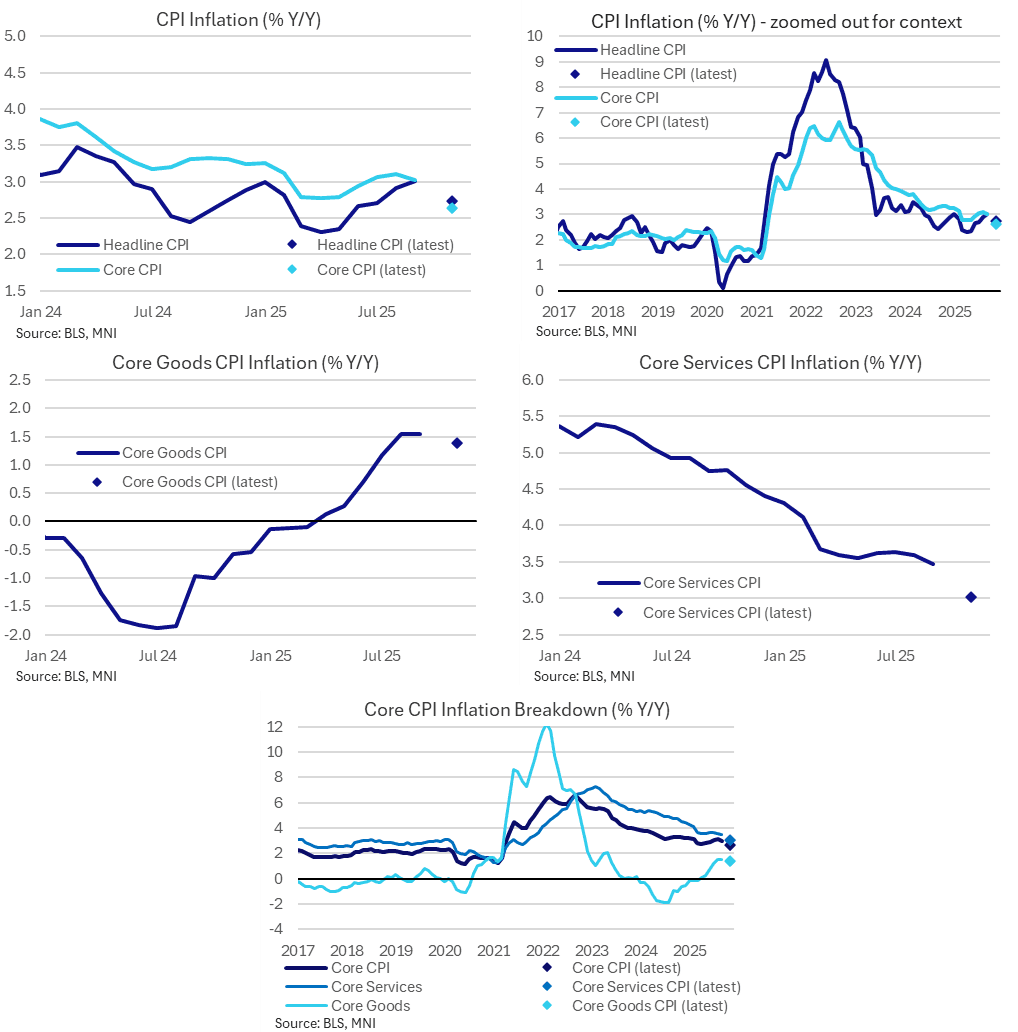

US DATA: Core Services Drive Surprisingly Soft Y/Y Inflation In November

Dec-18 13:43

- Headline CPI was far softer than expected in November at 2.74% Y/Y (we had seen a median estimate of 3.05) after 3.01% in Sep.

- It was led by core CPI at 2.63% Y/Y (median estimate of 2.98) after 3.02% in Sep.

- Core services drove the moderation on the month to 3.02% Y/Y after 3.47%, whilst core goods saw a smaller moderation to 1.39% Y/Y from 1.54% in September.

- Rent components played a sizeable role in this core services moderation, with OER at 3.36% Y/Y vs 3.76% in Sept and primary rents at 2.96% Y/Y vs 3.40% in Sept.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

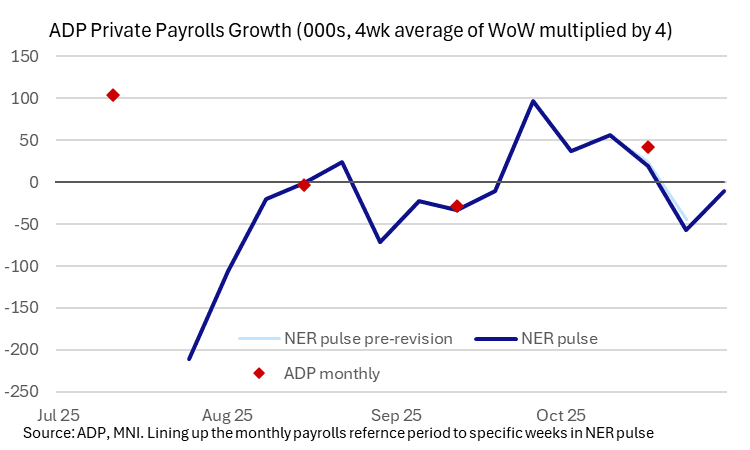

US DATA: Weekly ADP Sees Another Decline Heading Into November

Nov-18 13:42

- The ADP NER Pulse reports -2.5k private sector jobs lost over the four weeks to Nov 1 on a week-on-week basis.

- It follows a downward revised -14.25k (-11.25k) in the previous week to Oct 25 and 4.75k (6.25k previously) in the week to Oct 18.

- Whilst not as weak as last week’s surprisingly soft estimate, it still points to a resumption of a rolling over in jobs growth after the 42k increase in the official monthly report for October had fared a little better than expected after a sizeable decline in September.

- Note the chart below shows on a crude monthly basis to show how it's changed vs the last published monthly figures.

- Once again, ADP warns that “These numbers are preliminary and could change as new data is added."

- Note also that ADP first published this figure at another new link today: https://www.adpresearch.com/job-growth-is-sluggish-but-new-hires-are-on-the-upswing-how/

US TSY FUTURES: BLOCK: Dec'25 2Y Sale Post-Data

Nov-18 13:39

- -5,000 TUZ5 104-05.75, post time bid at 0827:49ET, DV01 $186,350.

- The 2Y contract has since traded up to 104-06.12 (+3.12).

US TSYS: Post-Weekly ADP Jobs React

Nov-18 13:32

- Treasuries extended highs after another lower weekly ADP data release, draws some selling on highs. Currently, the Dec'25 10Y contract trades +9.5 at 112-30 vs. 113-00 high, 10Y yield 4.0922% (-.0464), curves mildly steeper (2s10s +.589 at 53.223; 5s30s +3.204 at 103.862).

- Treasuries continue to trade below resistance at the 113-02 level, an area of congestion since Nov 5. A clear breach of this hurdle would be a bullish signal and suggest scope for a climb towards 113-18+, the Oct 28 high. A break would also cancel a short-term bearish theme. For bears, attention is on 112-10+, the 100-DMA and 112-06, the Sep 25 low. Trendline support also lies at 112-06.

- USD briefly trades a new daily low on the weekly ADP print, however momentum was already headed lower into the print - and markets have since stabilised. USDJPY continues to fade off the earlier cycle highs at 155.44, putting the rate back to flat on the day.

- Next up: Weekly Redbook retail sales (0855ET), NAHB housing index Nov & Factory orders Aug (post-shutdown catch-up) at 1000ET.

Trending Top

Jan-30 21:43

Jan-30 21:11