US DATA: Core PCE Prices Above-Expected, But Supercore Momentum Softening

Jun-27 12:57

Core PCE inflation came in at 0.179% M/M unrounded in May after 0.136% in April (an upward rev from 0.116% prior), which was higher than expected (consensus roughly around 0.15%, implying a split between 0.1% and 0.2% rounded)) with a higher revision.

- That, too, comes after a slightly higher revision to Q1 core PCE this week (3.7% from 3.6%), reflected across all three months albeit front-loaded: January was revised up to 0.344% (was 0.326%), with Feb up to 0.476% (was 0.465%) and March to 0.095% (was 0.091%).

- The Y/Y gauge picked up to 2.68% (expectations had been for 2.6%) from 2.58% prior (upward rev from 2.52%).

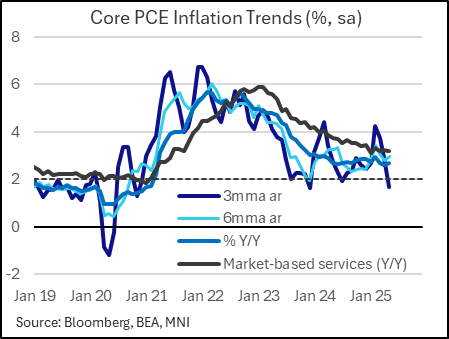

- Core goods printed 0.24% M/M, down slightly from 0.27% in April but still running at a strong rate, while core services ticked up to 0.17% M/M from 0.12%.

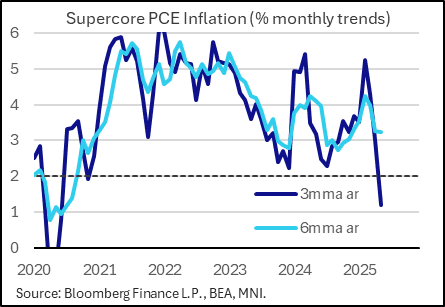

- The core services ex-housing gauge ticked up to 0.129% M/M from 0.01% prior. But this "supercore" reading saw the 3-month annualized rate (ie quarterly) pull back sharply to 1.2% from 3.0% in April, which marked the weakest since June 2020.

- Market-Based services inflation pulled back slightly however, to a 21-month low 0.15% from 0.23% prior, the 3rd consecutive deceleration. After two months of printing above core PCE, it's printing below it again, which the Fed may take note of as it's recently placed more focus on market-based as opposed to imputed inflation.

- Headline came in at 0.136% M/M was also revised higher to 0.118% M/M in April (was 0.100%), the fastest pace in 3 months - a little on the high side of consensus (0.1% rounded, 0.10% average). Headline PCE was 2.34% Y/Y, up from 2.20% prior (and back to the same rate seen in March).

- Overall, the Fed's preferred inflation gauge was running a little hotter in Q1 than previously estimated. However, May's quarterly inflation pace of 1.7% marked the slowest such momentum since December 2023.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR: Broken Put Fly

May-28 12:38

0QZ5 96.25/9600/95.62 broken Put Fly, bought for 1.25 in 10k.

EQUITIES: EU Bank Risk Reversal trades for more

May-28 12:32

SX7E (19th Sep) 150/235RR, bought the Call for 0.20 in 12k total.

US TSY OPTIONS: FVN5 107.00 Puts Trading

May-28 12:32

FVN5 107.00 puts ~8.3K change hands at 0-07+, flow initially triggered by a buyer.