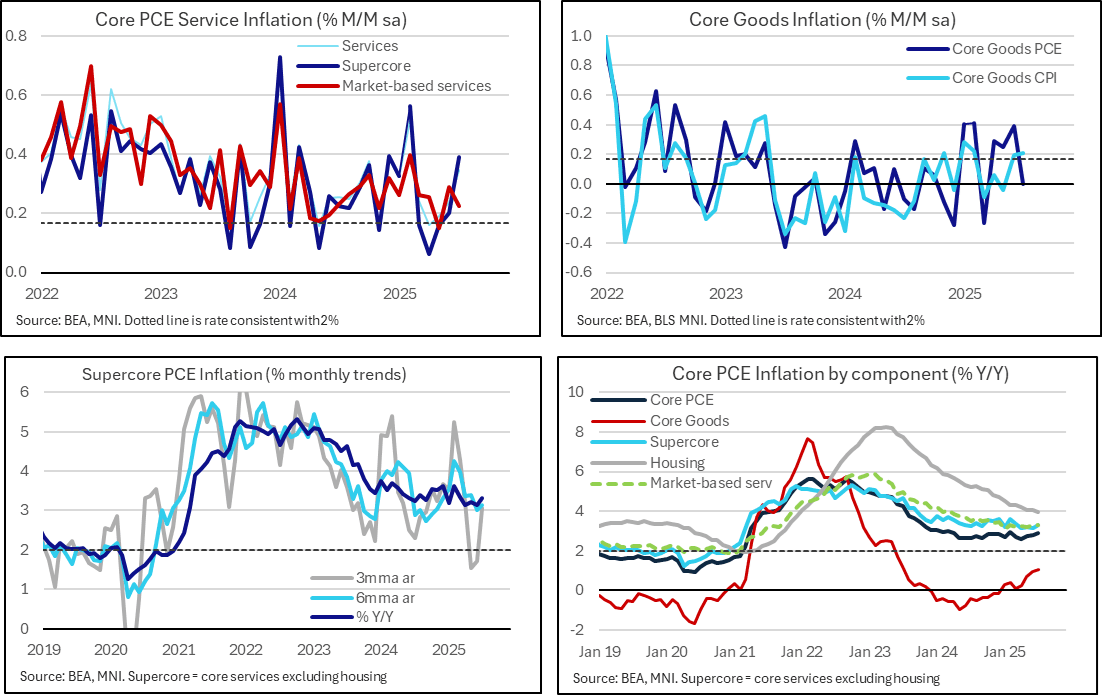

US DATA: Core PCE Confirms Recent Acceleration In Services [2/2]

Core goods PCE inflation halted in July after some strong increases whilst core services ex housing accelerated strongly on the month although some of this was in imputed categories. Nevertheless, FOMC members will be watching this latest uptick in services inflation with various service metrics still stubbornly high.

- Within the details, core goods inflation slowed abruptly in July with 0.00% M/M after a strong 0.39% M/M in June (core goods CPI has seen a steadier trend with 0.21% M/M in July after 0.20% in June).

- The core goods year-ago rate firmed to 1.08% Y/Y for its fastest since July 2023 vs -0.2% Y/Y at Dec 2024 prior to the second Trump administration.

- Core services ex housing (supercore) however firmed to 0.39% M/M after 0.20% M/M (initially 0.19%) in June, for its strongest single month since February.

- Supercore year-ago inflation firmed from 3.15% to 3.32% Y/Y for its strongest since March, although both three- and six-month run rates are at least running a little cooler in relative terms at 3.1% annualized.

- Market-based services inflation was more modest at 0.23% M/M after 0.29% M/M (initially 0.27%). It saw the Y/Y hold at 3.3% Y/Y (where it’s been for four of the past six months) although the three-month is running at 2.7% annualized (joint softest since Jul 2024) and the six-month at 3.2% (softest since Nov 2024).

- Recall that Chicago Fed’s Goolsbee (’25 voter), one of the most dovish members on the FOMC, said on Aug 21 that he thought the rise in July services inflation was a “dangerous” data point that he hopes is just a blip.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Sep'25 30Y Ultra-Bond Buy

- +2,000 WNU5 117-02, post time offer at 0918:59ET, DV01 $380,000.

- The 30Y ultra contract trades 117-02last (-16)

EQUITY TECHS: E-MINI S&P: (U5) Bulls Remain In The Driver’s Seat

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6457.75 High Jul 28

- PRICE: 6411.50 @ 14:18 BST Jul 30

- SUP 1: 6391.50/6322.32 Low Jul 24 / 20-day EMA

- SUP 2: 6241.00 Low Jul 16

- SUP 3: 6173.21 50-day EMA

- SUP 4: 6130.75 Low Jun 25

The trend set-up in S&P E-Minis remains bullish. Recent cycle highs once again confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6173.21. Support at the 20-day EMA is at 6322.32.

US TSYS/SUPPLY: TBAC Had Misgivings Over Buyback Optics, Rising Term Premia

It was interesting to see that the Treasury's private sector advisory group (Treasury Borrowing Advisory Committee, or TBAC) had misgivings over the optics of increasing longer-end liquidity buybacks as it could be seen as an adjustment of the maturity profile of privately-held debt. Indeed, the decision to up 10-20 and 20-30Y buyback sizes and not sizes across the curve didn't appear to be a unanimous recommendation. TBAC also suggested that it was possible to double the size of the buyback program within the requisite parameters and objectives. The full TBAC report to Treasury is here.

- In determining what buyback sizes to recommend, TBAC reiterated that "the Committee focused heavily on Treasury’s stated objective: liquidity support buybacks are not intended to change the overall maturity profile of debt outstanding." And "in order to quantify that, the Committee reviewed the 3y standard deviations of annual changes in WAM (2 months across all environments, 1 month across non-recessionary environments). The Committee noted that the current program, if executed fully at maximum sizes offered, shortens WAM by 0.4 months per year – well within the typical 1y change. The Committee felt that there was therefore capacity to double the program, if appropriate, without materially impacting WAM."

- However, "There was some debate among Committee members as to whether concentrating an increase in liquidity support buybacks in certain sectors of the curve could be misconstrued as WAM management, and for that reason many members felt a uniform increase across the curve, even though take up might routinely be below capacity, would be preferable. The majority of the Committee felt that they would be more comfortable recommending larger increases, or sectoral specific increases, if there was a more directly visible incorporation of the buyback program related funding needs into Treasury’s overall issuance decision."

- And "there was some discussion as to when weakness in certain sectors, as evidenced by the presenting member’s buyback score, warranted a buyback adjustment versus an issuance reconsideration. Regardless, the Committee felt that communication to the market was critical to ensure the program was not misconstrued to be active WAM management. Overall, the Committee felt there was scope to make the program larger and more responsive to evolving market conditions, while still being regular and predictable. However, it would be critical that Treasury monitor and adapt to any material buyback-driven change in debt distribution. The Committee feels strongly that issuance is the primary tool for managing the debt profile."

- The committee also noted that it could be a good time to reassess the "optimal debt structure" given a rise in term premia. Versus a Q3 2023 TBAC study: "term premium has increased modestly more than the scenarios considered, suggesting that a refresh of the optimal debt structure analysis could be beneficial. Additionally, the Committee discussed the fact that evolution in demand patterns suggests increased demand in front end and intermediate maturities relative to reduced demand in longer end maturities."

- Additionally, there appeared to be some debate about Treasury's forward guidance on coupon upsizing: "Given the breadth of uncertainty relating to both receipts and expenditures, the Committee was mixed on whether adjustment to Treasury’s expressed expectations of future changes was necessary."