EUROPEAN INFLATION: Core Momentum Highest Since May But Services Drivers Unclear

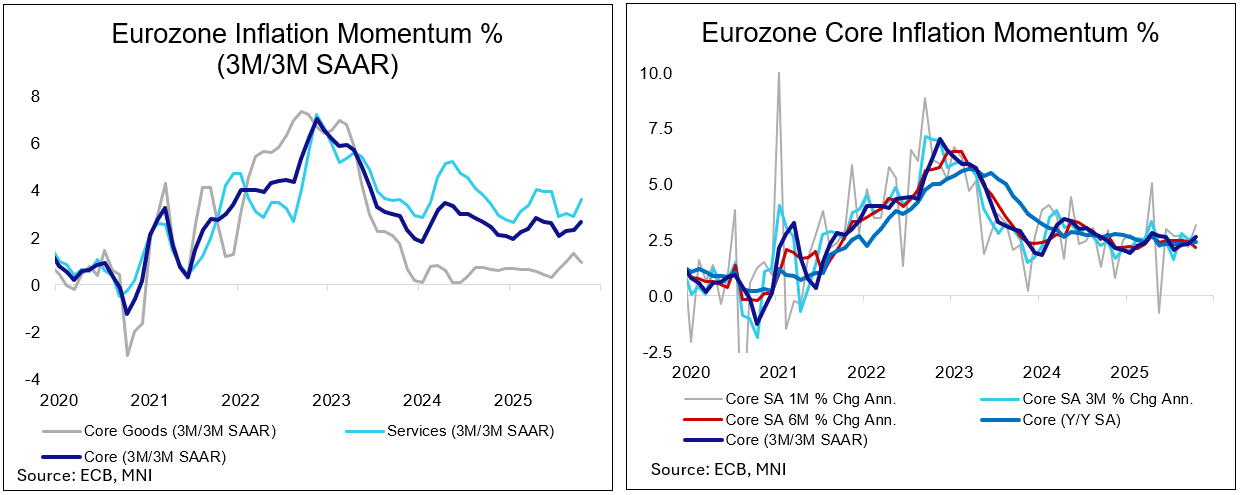

Eurozone core inflation momentum firmed in October to its highest rate since May according to this afternoon's ECB seasonally adjusted data. Some of the services strength behind it may be caveated by coming from volatile travel related categories (implied by previously released country-level NSA data), but we can't say for sure how much of the rise came from more persistent categories. Strength coming from the latter would encourage the more hawkish cohort of the ECB Governing Council who have clearly advocated against a renewed rate cut to 1.75%. ECB-dated OIS only has 1bp of cuts priced for the December meeting although some recent sources pieces have entertained a closer decision than that would imply.

- Core inflation momentum accelerated to 2.66% in October after 2.31% in September and the highest since May, calculated here as a 3m/3m annualised rate using ECB seasonally adjusted data. This brings the YTD average in the series to 2.40%.

- On a sequential basis, core prices rose 0.26% M/M vs 0.18% in Sep and 0.22% in Aug.

- Services inflation momentum was the driver here, increasing to 3.61% (vs 2.90% in September), the highest rate since June.

- It came with monthly services inflation of 0.39% M/M after 0.24% in Sep and 0.33% in Aug.

- Core goods momentum meanwhile gave back a little of its recent acceleration, easing to 0.93% vs a downward revised 1.33% in Sep (previously shown at 1.45%) and 1.0% in Aug. It points to less upside risk to the 0.6% Y/Y printed earlier today in the NSA data than implied last month.

- Core goods prices fell -0.05% M/M after 0.06% in Sept for technically the first decline since April.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (Z5) Bounces Off Support At The 50-Day EMA

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 112-31/113-00 High Oct 01 / High Sep 24

- PRICE: 112-22+ @ 16:41 BST Oct 1

- SUP 1: 112-01 50.0% retracement of the Jul 15 - Sep 11 bull phase

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Prices bounced Wednesday, despite the short-term bear cycle. Recent weakness has resulted in a print below the 50-day EMA, currently at 112-10+. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high.

MNI: US EIA: CRUDE OIL STOCKS EX SPR +1.79M TO 416.5M SEP 26 WK

- US EIA: CRUDE OIL STOCKS EX SPR +1.79M TO 416.5M SEP 26 WK

- US EIA: DISTILLATE STOCKS +0.58M TO 123.6M IN SEP 26 WK

- US EIA: GASOLINE STOCKS +4.12M TO 220.7M IN SEP 26 WK

- US EIA: CUSHING STOCKS -0.27M TO 23.5M BARRELS IN SEP 26 WK

- US EIA: SPR +0.74M TO 406.7M BARRELS IN SEP 26 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -1.6% TO 91.4% IN SEP 26 WK

FED: US TSY 17W BILL AUCTION: HIGH 3.785%(ALLOT 64.24%)

- US TSY 17W BILL AUCTION: HIGH 3.785%(ALLOT 64.24%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 27.84% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 6.17% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 65.98% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.32