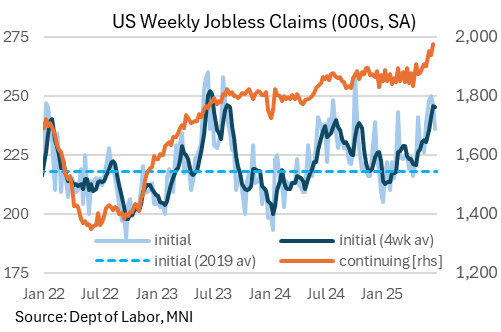

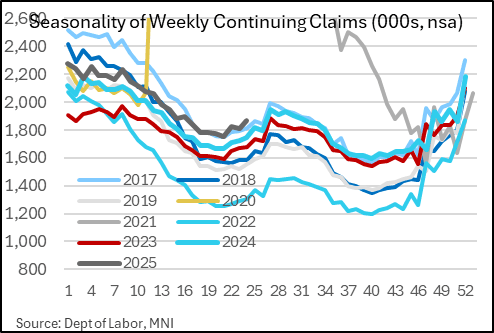

US DATA: Continuing Claims At Fresh Post-2021 High Suggests Continued Cooling

Jun-26 12:48

Initial jobless claims fell more than expected in the week of June 21, to 236k (243k survey) in what was the 2nd consecutive weekly fall (prior 246k rev up 1k) to a 5-week low.

- Once again though, continuing claims set a fresh post-Nov 2021 high, up to 1,974k (1,937k prior ref down 8k), much higher than the 1,950k expected in the Jun 14 week. The claims rate ticked up 0.02pp to 1.29%, a post-Dec 2021 high.

- The data are very much consistent with Fed Chair Powell's largest concern about an otherwise solid labor market, as he put it last week: "The thing is, there's -- a more concerning thing is there's not a lot of layoffs, but there's not a lot of job creation...if you're out of work, it's hard to find a job. But very few people are being laid off at this point."

- There was nothing out of the ordinary seasonality-wise, with initial claims usually coming down this time of year and continuing claims edging higher through mid-year. Notable state-by-state moves in initial claims included New Jersey (up 5.8k, a typical seasonal rise), with Minnesota (-5.2k) reversing some of the unusual rise seen in prior weeks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR: Looking for Unchanged Rates via Options

May-27 12:47

Looking for Unchanged Rates into Year end:

- SFRU5 95.87/95.75ps 1x2, with 95.93/95.75ps 1x2, bought the strip for 3.25 in 5k.

FOREX: US Election Related Highs Continue to Cap NZDUSD Topside, RBNZ Awaited

May-27 12:46

- NZD sits among the worst performers in G10 on Tuesday, shrugging off the more optimistic tone for global equities and taking its cues from the broader dollar rebound. Today’s 0.65% selloff has seen NZDUSD gravitate back below 0.6000 handle, as a cluster of US election related highs between 0.6025/38 continue to cap the topside for the pair.

- 0.6038 also represents the 61.8% Fibo retracement of the Sep’24-Apr’25 selloff. A break above here would signal scope for a stronger move towards the 76.4% at 0.6168. On the downside, the 50-day EMA has yet to be tested following the sharp break above on April 10. This average intersects at 0.5873 and will be firm support ahead of the RBNZ decision overnight.

- The RBNZ decision will take focus overnight, where rates are widely expected to be cut 25bp to 3.25%. Given heightened uncertainty, the MPC is likely to retain its easing bias again stating it has “scope” to cut rates further if required and its updated OCR path will garner attention. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal the potential need for greater accommodation.

- Our full preview with analyst views is here.

US TSYS: Minor Moves On Hassett And Then Durable Goods

May-27 12:38

- Treasuries have ticked a little higher on the preliminary April durable goods report, with overall orders not quite as weak as expected but core orders more notable as they surprisingly slipped -1.3% M/M (cons -0.1%) with only a partial offset from an upward revised 0.3% (initial 0.1%).

- TYM5 at 110-08 is back around where it was before it nudged 1-2 ticks lower shortly before the durables release to ~110-06 on NEC’s Hassett saying there could be more trade deals announced this week and that tariffs could go to 10% or less for some countries with good offers.

- Cash yields are 0.6-6.3bp lower on the day, with 30s leading the declines on the previously discussed potential Japan MoF bond issuance composition tweaks.