EM ASIA CREDIT: Contemporary Amperex: Reserve report brings restart closer

(CONAMP, A3/A-/A-)

"Lithium Miners’ Shares Slide After CATL Mine Reserves Approved" - BBG

Contemporary Amperex (CATL), the world’s largest EV battery supplier, had suspended operations at its Jianxiawo lithium mine in Jiangxi after its mining license expired in August. The approval of its reserve report brings it closer to a restart. The suspension was always expected to be temporary. Neutral for spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

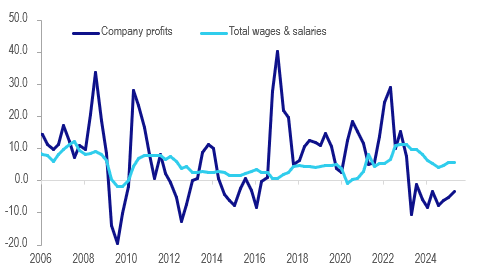

AUSTRALIA DATA: Little Change In Q2 Inventories, Profits Remain Weak

Q2 inventory volumes rose 0.1% q/q, close to expectations, after an upwardly-revised +1.2% in Q1. Thus it seems likely that its contribution to Wednesday’s Q2 GDP is likely to be close to neutral. Q2 net export and public demand contributions are published on Tuesday. Bloomberg consensus is forecasting GDP growth to improve to 0.5% q/q and 1.6% y/y after Q1’s 0.2% & 1.3%.

- Company operating profits fell 2.4% q/q in Q2 to be down 3.3% y/y after -1.0% & -5.2% in Q1. The level is now 16.3% lower than Q2 2022, while total wages are 22.2% higher. It appears catch up for the previous five years. The annual profit rate has been contracting for the past two years.

- Wages and salaries rose 1.0% q/q to be up 5.8% y/y in Q2, the highest since Q1 2024.

- Mining profits fell 0.5% q/q while wages & salaries rose 2.3% q/q. Sales volumes were 1.2% q/q higher but inventories increased 4.8%.

- Retail sales volumes increased 0.8% q/q while stocks fell 0.5% but profits fell 5.8% as wages increased 1.2%.

Australia company profits vs wages & salaries y/y%

CHINA PRESS: China Opposes U.S. Removal Of Semiconductor Firms From VEU List

The Ministry of Commerce on Saturday voiced opposition to the U.S. choice to withdraw Validated End-User authorization for three semiconductor businesses running in China. China urged the U.S. to rethink the move, adding it would take necessary measures to safeguard the legitimate rights and interests of enterprises, the Ministry said, after the U.S. removed Intel Semiconductor (Dalian) Co., Ltd., Samsung China Semiconductor Co., Ltd. and SK Hynix Semiconductor (China) Ltd. from the VEU list. VEU permission allows U.S. exporters to ship certain high-technology civilian items to pre-approved entities without requiring private export licenses for each shipment.

AUSSIE BONDS: Futures Hold Lower, Ignoring Softer Q2 GDP Partials

Aussie bond futures maintain a negative bias, despite softer Q2 GDP partials and monthly building approvals data. The back end remains softer, with XM (10yr) futures down 3.5bps to 95.665. 3yr futures (YM) are off by 1.5bps to 96.575. Still, both contracts remain up from late August lows. US Tsy futures are mostly lower as well, providing a negative bias for the Aussie market.

- In the cash ACGB yield space we are around 1-5bps higher, with the 10-30yr tenors leading from a yield standpoint. The benchmark 3yr is up around 1.5%bps to 3.41%, while the 10yr is up 3bps to be back above 4.3%.

- The data showed Q2 company profits down 2.4%q/q, against a +1.1% forecast rise, while Q1 printed at -1.0%. Inventories were +0.1% in Q2, against a 0.2% forecast rise. Building approvals fell 8.2%m/m in July, after a 12.2% gain prion. August ANZ job ads were +0.1%m/m, after a -0.6% decline in July.