US DATA: Consumption And Income Momentum Remained Limited At End-Q2

June's Personal Income and Outlays report confirmed a slowdown in spending and income growth in the second quarter, with May looking to have been the weakest month but the subsequent recovery in consumption looking fairly tame so far.

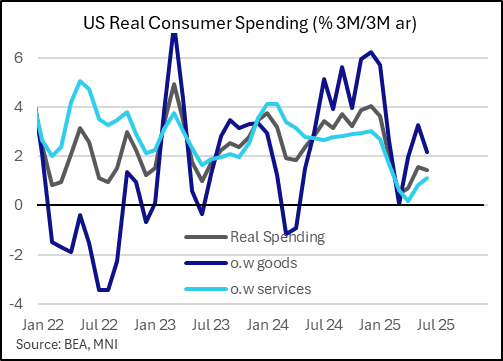

- Real spending rose by 0.1% M/M (0.06% M/M unrounded) in June, remaining below its end-2024 level albeit amid significant volatility along the way (0.7% rise in March ahead of tariffs, 0.1% in April, -0.2% in May). The 3M/3M annualized rate came in at 1.4% (after 0.5% in Q1). This merely confirms the quarterly PCE consumption reading in this week's Q2 GDP report but suggests that there was neither strong momentum coming into nor exiting the quarter.

- That said, services spending was steady throughout, rising 0.1% M/M in each month of the quarter (albeit decelerating very slightly on an unrounded basis), though overall this remains an area of softness (up 1.1% 3M/3M SAAR). To be fair this is an improvement from contractions in January and February, but not an area of particular strength.

- Real goods spending meanwhile had a more pronounced drop to open the quarter (negative in April and May, shifting barely positive at +0.1% in June), leaving the quarterly growth rate at 2.2% but a far cry from ~6% at the turn of the year.

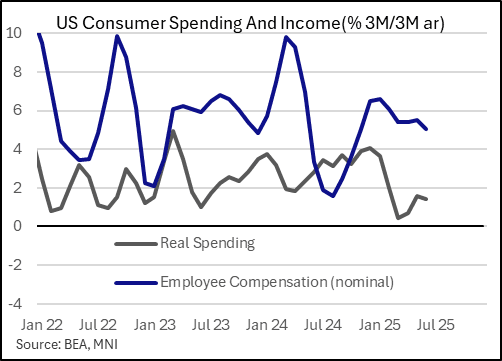

- Real disposable income growth was flat in June, following -0.7% in May. Previous months' readings have been distorted by one-off Social Security payments, but the underlying trend of growth remains fairly solid at 3.0% 3M/3M SAAR (was 2-2.5% for most of late 2024/early 2025).

- What's more worrisome is a slowdown in nominal employee compensation: June's 0.2% M/M rise was the weakest in 11 months, bringing the 3M/3M growth rate down to 5.1%, a 7-month low. To be sure this is still robust but down from the 5.4-6.6% quarterly growth rate over the preceding six months.

- With consumption growth in this cycle being very much employment income-driven, this is a potential warning sign worth watching in the coming months.

- The household savings ratio was flat at 4.5%.

- Real variables were revised down very slightly in the updated Apr/May readings on account of the higher PCE inflation estimates.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Redbook Retail Sales Growth Remains Steady Amid Weakness In Other Data

Johnson Redbook retail sales posted a 4.9% Y/Y rise in the week to Jun 28, accelerating from 4.5% the week prior and bringing the month-to-date sales increase to 4.9% Y/Y (up from the prior week's MTD of 4.8% but on the light side compared to retailers' targeted 5.7%). Technically, June is a 5-week retail month which ends July 5.

- The anecdotes of the report are largely upbeat, pointing to both rising activity in the week alongside discounting and some anticipation of Amazon Prime Day: "The Fourth of July holiday promotions, combined with summer heat waves and the demand for seasonal goods, have led to an increase in customer traffic and sales for the week. Many stores now display summer clearance items alongside fall merchandise. Since this year's July 4th falls on a Friday, many retailers are responding by offering sales promotions that extend from the weekend before to the weekend following Independence Day. Shoppers are stocking up on food and beverages in anticipation of the holiday. Meanwhile, retailers are preparing to compete with Amazon's Prime Day sales, scheduled for July 8th to 11th."

- Amid some weakness seen in recent consumer data, including a downward revision to Q1 private consumption and May's PCE, Johnson Redbook sales' resilience casts a slightly more positive light on the consumer though there's clearly been a slowdown in this series since April's 6.7% Y/Y post-2022 high (likely influenced to some degree by pulling forward purchases ahead of tariffs).

- June's Census Bureau retail sales report (Jun 17) will be eyed for improvement (was a soft 3.3% Y/Y), especially in ex-auto sales (-0.3% M/M in May), albeit the Control Group sales were solid at +0.4% M/M.

BUND TECHS: (U5) Recovered From Monday’s Low

- RES 4: 132.42 2.000 proj of the May 14 - 20 - 22 price swing

- RES 3: 132.00 Round number resistance

- RES 2: 131.95 High Jun 13 and the bull trigger

- RES 1: 130.73/131.33 Intraday high / High Jun 20

- PRICE: 130.63 @ 13:34 BST Jul 1

- SUP 1: 130.00 Low Jun 30

- SUP 2: 129.67 76.4% retracement of the May 14 - Jun 13 bull leg

- SUP 3: 129.30 Low May 22

- SUP 4: 128.97 Low May 14 and a reversal trigger

Recent weakness in Bund futures resulted in a print below key short-term support at 130.12, the Jun 5 low. A clear break of this price point would highlight a bearish threat, undermine the recent bullish theme, and signal scope for an extension towards 129.30, the May 22 low. The contract has recovered from yesterday’s low. Key resistance has been defined at 131.95, the Jun 13 high. Clearance of this level would reinstate a bullish theme.

CROSS ASSET: Selling Orders are emerging in Treasuries

- Some order flow are hitting the Treasuries, but nothing big, TYU5 is sold in 4k, FVA 3k, USA 1k.

- US Emini is seeing some small momentum selling, now targets Yesterday's low at 6223.25, which is also Yesterday's Open.

- This is helping the USDJPY back at the 143.00 figure, but all within ranges across multi Assets.