EU CONSUMER CYCLICALS: CONSUMER CYCLICALS: Consumer & Transport: Week in Review

The only point in macro we want to flag is today's US June PCE print that pointed to relatively solid real consumption (+0.2%). But as our economist notes real income growth was slowing towards the end of the quarter and personal savings rate at 3.4% is at the lowest since Dec '22. Our focus stays on earnings which will give better a forward indication for now. We've linked the movers this week below and it wasn't all in earnings; Essity continues to price out Event of Default triggered put at par, Rentokil has started pricing in a par put on potential PE buyers and Whirlpool is repricing (mainly in $s) its chances of a rating uplift after Bosch made another acquisition.

As an aside, we know credit doesn't like to care about governance but over time we often see that as a costly mistake. The most recent example was Burberry, a co we gave multiple warnings of when it came to primary. The bond we saw as effectively funding elevated equity pay-outs from the year before and the CEO's strategy to capex store refurbishments while refusing to disclose online sales exposure was worrying. He was let go by the board last week and the new '30 bond holders have been left with 40bps of spread widening. We again see red flags this week on Elo/Auchan who thought it was appropriate to have a private call for one of its most watched earnings before releasing a public presser. Yes, a private co, but it has €7b in public bonds, Xover member CDS and revisiting public markets as recently as April.

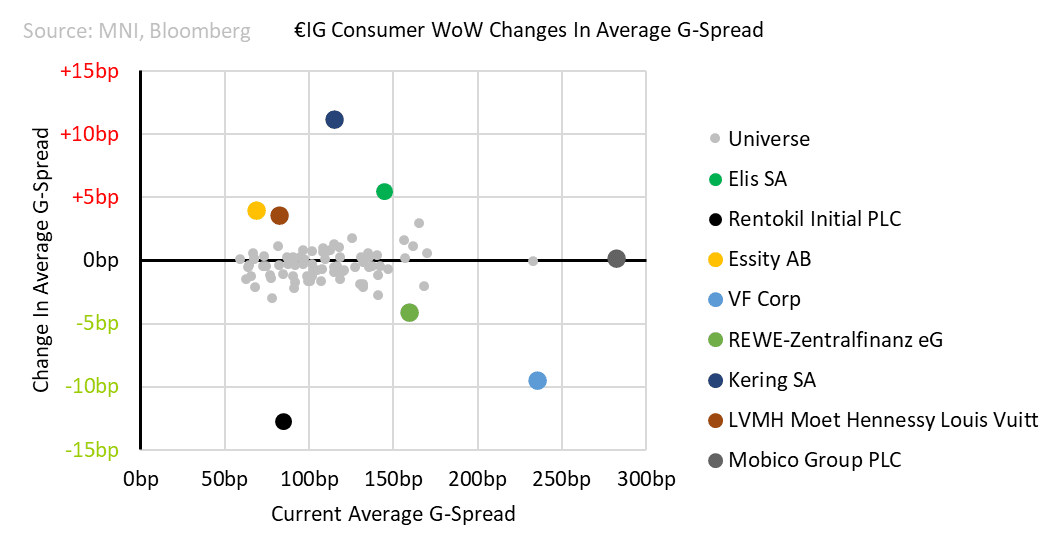

Ex. Auchan the two other disappointments in earnings - Air-France and Kering - should have been expected. Levels are better on both, but we remain cautious on the lack of positive near-term catalyst and macro potentially weakening before then. No Primary this week for us.

Notable Earnings

- Elo/Auchan (NR/BB+); Poor results were already flagged by S&P as it took on loss-making Casino stores this half. But still the approach to communication and plans to pull margins out of the gutter are unclear to us. The price action and trends in earnings will no doubt trigger some to think back to fellow French grocer Casino and its bonds (went to single digits before restructuring).

- easyJet (Baa2/BBB Pos); after disappointment from Ryanair, firm results took us (and the market) by surprise. Unfortunately, cash curve was and is not showing much value. Booking.com might turn into a comp. as its Holiday business continues to contribute more and more.

- Air France-KLM (NR/BB+/BBB-); tough co to follow and catalyst are not positive near term. Impact from Olympics it keeps warning on and indications of month-to-month trends within Q2 was indicative of that.

- Carrefour (NR/BBB); benefits of diversification (particularly when that means out of France Food) is showing for CAFP. It downplayed the weaker areas, one to watch in Q3 for any larger risks from that continuing.

- Whirlpool (Baa2/BBB-/BBB Neg); post-Bosch comments we see it needing to come out. Results were weak on the bottom line adding to the pain for longs.

- Reckitt (A3 Pos/A-); unclear where proceeds from trimming down the business will go but it has a history of high-grade ratings. Still not provisioning for any NEC claims.

Event-driven Movers

- International Game Technology (Ba1/BB+ CW Pos/BBB-); Looks like more cash coming its way on Apollo taking the gaming business, EoD trigger is unclear to us but regardless IG ratings on closure there.

- Essity (Baa1/BBB+); no formal notice, yet 31s are leaking wider. Not great sign for those eyeing the par put but again caution for those not in the conversation.

- Whirlpool (Baa2/BBB-/BBB Neg); repriced chances after Bosch mgmt downplayed future acquisitions.

- Rentokil (NR/BBB/BBB); PE rumours spark CoC at par possibility.

Rating Changes

- Adecco (Baa1/BBB+ Neg); S&P moves to neg. outlook.

- Walgreen Boots (B1/BB Neg); S&P finally moves off IG with a double notch downgrade and neg. outlook.

- VFC (Baa3 Neg/BBB- Neg); extreme patience from raters continues, Moody's stays put.

- Carnival (unsecured; B2 Pos/BB); Moody's follows S&P with a single-notch upgrade and pos. outlook. Still notches aggressively for unsecured.

- LVMH (Aa3/AA-); S&P promptly comes out to green light earnings performance in the face of peers.

- Tesco (Baa3/BBB- Pos/BBB-); S&P moves to positive outlook echoing a recent run of positive news for the co.

- Deutsche Post (A1/NR/A-); Fitch with a 1-notch upgrade to the dislocated/tight curve

- Fnac Darty (NR/BB+ Neg/BB+ S); S&P positive on Unieuro acquisition (headline only).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Sell-Off Momentum Slows, 5Y Supply Ahead

- Treasuries probed marginally lower in recent trade, with TY touching a new session low of 110-01+, before lifting back to 110-03.

- Momentum behind today’s sell-off slowed after a sharp decline in new home sales albeit one that was partly mitigated by large upward revisions. A beat for Australian CPI set the tone overnight (building on yesterday’s CAD CPI) after which there has been little new headline drivers for the sell-off.

- TY dipped below the Jun 13 low (110-03) but holds above more meaningful support seen at 109-25 (50-day EMA).

- Cash yields sit 4.8-6.7bps higher on the day, led by 20s, with 2s10s at -43.3bps off yesterday’s ytd low of -50.8bps (most of that aided by the new 2Y).

- Near-term Fed implied rates have been less willing to lift further today, with the end-2024 effective rate of 4.88% unchanged from when US desks filtered in, showing some reluctance to push much further above pre-retail sales levels ahead of more notable data over the next two days.

- The 5Y auction at 1300ET is now firmly in focus after yesterday’s well-received 2Y – more to come on this a little nearer the time.

US 10YR FUTURE TECHS: (U4) Bullish Trend Structure

- RES 4: 111-31 1.382 proj of the Apr 25 - May 16 - 29 price swing

- RES 3: 111-17+ 1.236 proj of the Apr 25 - May 16 - 29 price swing

- RES 2: 111-13 High Mar 25

- RES 1: 111-01 High Jun 14

- PRICE: 110-03 @ 16:27 BST Jun 26

- SUP 1: 109-25+/109-00+ 50-day EMA / Low Jun 10 and key support

- SUP 2: 108-27+ Low Jun 3

- SUP 3: 108-14+ Trendline drawn from the Apr low

- SUP 4: 107-31 Low May 29 and a key support

A bull cycle in Treasuries remains in play and S/T pullbacks are considered corrective at these levels. The recent consolidation still appears to be a flag formation - a bullish continuation signal. Furthermore, the breach of resistance at 110-21, Jun 7 high, confirmed a resumption of the bull leg that started Apr 25, and opens 111-17+, a Fibonacci projection. Key support to watch lies at 109-00+, the Jun 10 low. A break would reinstate a bearish theme.

US TSYS: US TSY 17W BILL AUCTION: HIGH 5.220%(ALLOT 74.31%)

- US TSY 17W BILL AUCTION: HIGH 5.220%(ALLOT 74.31%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 44.85% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 4.15% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 51.00% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 2.75