ISRAEL: Consumer Prices Rise 2.5% Y/Y in October, In Line With Expectations

- "ISRAEL OCT. CONSUMER PRICES RISE 2.5% Y/Y; EST. +2.5%" - BBG

- "ISRAEL OCT. CONSUMER PRICES RISE 0.5% M/M; EST. +0.5%"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: OAT Futures Narrowing Gap To Resistance; French Risks Still Present

OAT futures are slowly narrowing the gap to resistance at 123.23 (equates to the 3.35% 10-year yield level), currently +47 ticks at 123.16. Regional headline flow remains fairly limited, with yesterday’s pullback in near-term French political risks driving the intraday bid in EGBs.

Although French PM Lecornu now looks likely to survive tomorrow’s censure votes, France’s political/fiscal outlook still faces risks.

- Socialist leader Faure has noted that "I didn't buy the budget, I'm going to fight it tooth and nail from now on, and we'll see who on the right and the left gets satisfaction article by article."

- Lecornu will have to tread a fine line in budget negotiations to avoid losing implicit support of the Socialists and/or the LR. Some Socialist MPs (e.g. Paul Christophle) are still planning to censure the Government despite their Party’s intstructions.

- Additional concessions to the Socialists would further impede fiscal consolidation efforts, and likely push the expected 2026 deficit closer to 5.0%, rather than the 4.7% currently targeted.

That said, today’ s strength in OAT futures is continuing to support Bunds. Bund futures are once again testing the 130.00 figure (+29 ticks at 129.97), which shields resistance at 130.05 (76.4% retracement of the Jun 13 - Sep 3 bear leg).

US TSYS: Early SOFR/Treasury Option Roundup

Light SOFR and Treasury options trade overnight, flow paired amid call & put buyers. Underlying futures gaining slightly in 2s-10s, bonds outperforming. Projected rate cut pricing largely steady vs. late Tuesday levels (*): Oct'25 at -24.5bp (-24.2bp), Dec'25 at -48.4bp (-48.4bp), Jan'26 at -61bp (-61.2bp), Mar'26 at -74.1bp (-74.1bp).

- SOFR Options:

- 3,300 SFRM6 98.00/98.12 call spds, 0.5 ref 96.84

- 4,500 SFRX5 97.00 calls, cab ref 96.365 ref 96.365 to -.37

- +2,000 SFRF6 97.00/97.50 2x1 put spds, 0.5

- +8,000 SFRZ5 96.25/96.43 2x1 put spds, 5.5 ref 96.37

- +1,250 SFRX5 96.18/96.37/96.56 iron flys, 6.5 ref 96.375

- Treasury Options:

- +5,500 TYZ5 111/112 put spds vs. 116 calls, even net

- +3,000 TYX5 115/116 1x2 call spds, 0.0

- +2,000 TYZ5 114.5/115.5 call spds, 13 ref 113-15

- +2,000 TYZ5 114.5/115 call spds, 8 ref 113-15.5

- +2,000 TYX5 111.5/112/112.5/113 put condors, 6.0

- over 8,000 TYX5 114 calls, 10

- 2,000 FVZ5 108.5 puts, 5 ref 109-24.75 to -25

- 2,000 USZ5 110/114 2x1 put spds, 10 vs. 118-07/0.06%

- +4,000 TYZ5 111/112 put spds, 9

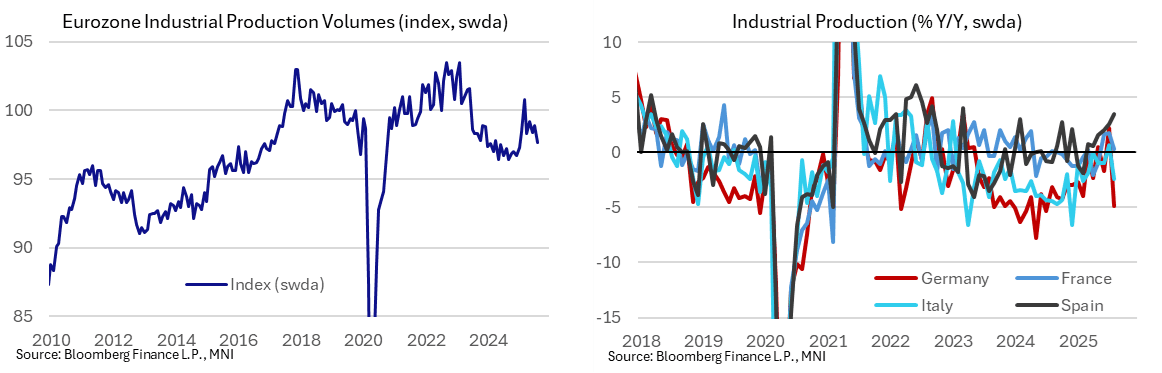

EUROZONE DATA: Ireland Boosts August IP But Weakness Broad Across Big 4, Sectors

Euro area industrial production fell -1.2% M/M in August, albeit not as weak as the -1.6% expected after all 'big 4' countries contracted. While a July revision (0.5% from 0.3% unrevised) underpins the upward surprise, Ireland had an outsized positive impact this time, at 9.8% M/M. Sequential weakness was broad-based in August with all main categories except non-durable consumer goods down M/M.

- All four main Eurozone countries saw M/M declines in August, with Germany standing out negatively at -5.2% (auto slump at least in part attributed to holiday closures and production changeovers), France at -0.7%, Italy at -2.4%, and Spain at -0.1%. These compare to July prints of 1.5%, -0.1%, 0.4% and -0.5%, respectively.

- Eurostat added an explicit comment on Ireland's 9.8% M/M print, saying "the high weight of subcontracted production makes the Irish industrial production index volatile, monthly changes can be higher than in other countries". The volatility of the series suggests a risk of reversing in September.

- August weakness was broad-based across sectors, with energy at -0.6% M/M (-1.7% prior), intermediate goods at -0.2% (0.5% prior), capital goods at -2.2% (1.7% prior), durable goods at -1.6% (1.2% prior), and only non-durable goods marginally positive at 0.1% (1.8% prior). Also on a Y/Y comparison, all sectors except non-durable consumer goods (8.2% Y/Y, not unusually high for recent months) saw declines in August.

- The Eurozone Manufacturing PMI dipped back into contraction zone amid lower factory orders in September: "September’s contraction in the headline [Manufacturing] PMI was driven by a reduction in new order inflows and a sharper rate of job shedding. Production volumes continued to expand, although the pace of growth slowed markedly from August’s near three and-a-half-year high."