EU CONSUMER CYCLICALS: CONSUMER CYCLICALS: Consumer & Transport; Week in Review

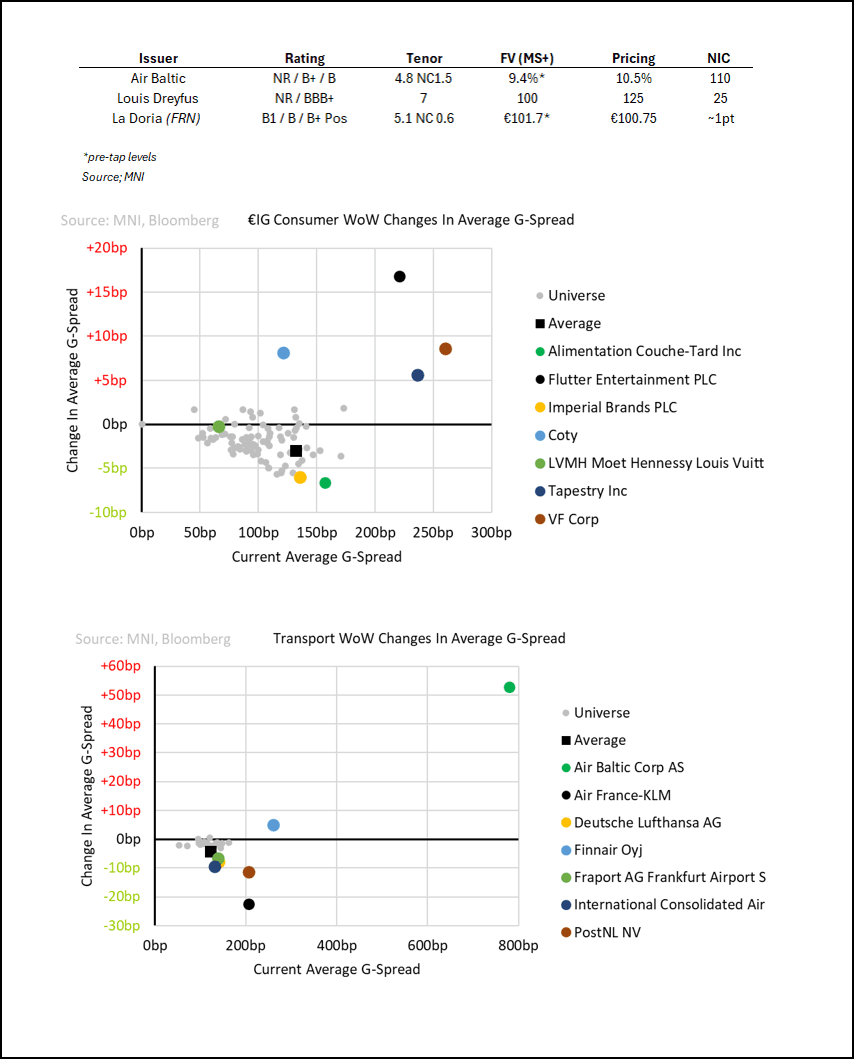

We had the first luxury and staffing companies report this week - both missed exposing some peer credit curves that are not positioned for weakness. One would be forgiven for looking at Burberry equities vs. VFC bonds and reaching the conclusion LVMH missed on US or Europe – that was most not the case but valuation thoughts ahead of both reporting seem to be taking over. Walgreen boots didn’t disappoint; bringing +1pt/>10% vol is becoming the norm for it. Primary was surprisingly interesting; Air-Baltic coming out for a tap ahead of earnings while Louis Dreyfus did not get the Cargill treatment. Macro remains firm with US nominal control group retail sales at +0.7% (prev. +0.3%) and UK ex. fuel real +0.3% (prev. +1%) – numbers to keep in mind when companies report poor earnings on only weak macro.

(links to notes in weekly pdf that will follow)

Fundamentals linked news

- LVMH finally giving into weaker Chinese consumer after an impressive post-covid run in growth. It has some different thoughts on how to manage the weak environment vs. peers

- Auchan; given the ongoing volatility we had a chat with the company on core questions we had

- Walgreen Boots earnings were a mixed bag leaving it net credit neutral in our eyes. Given euro 26s were heading in wide, some support on the lack of a large miss

- Manpower kicks off staffing earnings on a sour note. We reiterate caution for peer curves that are trading tighter

- Rentokil reported better than expected 3Q results, but FY guidance is unch from last month’s profit warning. High cash-price lines have been left wider than fundamentals are implying

- Burberry; resilience from equities and sterling 30s likely a sign of valuations finding a bottom; we are not as optimistic and still see better rotations in credit

- Coty trims sales expectations after a small 1Q miss but keeps EBITDA guidance unchanged. We do still see the beauty operator as a rising star and investors who agree are likely to see value on any widening

- Flutter faces earnings hit if leaks on UK doubling gambling taxes (with a focus on online gaming) prove to be true. We do see leverage impact, but short of rating impact for now. Latter is in the hands of the company that has ample free cash flow to manage the balance sheet.

- Lufthansa CEO’s continuing pessimistic remarks on the market environment make us nervous heading into earnings. We do seem to have passed the window for a profit warning - if so breaking this year’s theme

Event Driven Movers

- Alimentation Couche-Tard seems fixated on buying 7-11 despite the target reporting poor earnings and taking more defensive measures last week. The management, including founder Alain Bouchard, have flown to Tokyo – even without 7-11 agreeing to a meeting. We may be in for multi-tranche, currency and even multi-year supply if this closes. 7-11 equities are not confident and pro-forma IG rating target reiterated by management this week.

- Essity bondholders finally give formal notice of their view that an event of default had occurred after the ~€1.7b Vinda stake divestment in late 2023. The claims are on the low-cash price 29, 30 and 31s and from “a minority part” of total outstanding. Company seems to be standing firm. It seems bonds pre-empted it; they were moving off recent wides and back tighter this month.

Primary (fundamentals linked, levels below)

- Louis Dreyfus, €40m Air Baltic tap, €125m La Doria FRN tap

Rating Actions

- Wizz Air (Ba1/NR/BB+); Fitch junks Wizz ahead of earnings. The 26s trading past it seems to echo our sentiment on levels

- Deutsche Bahn (Aa1/AA- Pos/AA+); Moody’s follows S&P’s overly optimistic comments with more measure. It is still net positive on the prospect of more hand-holding from the German government

- French Sovereign (Aa2/AA-/AA- Neg); Fitch moves to negative outlook; La Poste has direct uplift while Aeroports de Paris and Air-France should be unaffected despite the partial government ownership

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Equities Roundup

- Stocks clung near steady to modestly mixed levels Wednesday, inside session ranges as markets await today's FOMC policy announcement. The DJIA trades down 60.87 points (-0.15%) at 41543.94, S&P E-Minis down 5.5 points (-0.1%) at 5696, Nasdaq down 8.4 points (0%) at 17627.84.

- Information Technology and Consumer Discretionary sectors led gainers in the first half, hardware and semiconductor makers supporting the IT sector: Super Micro Computer +2.07%, Apple +2.0 while Enphase gained 1.31%.

- The Consumer Discretionary sector led by a mix of stocks: GM +2.33% after announcing EV customer access to Tesla's supercharge network. Meanwhile, Deckers Outdoor gained 1.72%, Carnival Corp +1.66%.

- On the flipside, Materials and Finance sectors underperformed in the first half, chemical makers weighing on the former: Avery Dennison -2.75%, Albemarle -2.44%, Lind PLC -0.96%.

- Meanwhile, financial services shares weighed on the Finance sector with American Express -1.27%, Synchrony -1.26%, Visa -0.88%.

FED: Two Former Regional Fed Presidents In 25bp Cut Camp

Speaking on CNBC, two former regional Fed Presidents have lent support to the argument for the Fed to cut by 25bps starting today, both of whom tended to be at the more hawkish end of the FOMC in their tenures.

- Former St Louis Fed’s Bullard said the Fed should cut by 25bps today and signal 25 at subsequent with the case for a 50bp cut being overblown.

- “Lots of things looking pretty good about the economy so I just don’t think it’s the kind of situation where you have to go 50,”

- He’s been followed more recently by former Cleveland Fed’s Mester as seeing a good case for doing a series of 25bp cuts, but acknowledging it as being a really close call.

US TSYS: US TSY 17W AUCTION: NON-COMP BIDS $593 MLN FROM $60.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $593 MLN FROM $60.000 BLN TOTAL