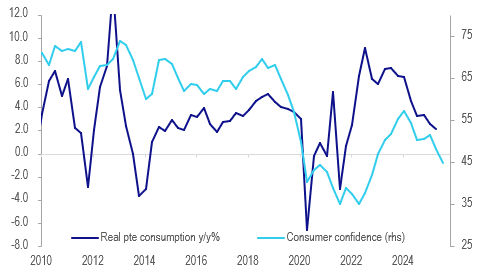

THAILAND: Consumer Confidence Weakens Further Signalling Slower Spending

Thailand’s University of the Thai Chamber of Commerce consumer confidence index fell to 50.1 in August from 51.7, around neutral. Economic conditions declined 1.5 points to 44.1, signalling that private consumption growth slowed further in the quarter. Political uncertainty likely added to pessimism regarding the economy, as former PM Paetongtarn was suspended on July 1 but wasn’t officially removed until August 29. The new PM has promised elections within four months and so political instability looks likely to continue for now.

- Both consumer expectations and the present situation deteriorated in August to 57.3 from 58.9 and 35.4 from 36.7 respectively.

- Real household expenditure growth peaked in Q3 2022 at 9.2% y/y and has been slowing since. It moderated to 2.1% y/y in Q2 this year from 2.5% y/y in Q1 and 3.4% y/y in Q4 2024.

- July private consumption fell 0.2% m/m, third consecutive monthly seasonally-adjusted decline, bringing the annual rate to -0.3% y/y, the first contraction since November 2021.

- The strong baht has weighed on the important tourism sector with arrivals down 15.9% y/y in July, the largest decline since the pandemic.

- Employment remains soft falling 0.9% y/y in July. The jobs component of consumer confidence fell 1.6 points to 48.3 in August, while future income was down 1.6 points to 58.0.

Thailand consumer confidence vs consumption y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

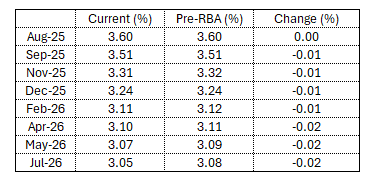

STIR: RBA Dated OIS Slightly Softer After RBA Cuts 25bps

RBA-dated OIS pricing is flat to 2bps softer across meetings after the decision, with mid-2026 leading.

- A 25bp rate cut in August was given a 97% probability.

- A cumulative 36bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Subdued Session Ahead Of US CPI Data

NZGBs closed little changed after trading in narrow ranges on a data-light day.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- (MNI) The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Swap rates are unchanged.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- July card spending is out tomorrow and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June.

- RBNZ dated OIS pricing is unchanged across meetings. 23bps of easing is priced for August, with a cumulative 40bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.

AUSSIE BONDS: RBA Cuts As Expected, Limited Reaction

ACGBs (YM -0.5 & XM -1.0) are moderately richer after the RBA cut the cash rate by 25bps to 3.60%.

- The Board noted that inflation continues to moderate toward the 2–3% range. Trimmed mean inflation fell to 2.7% and headline inflation to 2.1% in the June quarter. Domestic demand is gradually recovering, household incomes have risen, and labour market conditions, though easing, remain tight.

- With 75bps of cuts this year, the Board remains cautious but ready to respond to shifts in global or domestic conditions, maintaining its focus on price stability and full employment.

- Cash ACGBs are 1-2bps richer after the RBA decision, with the AU-US 10-year yield differential at -2bps.

- Swap rates are 2-4bps lower after the decision, with the 3s10s curve steeper.

- The bills strip has richened since the decision but sits flat on the day.

- RBA-dated OIS pricing is flat to 3bps softer across meetings after the decision, mid-2026 leading. A 25bp rate cut in August was given a 97% probability today. A cumulative 36bps of easing priced by year-end.

- Tomorrow, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.