EU CONSUMER CYCLICALS: Consumer & Transport: Week in Review

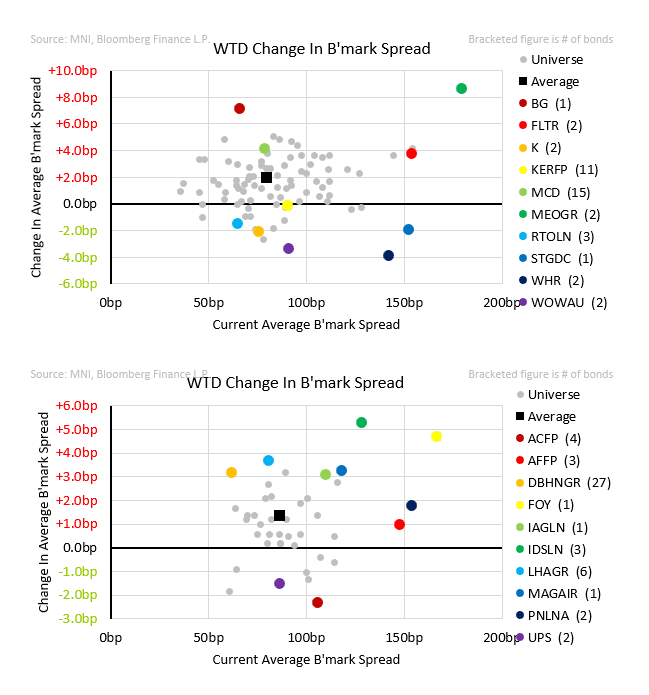

HY tightening was not enough to support IG – nerves on the doorstep of earnings perhaps stopping the blatant compression we often see. The few that did manage tightening include Kellanova, Woolworths and Norway and Milan airports – all levels we have flagged as interesting in the past. Equally mid-single digit widening from McDonald’s, IDS and Manchester airport has our interest to end the week. On earnings, the largest F&B and Luxury names both delivered firm results painting a supportive backdrop. Numbers to watch for next week include Bunzl, Edenred, Kering, Carrefour, Rentokil, DSV, and Groupe SEB.

- Suedzucker issued a trading update only a week after earnings, offering no incremental detail, and followed with a “correction” the next day — again with no value-add. It continued to reflect a somewhat poor ability to provide accurate guidance and reporting clarity.

- Pernod Ricard reported rough numbers, pointed to several one-offs on the call, but we still viewed the results as weak net of those. Guidance remained open-ended. Equities rose +6% during the week, albeit from a very low base.

- Nestle delivered a strong Q3 sales print for the new CEO’s first earnings. Combined with aggressive job cuts and upbeat Q4 guidance, equities rallied +11%. New issues had traded heavy into the print.

- Levi equities finished -13% last week despite the 3Q beat. Management reiterated the weak 4Q guidance baked in macro conservatism.

- IDS faced a larger £21m fine for missing delivery targets. Thresholds had been relaxed under USO reforms but still sit above historically achieved levels.

- Edenred / Pluxee: French government officials confirmed plans for an 8% employer levy on CSE-funded benefits, partially eroding the existing tax shield employers enjoyed.

- Air France 26s widened and triggered us to remind markets that there is a likely SLB step at maturity.

- We noted the no-cost rotation to avoid Alcohol (vs. F&B) in Euro credit confusing as moderation in consumption trends persist globally.

- LVMH reported nearly all regions and all segments improving vs. last quarter. An improvement to growth in mainland China was the main driver of the surprise, but we remain cautious on read-through noting the extraordinary store opening it had in China and still negative y/y Chinese cluster spend.

- FDJ reported lacklustre results on higher gaming taxes in France and ongoing UK/Netherlands online weakness. FY guidance was narrowed with a stabilisation expected in latter as it rolls over easier comps.

- No Primary

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

IMF: NY Post-Bessent Chief Of Staff Set To Become Seniormost US Off. At IMF

The New York Post reports that, according to its sources, US Treasury Secretary Scott Bessent's chief of staff, Dan Katz, is set to leave the administration to take up the post of first deputy managing director of the International Monetary Fund (IMF). Speaking on the sidelines of the IMF and World Bank spring meetings in Washington, D.C., earlier this year, Bessent criticised both organisations, claiming that “mission creep has knocked these institutions off course".

- Bessent argued the IMF has the mission of "promoting global monetary cooperation and financial stability", but instead is focused on progressive social issues. Bessent: "The IMF and World Bank serve critical roles in the international system. And the Trump Administration is eager to work with them — so long as they can stay true to their missions.”

- If appointed, Katz would become the seniormost US official at the IMF, second only to Managing Director Kristalina Georgieva. Historically, the IMF has always been led by a European, while an American has served as president of the World Bank, although this is not a formalised split. The appointment of a senior Trump administration figure to such an influential role at the IMF would draw attention towards the global lender of last resort.

EUR: EURCAD hits a fresh 16yrs High

- Just a 19 pips swing for now in the USDCAD, initially fell but remains fairly close to where it trading at pre decision.

- The one to watch is the EURCAD that did managed a new 16yrs high, highest since July 2009.

- Immediate resistance is still right here at 1.6330, this was the June and July 2009 highs.

(Chart source: MNI/Bloomberg Finance LP).

BOC: Statement Comparison - Sept 2025 Vs July 2025

A comparison of September's rate announcement vs prior (July) in link below: