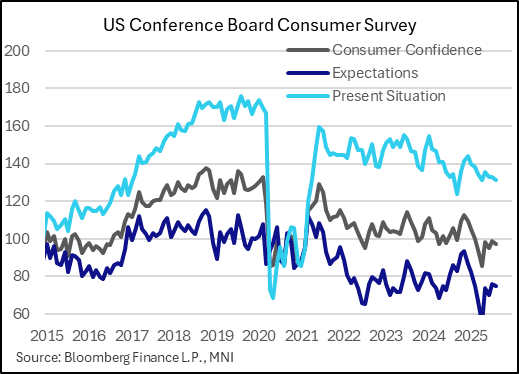

US DATA: Conf Board Consumer Sentiment Remains Subdued Amid Job Pessimism

The Conference Board's September survey showed a bigger weakening in consumer sentiment than had been expected. The headline reading fell to 94.2 (96.0 expected, 97.8 prior rev from 97.4), with present situation falling to 125.4 (132.4 prior, rev from 131.2) and expectations to 73.4 (74.7 prior rev from 74.8).

- These readings are mostly improved from the 2025 lows during the height of uncertainty over government tariff policy, but remain very weak on a historical basis.

- "Present situation" is just 0.1 point off the April low. Indeed the readings don't show any evidence of improvement across any major category of consumer despite the federal tax cut bill in July and less uncertainty over the tariff outlook.

- The deterioration also hasn't been as severe as in the University of Michigan survey. But either way, poor consumer sentiment hasn't really translated into actual consumer spending activity (real PCE is running at a 2-3% annualized clip in Q3), so we take the results with some caution.

- We did however note this mention of poor job conditions in the report: "Among consumers’ write-in responses, there was a rise in mentions of jobs and employment to a level unseen since August 2024. The comments were mostly negative, especially when referring to the current situation; there were a few positive comments which mostly conveyed hopes that things would get better." As we noted separately, the "labor differential" in this report hit a cycle low, indicative of consumers perceiving a weaker jobs market.

- Other concerning findings: "consumers’ views of their current financial situation recorded the largest one-month drop since we started to collect this data in July 2022. The share of consumers thinking that a recession is very likely over the next 12 months rose slightly in September, to the highest level since May. In addition, more consumers thought that the economy was already in recession."

- Buying plans for cars, services (especially travel-related) deteriorated, though there was little change in intentions to buy big-ticket items, and home purchasing plans rose to a 4-month high (mirroring the pullback in mortgage rates since August, we note) to relatively normal levels.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: S&P Upgrades Portugal To A+ From A

S&P has upgraded Portugal's long-term credit rating to A+ from A, with a stable outlook (had been positive).

- This is the 7th S&P upgrade for Portugal, from a low of BB in 2012-15. Only four ratings are higher (AA-, AA, AA+, AAA). This is the same rating as Slovakia, and just above Spain (A) per S&P.

- Per Bloomberg: "*S&PGR UPGRADES PORTUGAL TO 'A+' ON LOWER DEBT; OUTLOOK STABLE"

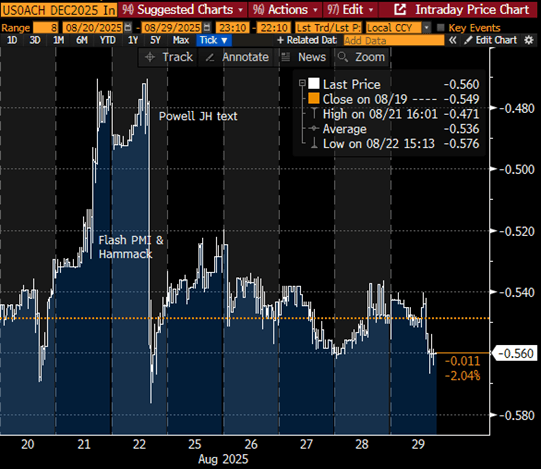

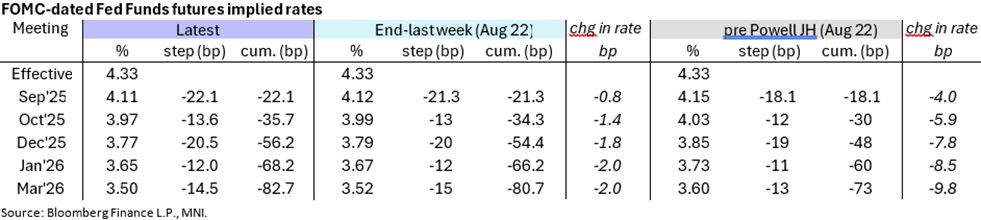

STIR: Still Eyeing September And December Cuts

With few market-moving data points this week, implied Fed rate cuts essentially held onto their post-Jackson Hole upward repricing, adding a couple of basis points of easing for good measure heading into the Labor day weekend.

- Indeed, the lack of movement is somewhat remarkable given this week's extraordinary "firing" of Fed Governor Cook, which is currently being fought out in the courts. In all it probably added to the dovish tone on the near-term rate outlook post-Jackson Hole but not substantially so, at least so far.

- The current path sees a September rate cut priced with nearly 90% implied probability, with 56bp of cuts through end-year (a cumulatively priced second cut in December) and 83bp through March 2026 (3+ cuts).

MACRO ANALYSIS: MNI US Macro Weekly: One Week, Two Labor Days

We've just published our latest US Macro Weekly - Download Full Report Here

- A busy pre-holiday week for data brought mixed economic signals and little net change in Fed easing expectations, putting next week’s labor day – Friday with its nonfarm payrolls report, of course, with apologies to Monday’s federal holiday – in focus for the FOMC and market participants alike.

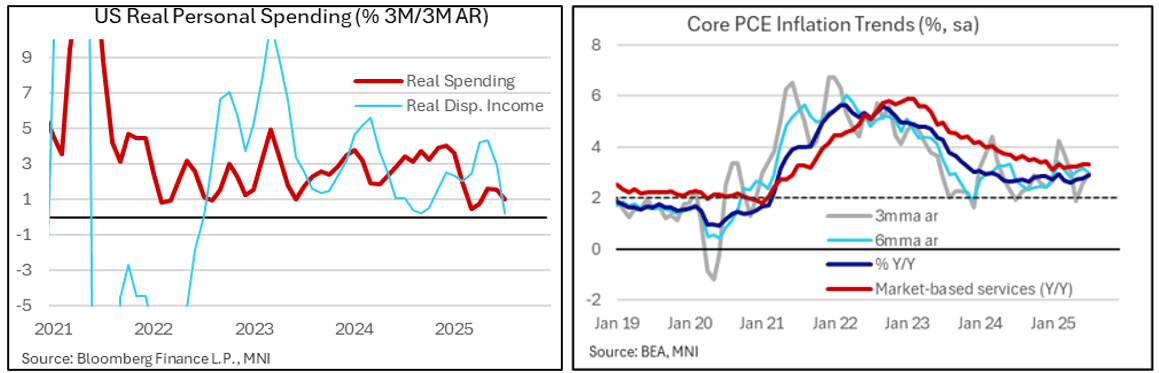

- Second-quarter GDP was revised up by more than expected in the second reading, to 3.3% Q/Q SAAR, driven by better-than-previously estimated domestic demand but still leaving 1st half growth in slightly weaker territory vs last year. That said, the Atlanta Fed's Q3 GDPNow estimate jumped to 3.47% (though the implied contribution from net exports in the quarter looks somewhat dubious, as we explain).

- The other major release of the week was July's Personal Income and Outlays report, which showed a modest uptick in income and spending on the month. However, the broader trends remain mixed at best, as real disposable income growth remains soft and services consumption is failing to regain traction.

- Core PCE inflation was close to expectations in July as the Y/Y accelerated to 2.9% for its fastest since February as it moves further away from recent lows of 2.6% having stalled above the 2% target. Recent trend rates are a little hotter but the median FOMC member will still need to see a further acceleration to meet their 4Q25 forecasts from June.

- Labor data were mixed. Latest jobless claims were in line to slightly better than expected, with initial claims trending a little higher but still impressively low whilst continuing claims are broadly plateauing after sharper increases in 1H25. But within the Conference Board consumer survey, the labor differential edged lower again, suggesting a continued upward trend in the unemployment rate.

- Elsewhere: regional Fed activity surveys were individually mixed, but combined generally showed an improvement in both manufacturing and services activity albeit with continued upside price pressures.

- Consumer sentiment (UMichigan and Conference Board surveys) and housing activity remained soft.

- Apart from Gov Waller again making the case from rate cuts, other FOMC colleagues who commented this week were a little more guarded when it came to the need for easing, to our ear.