PERU: Concern Expressed About Further Pension Fund Withdrawal

Sep-25 13:14

- Following the recent approval by Congress of a new pension withdrawal bill, the Lima Stock Exchange has voiced its concern that repeated and large-scale withdrawals could undermine the stability of the pension system and threaten retirees’ financial security. In addition, it said that the plan poses risks to the capital market, since pension funds are major investors in financial instruments and infrastructure projects.

- As a reminder, this is the country’s eighth pension withdrawal in recent years, with the bill approved by Congress earlier this month allowing workers to withdraw up to $7.5bn from private pension funds.

- Writing on this recently, Scotiabank noted that this withdrawal would potentially lower total AFP AUM to PEN 95bn, compared with nearly PEN 230bn in AUM had none of the eight withdrawals taken place. The shrinking of the private pension fund system, they write, also means that the job private pension funds have played in local financial markets has become "severely impaired, reducing the role that AFPs have had in providing liquidity and breadth to markets.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US Q2 FHFA HPI Q/Q SA -0.0% V +2.9% Q2 2024

Aug-26 13:00

- MNI: US Q2 FHFA HPI Q/Q SA -0.0% V +2.9% Q2 2024

MNI:US JUN FHFA HPI SA -0.2% V -0.1% MAY; +2.6% Y/Y

Aug-26 13:00

- MNI:US JUN FHFA HPI SA -0.2% V -0.1% MAY; +2.6% Y/Y

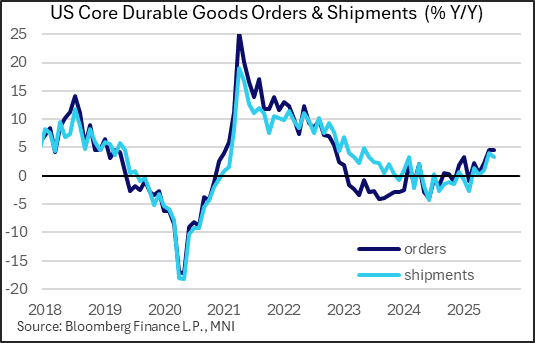

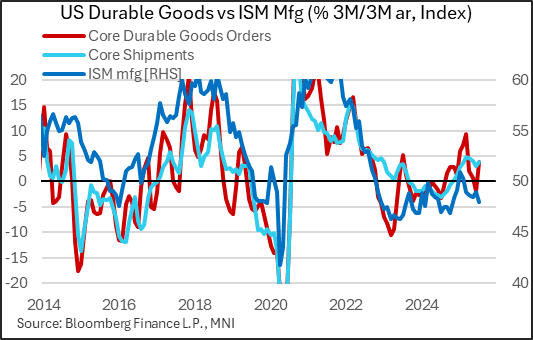

US DATA: Solid Start To Q3 For Durable Goods Activity

Aug-26 12:57

Durable goods orders showed a pickup in July, with better revisions casting a slightly better light on goods production and business equipment investment this summer.

- Headline durable goods orders bested expectations at -2.8% M/M (-3.8% expected, -9.4% prior), weighed down once again by the extremely volatile nondefense aircraft orders category (-33% M/M, after -53% prior).

- A better signal came from durable orders ex-transportation, which rose 1.1% (0.2% expected) after 0.3% prior. And the key core capital goods orders (nondefense, ex-aircraft) category also rose by 1.1% M/M (0.2% expected), more than reversing June's decline (-0.6%, upwardly revised from -0.8%).

- Meanwhile, core shipments continued to hum along, rising by a 27-month high 0.7% M/M (0.2% expected, 0.4% prior rev from 0.3%).

- Zooming out, core capital goods orders are nor rising at a 3.8% 3M/3M annualized pace, the strongest since March at which point activity was seen to be heavily influenced by tariff front-running.

- The Y/Y NSA figure may tell a clearer story, and it's a positive one: core orders have risen 4.4% Y/Y by that measure for two consecutive months, the best seen since Q4 2022.

- Category-wise, there was strength pretty much across the board, with metal products, machinery, computers/electronics, and electrical equipment/appliances/ components, and motor vehicles and parts all seeing a rise in new orders (we exclude volatile aircraft).

- One note of caution here is that the figures are in nominal dollar terms and thus may be reflecting a bottoming out of goods / components prices in addition to orders volumes. But momentum appears to be headed back in a positive direction, at least tentatively.