AUSTRALIA DATA: Commodity Volumes Down, Exports To China Remain Weak

Apr-03 02:43

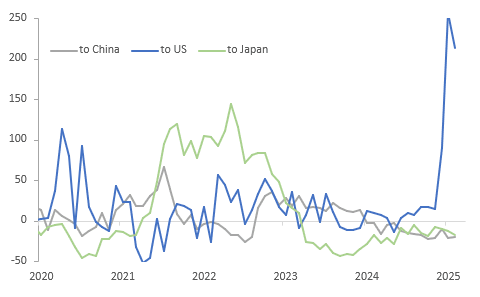

Australia’s merchandise exports remained soft to much of Asia while strong growth continued to the US and UK. There was a sharp rise in shipments to the US in Q1 as exporters aimed to beat the imposition of tariffs which take place from April 4.

- Australia will face the minimum universal 10% tariff, in line with Australia’s barriers to US goods according to Treasury calculations, with a possible ban on fresh beef in a tit-for-tat move.

- Exports to the US rose 213% y/y in February but the market accounted for only 4.6% of Australia’s 2024 exports worth less than 1% of GDP.

- The RBA this week didn’t seem concerned about the direct impact on Australia from US tariffs but was watching the effect on supply chains, and global & Chinese growth, Australia’s largest export destination, as well as any retaliatory measures. China will face 54% tariffs on its imports to the US.

- Australia’s goods exports to China fell 19.9% y/y in February, close to the October trough. Shipments to Japan fell 17.6% y/y and India was down 34.5% y/y due to lower gold purchases. Korea turned positive rising 6.7% y/y, NZ rose 4.8% y/y and the UK 64.7% y/y.

- Export volumes of Australia’s key commodities were lower in February, while unit values for coal and LNG were down but iron ore up. Quantities of coal were mainly driven down by India and Japan, while China and Japan bought less iron ore.

Australia goods exports y/y%

Source: MNI - Market News/ABS

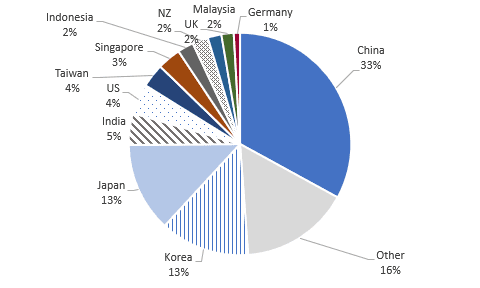

Australia goods exports by destination % total 2024

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Richer At Lunch Ahead Of 10Y Supply

Mar-04 02:41

At the Tokyo lunch break, JGB futures are stronger, +8 compared to settlement levels, after reversing overnight weakness.

- Outside of the previously outlined domestic data drop, there hasn't been much by way of domestic drivers to flag.

- “President Trump's latest criticism about a weak yen may be a good opportunity for Japan to think more seriously about how to fix the excessive depreciation of the yen, which has caused import-price inflation, says SMBC Nikko Securities strategist Makoto Noji.” (per BBG)

- Cash US tsys are 1-3bps richer, with a steepening bias, in today’s Asia-Pac session after yesterday’s solid gains.

- Cash JGBs are flat to 3bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 1.2bps lower at 1.402% ahead of today’s supply.

- This month, the 10-year auction offers an outright yield 10-15bps higher than last month but 7bps lower than its cyclical high of 1.466%. Additionally, the yield curve between 2- and 10-year bonds has steepened slightly compared to the prior month.

- Today’s auction is also likely to be supported by an improvement in sentiment toward global long-end bonds over the past two months. For instance, the US 10-year yield is roughly 65bps lower than its early January high.

- Swap rates are 1-3bps lower, with a flatter curve. Swap spreads are mostly tighter.

JGBS AUCTION: 10-Year JGB Supply Faces Higher Yield & Steeper Curve

Mar-04 02:36

The Japanese Ministry of Finance (MoF) will today sell Y2.6tn of 10-Year JGBs. This month, the 10-year auction offers an outright yield 10-15bps higher than last month but 7bps lower than its cyclical high of 1.466%.

- Additionally, the yield curve between 2- and 10-year bonds has steepened slightly compared to the prior month.

- Today’s auction is also likely to be supported by an improvement in sentiment toward global long-end bonds over the past two months. For instance, the US 10-year yield is roughly 65bps lower than its early January high.

- The relative affordability of 10-year JGBs versus futures— gauged by the 7- to 10-year spread — sits little changed relative to last month, after bouncing off the lower end of its range over the past year during the month.

- Amid this backdrop, it will be interesting to see if the current 10-year yield generates sufficient demand at today’s auction.

- Results are due at 0435 GMT / 1235 JT.

CHINA: Bond Futures Down as Markets Wait for NPC.

Mar-04 02:27

- Traditionally markets are quiet leading up to the National Party Congress and this year (despite the tariff threat impacting equity markets) bonds remain contained.

- The 10YR China bond future is trading flat today at 108.46, trending just below the 50-day EMA of 108.50 where it has been for several trading days.

- The 2YR China bond future is down by -0.03 at 102.64, trending back down towards the 200-day EMA of 102.63.

- Government bond yields are lower today with the CGB 10YR at 1.75% (-1bps).

- The CGB 10YR has traded in a tight range over the last week as bond markets await the outcome of the NPC with expectations growing for monetary policy and fiscal policy intervention to support economic growth.