EM LATAM CREDIT: Colombia: MNI BanRep Preview – Dec 2025

MNI Macro

- BanRep is expected to leave its policy rate unchanged at 9.25% for a fifth consecutive meeting on Friday, in another split decision, although risks of a hike have increased significantly amid mounting concerns over the inflation outlook.

- Rising inflation expectations, strengthening domestic demand and increasing fiscal pressures have prompted the majority of the BanRep Board to strike a more hawkish tone recently, with the market now pricing in over 150bp of rate hikes over the next year.

- For now, softer-than-expected CPI data this month give the Board some breathing space to wait for the outcome of 2026 minimum wage negotiations before year end.

The full MNI preview with analyst views is here: https://mni.marketnews.com/4qd8yTJ

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USDJPY Takes Out Key Resistance; Broadens Upside Range

- PM Sanae Takaichi is due to hold a meeting with Bank of Japan Governor Kazuo Ueda Tuesday. This will be the first in-person meeting since Takaichi came to office, and comes as tensions have surfaced between Takaichi’s government and the BoJ. Any perceived pressure being put on the BoJ will be closely scrutinised by markets. This applies especially as further JPY weakness would increase the likelihood for a December BoJ hike which may act counter to Takaichi's dovish fiscal stance.

- The minutes of the RBA's November policy meeting are due - at which comments concerning the labour market will be very closely watched. October employment change data more than doubled median expectations, with a shift to fulltime employment particularly notable - any acknowledgement that a stronger jobs markets could limit RBA easing ahead could have trigger AUD strength. Into the minutes release, AUDUSD is holding above the 0.65 handle, underpinned by the 200-dma support longer-term, last crossing at 0.6457.

- Resultantly, the JPY is the poorest performing currency Monday, while GBP and NOK trade more favourably. EURGBP trades either side of the 0.88 handle, erasing a small part of the recent rally up to 0.8865.

- Tuesday data schedule is light, with markets gearing for the now much-delayed September NFP print due this Thursday. The central bank slate is busier: ECB's Pereira & Dolenc are set to make appearances as well as BoE's Pill & Dhingra. Lastly, Fed's Barkin is due to comment on the economic outlook having not commented directly on policy since the last Fed decision. Barkin had previously seen less caution around the jobs market given the unlikely circumstance of broad layoffs given such a slow pace of hiring in recent years.

CANADA DATA: Cell Phone Inflation Drives Otherwise Soft Services CPI (2/3)

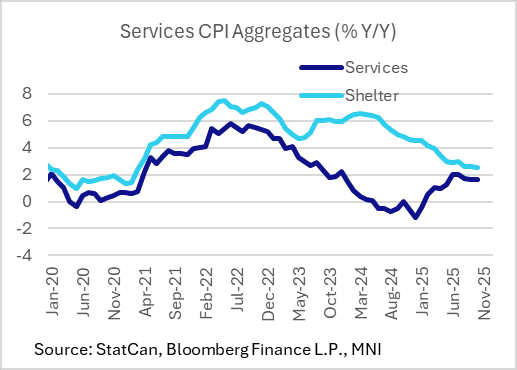

Underlying the steady core dynamics were a pickup in services prices alongside steady core goods prices - however the details were mixed beneath the surface.

- Overall, services prices saw a pickup to 3.2% Y/Y from 3.0% prior, for a 5-month high. Household operations (9% of the CPI basket, up 4.0% Y/Y after 3.1% prior for the highest reading in a decade) appeared to drive this increase, in turn by a 40+ year record rise in phone services driven by cellular prices (+7.7% for 1% of the basket). However, other categories were largely mixed.

- The most prevalent was shelter, which descended to a 2.5% Y/Y rate from 2.6% in the prior 2 months for a fresh post-March 2021 low. This came despite a pickup in rented accommodation inflation (5.1% after 4.7% for a 6-month high), with owned accommodation (2.0% after 2.1%) disinflating slightly as mortgage and homeowners replacement costs pulled back. The property tax CPI of 5.6% Y/Y (vs 6.0% in the prior 12 months) represented a disinflationary shift in this annual update but still an upside driver to overall CPI. Water, fuel and electricity saw a 0.5% Y/Y fall for a 4-month low, in large part due to the aforementioned drop in natural gas prices (-17.0% Y/Y).

- Elsewhere, transportation CPI was down to 0.7% Y/Y after 1.5%, offset in part by a pickup in recreation/education to a 7-month high 2.0% from 1.6%, while health and personal care was relatively steady at 2.5% (2.6% prior).

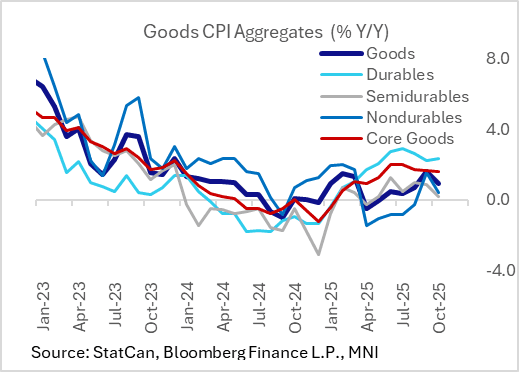

- Goods prices rose by 0.9% Y/Y, down from 1.6% prior, though it was notable that durable goods (2.3% after 2.2%) remained stubbornly strong even as we saw a sharp pullback in semidurables (0.2% after 0.9%) and nondurables (0.4% after 1.5%), which in part were due to softer food/energy prices.

- In sum, core goods prices were steady at 1.6% for a 2nd consecutive month.

- Highlighting the move lower in core: clothing and footwear prices saw a 0.3% Y/Y fall, after 4 consecutive positive months, while furniture and household equipment inflation fell to a 7-month low 0.3%.

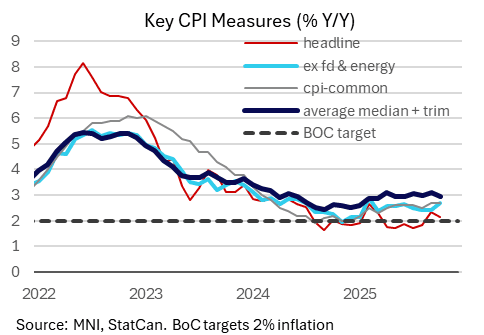

CANADA DATA: Core CPI Measures Stubborn Enough To Keep BOC On Sidelines (1/3)

Despite headline CPI printing more or less as expected in October, some core inflation measures were surprisingly stubborn compared with an elevated September. It's unlikely to have much bearing on BOC thinking on rates, with Governing Council already having signaled at the October meeting an indefinite rate hold. There were some worrying signs in "underlying" inflation by some metrics looks but overall they look to have remained around the BOC's estimate of 2.5%, suggesting little impetus to reconsider the policy stance on the basis of this release. That said, the stubbornness in core dynamics appears to have driven the market reaction which was to reduce implied chances of a December cut from slim (~5%) to none (<1%).

- October's non-seasonally adjusted headline CPI rise of 0.24% M/M was in line with expectations (0.2%). While this was up from 0.06% prior for a 3-month high, the dip to 2.16% in Y/Y from an unexpectedly-hot and 7-month high 2.36% prior will probably be the primary takeaway from a headline perspective (and the unrounded figure was more or less in line with the 2.1% consensus as we saw multiple 2.2% expectations).

- As widely-expected the key downside impact came from gasoline prices, which fell 4.8% M/M (and 9.4% Y/Y). (Natural gas prices also dropped sharply, by 11% M/M).

- However we also note a 0.6% M/M drop in October in grocery prices, which is bigger than the usual seasonal drop (and key in a category that has seen upward pressures in recent months). This helped cool the % M/M CPI SA reading: 0.12% was a 3-month low (0.43% prior).

- Outside of that though we saw strength in underlying metrics in various areas. MNI's "underlying" composite (averaging trim, median, ex-food/energy and CPIX) showed a rise of 2.8% on a 3-month annualized basis, which is the highest since June, but the longer-run 6-month measure dipped to 2.6% from 2.9% prior.

- Core (ex food/energy) CPI was revised up to 0.26% M/M from 0.19% prior, without which October's 0.26% would have marked a 5-month high. This drove the Y/Y rate to 2.69% Y/Y, a sizeable jump from 2.44% in each of the prior 2 months and marking the highest since February. The 3-month annualized rate rose to 2.6% (4-month high, 1.8% prior) with the 6-month steady at 2.4% (2.5% prior).

- Likewise the measure ex-8 most volatlie/indirect taxes ticked up to 2.94% Y/Y from 2.83% prior, a 26-month high, with the M/M reading coming in at 0.31% for a 2nd consecutive month. That meant the 3-month annual rate rose to a 4-month high 3.3% from 2.3% prior, though the 6-month rate moderated to 2.8% from 3.1% prior.

- The trim/median readings overall suggested softer inflation pressures. The closely-watched Y/Y readings averaged 2.95% (3.0% trim, 2.9% median) for a below-expected reading (3.00% consensus), in addition to a 0.05pp downward revision to prior (3.10%) and in line with BOC's 2.9% Q4 projection. This was a 4-month low in the average.

- The M/M SA readings of 0.23% trim / 0.14% median M/M marked a moderation overall vs 0.23%/0.23% prior (the average fell to 0.18% from 0.23% from a 13-month low). The 3-month annualized rate dipped to 2.6% from 2.7%, staying in the same recent range, but the 6-month fell to 2.6% from 2.9%, marking a 13-month low.