EM LATAM CREDIT: Colombia: Fitch Downgrade – Neutral

(COLOM; Baa3/BBneg/BB)

• Fitch cited large fiscal deficits, rising debt/GDP, escape from the fiscal rule and political constraints that are blocking revenue raising proposals, all of which have been expressed in market valuations. COLOM 8% 2035 were quoted equal yield of about 7.1% to much lower rated El Salvador (ELSALV; B3/B-B-) 2035s.

• COLOM 10-year notes were quoted at T+288bp, about 40bp wider since the completion of a USD4bn buyback of USD debt a month ago. Up to mid-November, spreads tightened 120bp since June 30th as the market absorbed other USD bond buybacks in August and September and suspended focus on fundamentals.

• Fitch projected a fiscal deficit of 6.5% of GDP in 2025, which would be slightly lower than 6.7% in 2024. The rating agency mentions the favorable accounting treatment of below par USD bond buybacks in reducing interest costs from 4.7% to 3.6% of GDP.

• Fitch estimated a primary fiscal deficit of 2.9% of GDP for 2025, higher than the 2.4% in 2024 and a key consideration when comparing to other similar rated countries with a median primary fiscal deficit of -.1%. Congressional rejection of the tax reform in plugging the COP16Tn budget funding gap was also cited. We addressed the likelihood of tax reform failing as well as the impact from mounting fiscal deficits and sticky inflation which has kept the Central Bank from cutting the policy rate in our post a few weeks ago: https://mni.marketnews.com/48Jw0AL

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: FTSE Put Spread

UKX (16th Jan) 9000/8450ps 1x2, bought for 1 in 2k.

US TSYS: Early SOFR/Treasury Option Roundup, Underlying Pares Gains

Treasury & SOFR option volumes rather modest overnight, underlying futures firmer - but scaling off recent highs ahead the NY open. Projected rate cut pricing appears steady to gaining slightly vs late Friday levels (*): Dec'25 at -10.2bp (-10.8bp), Jan'26 at -20.6bp (-20.9bp), Mar'26 at -30.5bp (-30.8bp), Apr'26 at -38.1bp (-37.4bp).

- SOFR Options:

- 4,000 SFRZ5 96.31/96.43 call spds

- Block 2,500 2QH6 97.12 calls, 8.0 vs. 96.755

- 5,000 SFRZ5 96.18/96.25/96.31 put flys ref 96.183

- 2,000 SFRZ5 96.18/96.31 call spds vs. 0QZ5 97.00/97.12 call spds

- 1,125 SFRZ5 96.00/96.06/96.12 put flys ref 96.183

- Treasury Options:

- 2,100 USF6/USG6 116 put spds ref 116-19

- 1,600 FVF6 108/108.75 put spds ref 109-09.25

- 3,500 TYF6 110/112 put spds ref 112-20

- 1,700 TYF6 114.5/115.5 call spds ref 112-18

CANADA DATA: Inflation Seen Softer In October, Big Surprise Needed For BOC Shift

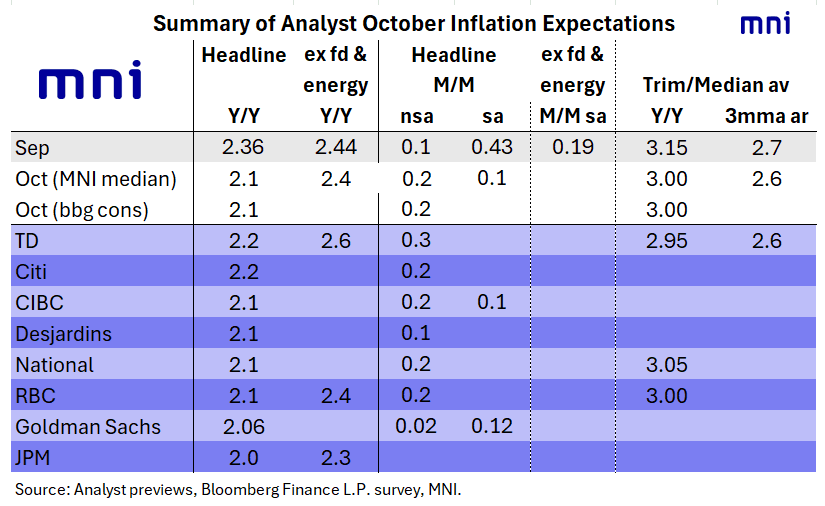

Re-upping our Canadian CPI (0830ET) preview note with updates sell-side forecasts - in short, inflation pressures are expected to have pulled back in October from September's 7-month high 2.4% Y/Y. Consensus (Bloomberg median) sees October CPI at 2.1% Y/Y (2.4% prior), with M/M at 0.2% (0.1% prior), while the average Median/Trim measure is seen at 3.00% (3.15% prior). MNI's analyst median suggests a skew to the soft side vs that - see table below.

- Some factors seen keeping a lid on inflation in October include Ottawa's removal of retaliatory tariffs on the US in September, as well as softer gasoline prices. Overall, core goods inflation is moderating with core services merely a little stickier, and it was largely food/energy inflation and downstream effects thereof that spurred the latest tickup in overall CPI.

- October's data are unlikely to change the Bank of Canada's assessment at the October meeting that "Looking at the full range of inflation indicators, Governing Council concluded that underlying inflation was still around 2½%" (they're looking at measures beyond the traditional trim/median these days). In any case they "acknowledged that year-over-year inflation would be choppy in the coming months" so would be likely to maintain the bias to hold rates for the foreseeable future even in the event of a downside surprise.

- That said there's under 2bp of cuts implied by the December meeting and just 7bp priced through the next 4 meetings, so an upside surprise here probably wouldn't do much for near-dated pricing.