EM LATAM CREDIT: Colombia Debt Management

COLOMBIA: Finance Ministry Completes Local Debt Swap, President Petro in Brussels

MNI Macro

• In a statement published overnight, the Finance Ministry said that it had swapped a total COP43.4t in local notes (TES), receiving COP 22.25tn of the notes in one auction, while delivering COP 17.47tn, and receiving COP 21.14tn in another auction, while delivering COP 17.9tn. It said that the swap, its largest yet, reduced debt by COP 8tn, while generating fiscal savings of COP 1.7tn for this year.

• Meanwhile, President Petro posted on X last night to say that the recent boat destroyed by the US in the Caribbean may have been a Colombian boat, with Colombian citizens on board. This comes at a time of heightened tensions with the US, which has seen Petro say recently that he will seek changes to Colombia’s trade deal with the US, after the US revoked his visa.

• Today, President Petro remains in Belgium where is participating in the Global Gateway Forum in Brussels, discussing investments and partnerships in global connectivity and clean energy, amongst other subjects. On the data front, the macro calendar remains clear, with the next scheduled releases being August retail sales and IP on Oct 15.

• The next BanRep MPC meeting is due on Oct 31, when a further rate hold is expected given the uptick in CPI inflation reported earlier this week and the central bank’s mounting concerns over the inflation outlook. The minutes to last month’s MPC meeting suggest that the bar to a resumption of the easing cycle has been raised even further, with many analysts now not expecting the next rate cut until Q1 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: SOFR Calls, Rate Cut Pricing Eases

Back to better SOFR call volume overnight into early NY trade even as underlying futures trade lower, Treasury options more mixed on lighter volumes. Projected rate cuts receding from late Monday (*) levels: Sep'25 at -27bp (-28.7bp), Oct'25 at -47.3bp (-49.6bp), Dec'25 at -69.2bp (-71.4bp), Jan'26 at -82.3bp (-85.1bp).

- SOFR Options:

- 3,000 96.25/96.37/96.50/96.62 call condors ref 96.36

- Block, 6,500 SFRZ5 96.62/96.75 call spds 1.75

- +2,500 SFRM6/SFRU6 97.50/98.25 call spd strip, 18.5

- 2,000 SFRZ5 96.37/96.43/96.50 call flys ref 96.355

- 2,000 SFRZ5 96.25/96.37 call spds ref 96.38

- 2,850 SFRU5 96.00/96.06/96.18/96.25 call condors, ref 95.985

- +5,000 SFRU5 96.00/96.12 call spds, 1.5

- +2,500 SFRZ5 95.81/95.93 put spds, 0.5 vs. 96.35/0.05%

- +5,000 SFRZ5 96.50/96.62/96.75/96.87 call condors, 1.5

- +10,000 SFRU5 95.93/96.00/96.06 call flys, 2.75

- 2,000 SFRU5 95.87/96.00/96.12 iron flys, 4.0 ref 95.99

- Block, +5,000 SFRU5 95.87/95.93/96.00 call flys, 2

- Block, +2,500 SFRU5 96.00/96.12 call spds, 1.25

- Block/screen, +4,000 SFRZ5 96.50/96.62/96.75/96.87 call condors, 1.5

- +6,000 SFRZ5 96.00/96.12 put spds, 1.75

- -2,000 0QU5 97.00/97.50 call spd vs. 2QU5 97.00/97.37 call spds, 2.0 net

- +5,000 SFRU5 96.00 calls, 1.75

- Treasury Options:

- 2,400 TUV5 104.75/105 1x2 call spds ref 104-14.25

- 2,400 FVZ5 110 calls ref 109-29.25

- 2,500 FVV5 109.75 puts, 17.5 ref 109-28.25

- 5,000 TUV5 104.25/104.5 call spds ref 104-14.88

- 5,000 TYV5 113.5/114 call spds ref 113-13

- +2,000 TYV5 111.75/112.75 put spds 13 vs. 113-08.5/0.08%

- +1,500 TYV 112/113 put spds, 15 vs. 113-16.5/0.23%

- +1,500 TUH6 104.62/105.25 call spds, 13.5 vs. 104-14.75/0.20%

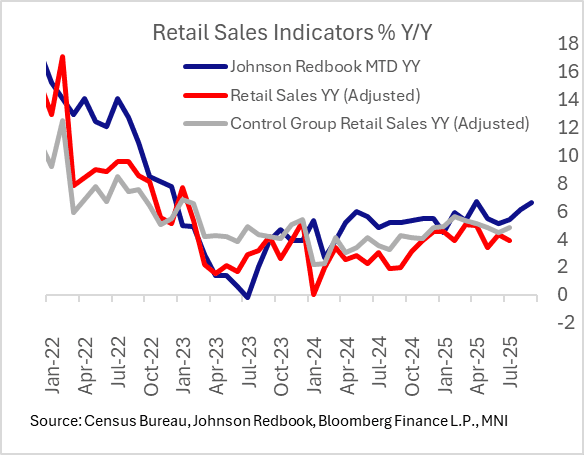

US DATA: Redbook Retail Sales Picking Up Through Q3

The Johnson Redbook Retail Sales Index rose 6.6% Y/Y in the first week of September (ending Sep 6), running a little above retailers' targeted 6.3% gain for the month.

- If sustained, this rate of sales would mark an acceleration from 6.1% in August and would be just below April's 6.7% for the 2nd-highest monthly growth since 2022.

- While reminding of the usual caveat that this is in nominal terms so may reflect ongoing tariff-related goods price inflation, the same can be said for Census Bureau retail sales data (for which the August release is on Sep 16, currently seen at +0.3% M/M for headline and 0.5% ex-auto/gas; the latter would imply the fastest Y/Y growth in 5 months at 4.9%).

- The anecdotal section of the report pointed to sustained retail demand going into the final month of the third quarter, notably with discount stores appearing to perform well. "Sales exceeded expectations in the first week of September, largely due to the Labor Day weekend, which brought in significant traffic early in the week. Both Sunday and Monday were particularly busy shopping days, marking the peak of this year’s back-to-school season. Shoppers responded enthusiastically to various Labor Day sales and promotions. Sales continued to be driven by the dual themes of back-to-school and seasonal apparel. Discount stores also reported strong food sales leading up to the long Labor Day weekend. While some retailers are approaching the end of their back-to-school calendar, others anticipate sustained momentum throughout the month, contributing to sales in electronics, children’s clothing, and school supplies."

MNI: US REDBOOK: SEP STORE SALES +6.6% V YR AGO MO

- MNI: US REDBOOK: SEP STORE SALES +6.6% V YR AGO MO

- US REDBOOK: STORE SALES +6.6% WK ENDED SEP 06 V YR AGO WK