LNG: Cold Winter Outlook Drives US Gas Up, Milder Europe Keeps It In Range

US gas continued to rise strongly driven by wintery weather across the east and forecasts for a cold season. Prices are now almost 10% higher this month and 21% since 17 October but is now flashing overbought. Production remains ample though to provide for increased heating consumption and robust demand for LNG exports. European prices continue to trade in a narrow range waiting for direction.

- Henry Hub rose 4.3% to $4.525 after reaching $4.581 off a low of $4.276. Not only has a cold snap hit the eastern US this week, but long-term forecasts for November to March have shifted cooler, according to Bloomberg. Temperatures for mid- and into the second half of the month have also been revised lower for the north and central US (Vaisala). Thus heating demand over winter is looking solid. BNEF data showed demand on Tuesday was up 20.1% y/y.

- European gas was little changed trading between EUR 30.83 and 31.180. The lack of direction is reflected by flat prices in November. The market is waiting for information on the outlook for winter and is stable while LNG imports remain strong but remains vulnerable to any supply disruptions.

- Storage in Europe is slightly lower at 82.4% having reached 83% last week. Near-term the weather shouldn’t cause a drawdown with temperatures above average over the second half of November, according to Bloomberg.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

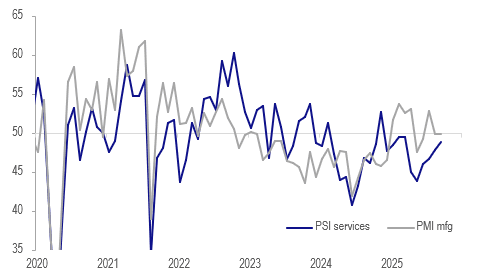

NEW ZEALAND: Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity

The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September up one point to 48.8, highest since March. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- The Q3 averages of the PMI and PSI show that there was some improvement in the quarter compared to Q2. Manufacturing rose 1 point to 50.9, slight growth, and services almost 3 points to 47.7, ongoing contraction.

- Forward-looking services orders rose to 51.4 from 47.8, the highest since November 2024. They continued to contract in Q3 overall at 48.6 but at a slower pace than Q2’s 45.5. Manufacturing saw an increase in orders in Q3 at 53.1 up from 49.5.

- Labour demand remained soft consistent with other data signaling a weak Q3 print on 5 November. September services employment fell to 47.8 from 48.7 with Q3 showing a further contraction in staffing at 47.6 (Q2 46.4). Manufacturing employment contracted too in the quarter.

NZ BNZ services vs manufacturing indices

Source: MNI - Market News/LSEG

JGB TECHS: (Z5) Bearish Trend Sequence Intact

- RES 3: 140.08 High Jun 13

- RES 2: 139.05 High Aug 4

- RES 1: 137.30 - High Sep 8 and key short-term resistance

- PRICE: 136.03 @ 15:44 BST Oct 10

- SUP 1: 135.61 - Low Oct 08

- SUP 2: 135.39 - 1.618 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

- SUP 3: 134.69 - 2.000 proj of the Aug 4 - Sep 2 - Sep 8 swing (cont.)

A bear threat in JGB futures remains present despite the intraday spike Monday. The contract pulled well off the intraday high, keeping the bias negative for now. The latest sell-off has also resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection. Key short-term resistance has been defined at 137.30, the Sep 8 high.

AUSSIE BONDS: Futures Surge At Open But Off Best Levels, Key Resistance Intact

Aussie bond futures surged at the open, as from late Friday we saw a sharp risk off move in the US. Trump's tariff threat against China drove safe have demand for US Tsys. For Aussie 3yr and 10yr futures, key short term resistance remains intact though.

- We sit away from best levels for Aussie futures, as softer language used by US officials today and by Trump this morning suggest scope for negotiations with China. US Tsys futures are down so far today, the 10yr off 5bps to 112-31.

- For 3yr futures in Australia we got to 96.495 earlier today, but now sit at 96.475, +7.5bps, while 10yr futures sit at 95.68, +6.5bps (earlier highs were at 95.7050). Near-term resistance to watch is 95.780, the Sep 12 high, while the 3yr future short-term resistance to watch is 96.615, the Sep 12 high.

- ACGB yields are around 6.5-7.5bps lower across the benchmarks, led slightly by the front end. The 3-10s curve was last around +80bps, holding within recent ranges.

- The AU-US 10yr spread is still threatening to break highs, last +26bps. A clean break above +30bps could see +40-45bps targeted for the spread, levels last seen in 2022. If US-China tensions don't de-escalate this spread may mean revert though, as Australian easing expectations could firm again if tariffs threaten the China growth outlook.

- The local data calendar is empty until tomorrow's Sep NAB business survey, along with the RBA policy minutes.