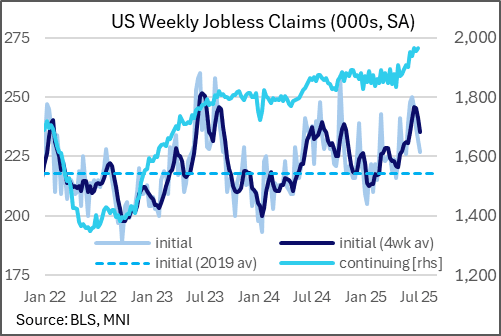

US DATA: Claims Data Reinforces "Low Firing, Low Hiring" Labor Market Theme

Jul-10 12:52

The latest weekly jobless claims report showed a further improvement in seasonally-adjusted initial claims, though the continued elevation in continuing claims kept the broader theme of a 'low firing, low hiring' labor market very much intact going into the second half of the year.

- Initial jobless claims were below expected at 227k (235k consensus, 232k prior rev from 233k) in the Jul 5 week. This was the 4th consecutive pullback from the recent high 250k in the Jun 7 week, with the current level now marking an 11-week low. The 4-week average fell for a 3rd consecutive week, to 236k, a 5-week low.

- Continuing claims were exactly in line at 1,965k (1,965k expected, prior rev from 1,964k) in the Jun 28 week. This was, by a mere 1k, the highest continuing print since November 2021.

- Overall continuing claims have pretty much steadied out between 1,900-2,000k (4 of the last 5 weeks were within a range of 1,951-1,965), with the advance seasonally adjusted insured unemployment rate in the 1.27-1.29% range over the past 5 weeks.

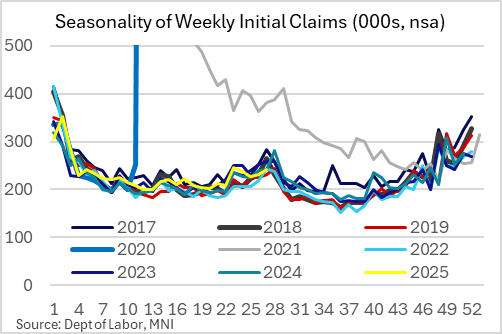

- So far as seasonal factors are concerned, initial NSA rose 10.0k, besting the seasonal factor expectation of a rise of 14.8k; there were no major standouts on a state-by-state NSA basis. Meanwhile continuing claims rose 6.1k NSA, with seasonal factors expecting a decrease of 3.9k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Gilt/Bunds Back Towards 200bp

Jun-10 12:49

10-Year gilts outperform Bunds by 5bp today, following the softer-than-expected UK labour market data.

- The spread is set for its lowest level since mid-May, last 201.1bp.

- Gilt bulls look to force a break back below the 200bp level, with a cluster of daily closing levels from late April through the early part of May then layered into 197.4bp.

- Longer term it is worth noting that May’s widening in the spread failed to break above April’s high (218.8bp), with the subsequent pullback leaving the spread just below the middle of the range witnessed since December.

- Relative fiscal and monetary stances are set to drive the spread over the longer run.

- Germany has already pledged meaningful fiscal loosening, while the UK’s fiscal fragility is well-documented and has resulted in a more active approach to issuance/liquidity management from policymakers in recent weeks (effectively shortening issuance WAM).

- A reminder that gilts are operating with a higher beta to U.S. Tsys than their German peers, which provides an extra layer of complexity given the volatile macro environment and recent swings in U.S. assets.

Fig. 1: UK/Germany 10-Year Yield Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

PIPELINE: Corporate Bond Update: US$ Issuer List Expanding

Jun-10 12:44

- Date $MM Issuer (Priced *, Launch #)

- 06/10 $750M Colonial Pipeline 8NC3

- 06/10 $500M PVH Corp WNG 5Y +160a

- 06/10 $500M CAF WNG Perp5.5 7.125%a

- 06/10 $Benchmark Experian Finance 10Y +110a

- 06/10 $Benchmark Omega Healthcare 5Y +160a

- 06/10 $Benchmark Lloyds 4NC3, 4NC3 SOFR, 11NC10

- 06/10 $Benchmark ANZ 3Y +60a, 3Y SOFR, 11NC10 +165a

- 06/10 $Benchmark M&T 3NC2 +105a, 3NC2 SOFR, 6NC5 +135a

- 06/10 $Benchmark Bahamas investor calls

US TSYS: US Tnotes is slowly ticking higher

Jun-10 12:42

- The US Tnotes isn't seeing much traction on the push higher today, although it is testing the session high, this has mostly been led by EGBs and the UK Gilt so far today.

- Looking at the TYU5 chart, a test back to 110.21 would mean a reversal of the US NFP sell off, but the contract did print a 110.29+ high last Friday during the earlier EU session, pre NFP.