LNG: China LNG Imports Rebounded in November and Higher Year on Year

China’s LNG imports rebounded to 6.94m tons in November and 13.6% higher on the year, according to General Administration of Customs data.

- LNG imports were the highest since Dec. 2024 and compared to 5.76m tons in October. Jan. – Nov. LNG imports fell 13.7% on the year to 60.01m tons.

- LNG imports to China are above last year’s levels as buyers take more shipments from long-term contracts, according to Bloomberg earlier this month. However Chinese demand for spot LNG cargoes remains weak amid strong inventories at major gas consumers and with amid demand, rising pipeline supply and domestic output this year.

- Pipeline gas imports increased by 7.9% compared to the same month last year to 5.01m tons and compared to 4.01m tons in October. Year to date imports rose 7.6% to 54.46m tons.

- China 30-day average daily LNG imports have risen to the highest since January at 232k tons on Dec. 17, according to Bloomberg ship-tracking data. Imports have net trended higher since a low of 156k tons in October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU-BOND SYNDICATION: 2.50% Oct-30 EU-bond tap: Spread set

- Spread set MS + 12bps (guidance was MS + 15bps area)

- Tap Size: E5bln (WNG) (MNI expected E5-6bln)

- Books in excess of E83bln (inc E6.75bln JLM interest)

- Settlement: 25 Nov 2025 (T+5)

- Maturity: 14 October 2030

- ISIN: EU000A4EG021 (immediately fungible)

- JLMs: GSBE SE / HSBC / J.P. Morgan (DM/B&D) / Natixis / UBS

- Timing: Books to close at 9:30GMT / 10:30CET

SONIA OPTIONS: Call Spread vs Put

SFIM6 96.65/96.75cs vs 96.15p, bought the cs for 0.25 in 4k.

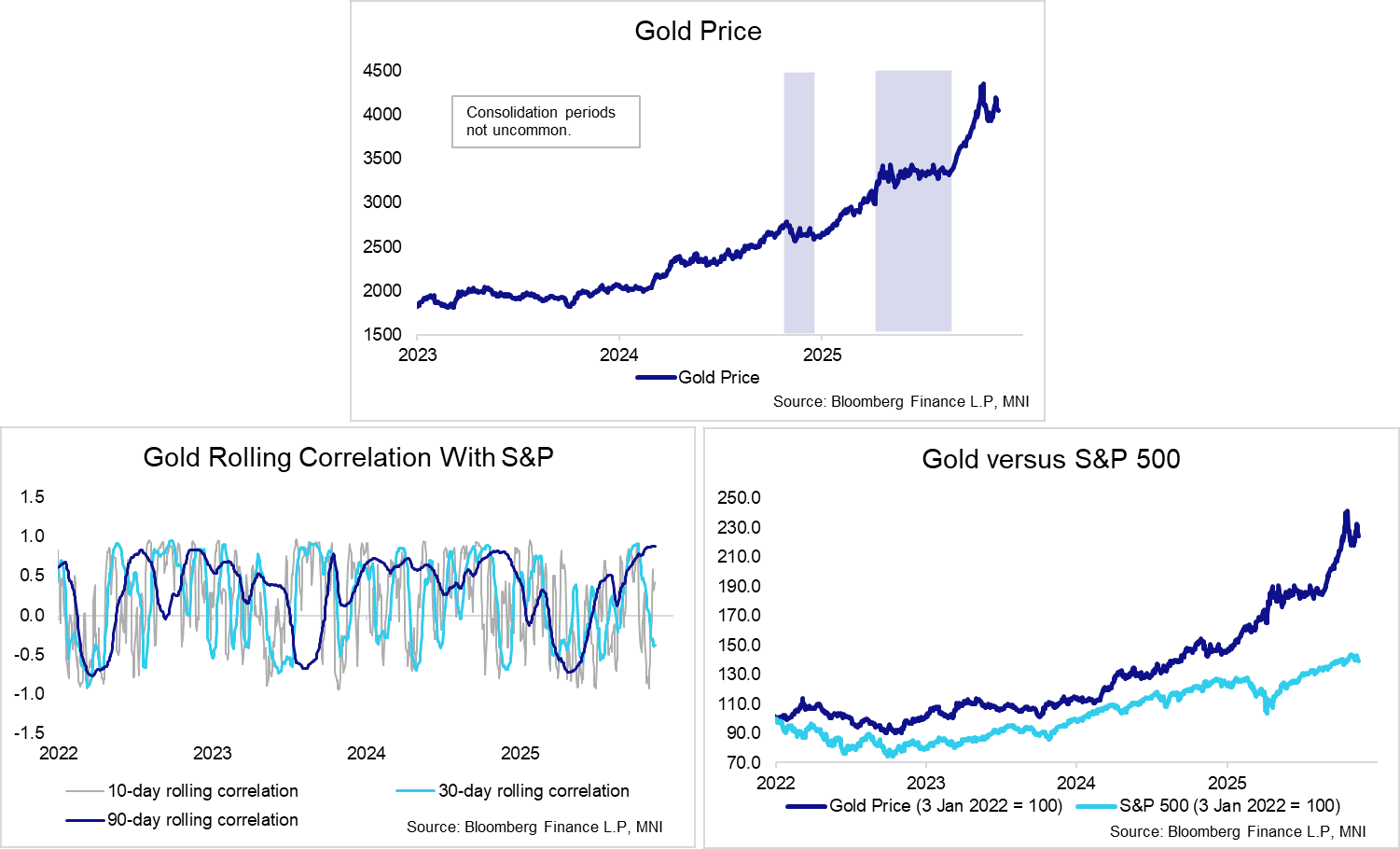

GOLD: 50-day EMA Support Still Intact, Consolidation Phase May Be Healthy

Gold has not acted as a risk hedge during the past week, with spot selling off alongside equities and narrowing the gap to key support at the 50-day EMA ($3,932 today). A clear break of this EMA would signal scope for a deeper retracement, exposing the Oct 28 low at $3,887 and round number support at $3,800. However, provided the 50-day EMA remains intact, a consolidation phase at current levels may be healthy for gold, and lay the groundwork for fresh extension higher. Longer-term bull themes such as central bank buying and debt monetisation continue to be favoured. Goldman Sachs estimate China added 15 tons of gold in September, well above the 1.24 tons officially reported (write-up per Bloomberg).

- In recent weeks, the combination of falling Fed rate cut expectations and a tightening of US liquidity conditions have worked against gold, spurring a fresh bout of profit taking/deleveraging after a solid rally through September/October.

- It’s worth remembering that Gold’s 90-day rolling correlation with the S&P has been positive for most of the last three years, save for isolated periods in early 2022, mid 2023 and Q2 2025 (the latter being Liberation Day fallout). Shorter-horizon rolling correlations are unsurprisingly more volatile.

- Through gold’s 100% rally since the start of 2024, consolidation periods and minor corrections have not been uncommon. Recall that price traded in a horizontal fashion in the four months from mid-April to mid-August.

- In their 2026 outlook, TD Securities write that “lower rates, continued tilt toward debasement narratives, along with supply side dynamics and asset managers looking for diversification are set to make gold, copper and crude oil perform above expectations”. Goldman Sachs still see gold at $4,900/oz by the end of next year.