EM ASIA CREDIT: China Huaneng Group (HUANEN): Final GUI

Nov-26 10:31

New Issue: USD benchmark PerpNC3

IPT: 4.7% area

FV: 4.2% area

Final GUI: 4.15% - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

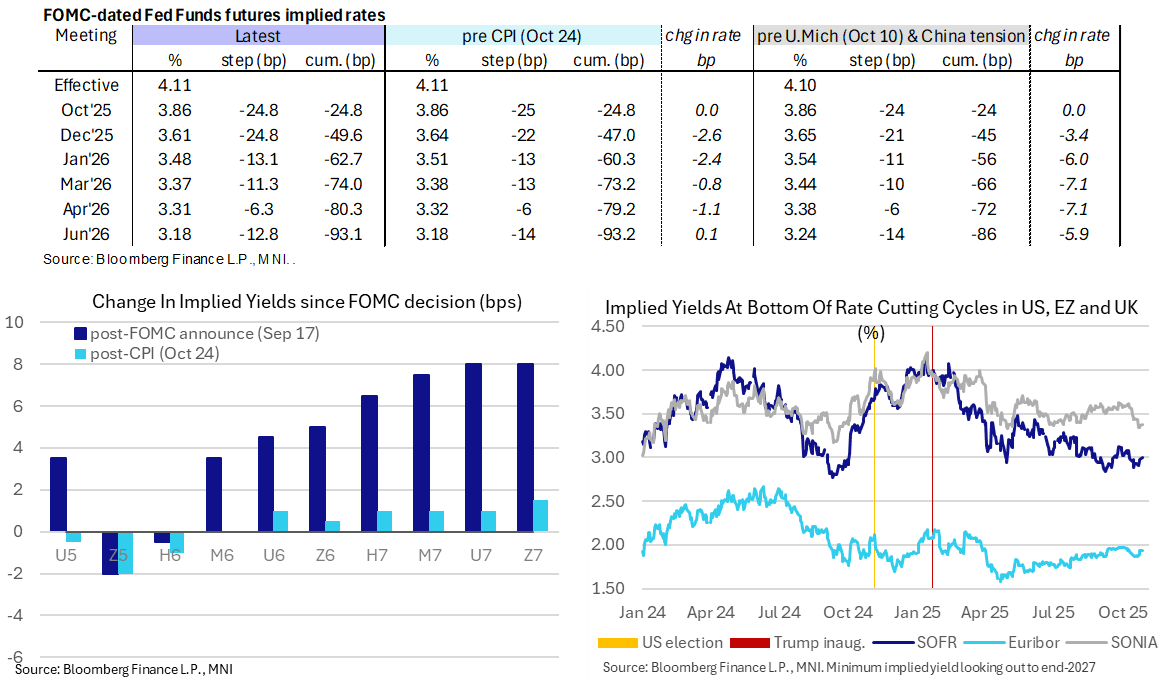

STIR: US-China Trade Deal Optimism Limits Dovish CPI Impact

Oct-27 10:31

- US-China trade deal optimism ahead of Trump-Xi meeting this week sees Fed Funds implied rates 1-2bp higher since Friday’s close, Wednesday’s decision aside where the Fed is still fully priced to cut 25bps.

- It’s seen these nearer term meetings reverse a large part of the dovish reaction to Friday’s CPI miss – see table.

- Cumulative cuts from 4.11% effective: 25bp for Wed, 49.5bp Dec, 62.5bp Jan, 74bp Mar, 80.5bp Apr and 93bp Jun

- Look beyond mid-2026 and SOFR futures are now a little lower than pre-CPI levels, albeit only just with a modest 1.5-2.5 tick decline since Friday’s close looking out to end-2027 contracts.

- The terminal implied yield is currently at 2.995% (SFRZ6) having last closed higher on Oct 9 prior to the initial flare-up in US-China trade tensions.

- MNI Fed Preview here: https://media.marketnews.com/Fed_Prev_Oct2025_6a6731f139.pdf with the analyst update to follow later today.

JAPAN: Moody's Affirm Japan at A1; Outlook Stable

Oct-27 10:29

"*MOODY'S RATINGS AFFIRMS JAPAN'S A1 RATINGS, MAINTAINS STABLE" - bbg

- "JAPAN RATING ACTION REFLECTS TRACTION ON REFLATION & FISCAL POLICY GEARED TOWARDS CONSOLIDATION

- DO NOT EXPECT RECENT LEADERSHIP TRANSITION TO SIGNIFICANTLY REVERSE JAPAN'S GAINS IN FISCAL CONSOLIDATION" - Reuters

LOOK AHEAD: Monday Data Calendar: Dallas Fed Mfg Activity, 2Y & 5Y Note Auctions

Oct-27 10:23

- US Data/Speaker Calendar (prior, estimate)

- 10/27 1030 Dallas Fed Mfg Activity (-8.7, -7.8)

- 10/27 1130 US Tsy $77B 26W bill & $69B 2Y Note auctions (91282CPE5)

- 10/27 1300 US Tsy $86B 13W bill & $70B 5Y Note auctions (91282CPD7)

- Source: Bloomberg Finance L.P. / MNI