INTERNATIONAL TRADE: China Exports To Vietnam Continue Surge Despite Levy Fears

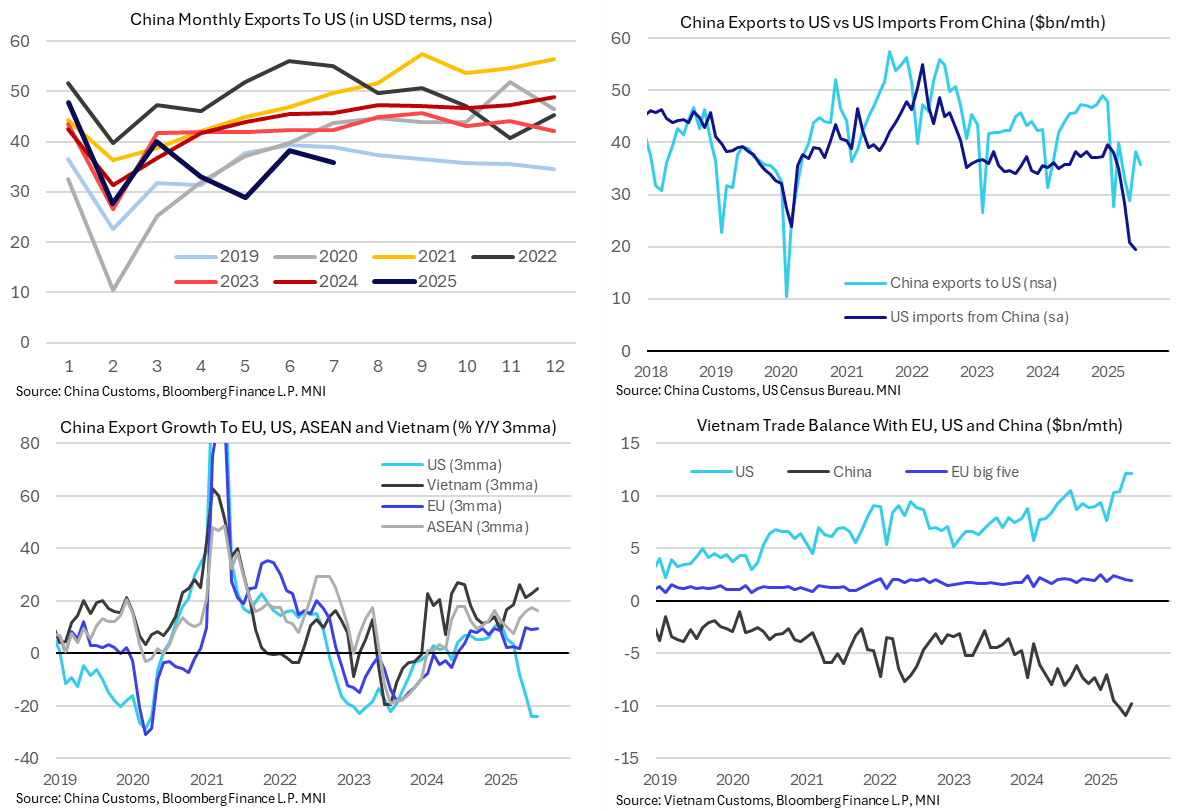

Latest China international trade data for July showed solid nominal export growth despite further heavy declines in shipments to the US at least on Y/Y terms. China exports to the US point to some stabilization in trade after May lows (although with further questions on differences between US accounting) whilst exports to Vietnam remain particularly strong in signs that fears over transshipment levies didn’t have an immediate impact.

- As noted overnight, China trade flows were stronger than expected in July as exports increased 7.2% Y/Y (cons 5.6) after 5.9% and imports rose 4.1% Y/Y (cons -1.0) after 1.1%.

- Export strength is being driven by Vietnam in particular at 28% Y/Y (25% 3mma), suggesting little impact at least immediately from fears of transshipments facing a 40% rather than 20% tariff rate under the US-Vietnam trade deal announced earlier in the month.

- It is admittedly early for any impact to show, especially seeing as Reuters today reported that “Tougher U.S. trade penalties on goods originating in one country being re-shipped from another are not expected to immediately follow new U.S. tariffs, three people in Southeast Asia with knowledge of the matter said, easing a major cause of concern.”

- Separate Vietnamese trade data shows trade from China to the US via Vietnam has been underway for some years but ramped up at the start of the second Trump administration in data up to June.

- Back to today’s China data, export growth to ASEAN countries more generally remains strong at 16.8% Y/Y (16% 3mma).

- Elsewhere, exports to the EU are still robust (9.3% y/y, 10% 3mma) with the latter suggesting similar rather than accelerated disinflationary pressures amidst European concerns of re-routing of excess supply.

- Exports to the US meanwhile continued to fall heavily, -21.6% Y/Y in July (-24% 3mma), and imports are declining almost as quickly at -18.6% Y/Y (-17% 3mma) as trade between the two remains constrained.

- In level terms, China exports to the US in non-seasonally adjusted terms at $36bn in July dipped from $38bn in June but were off the May low ($28bn). It compares to the $45.5bn of July 2024 which was broadly representative of the year as a whole when it averaged $43.7bn in 2024.

- There are increasing question marks when comparing with the US side of trade data, where US quoted imports from China have fallen more notably in data up to June (released Tue) to a seasonally adjusted $19.4bn vs $37bn averaged in 2024.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: Preview 3Y Note Auction

Tsy futures are near midmorning lows (TUU5 103-20.5, -.38 vs. 103-19.75 low) ahead of the $58B 3Y note auction (91282CNM9) at 1300ET, WI is currently at 3.881%, 9.1bp rich to last month's tail. Results will be available shortly after the competitive auctions closes at 1300ET.

- June auction recap: Treasury futures showed little reaction after $58B 3Y note auction (91282CNH0) tailed 0.5: 3.972% high yield vs. 3.967% WI; 2.52x bid-to-cover vs. 2.56x prior.

- Peripheral stats saw indirect take-up climb to 66.78% vs. 62.37% prior; direct bidder take-up retreated to 18.03% from 23.71% prior; primary dealer take-up 15.19% vs. 13.92% prior.

ITALY AUCTION PREVIEW: On offer this week

MEF has announced it will be looking to sell the following at its auction this Friday, July 11:

- E3.25-3.50bln of the new 3-year 2.35% Jan-29 BTP (ISIN tba)

- E3.00-3.50bln of the 3.25% Jul-32 BTP (ISIN: IT0005647265)

- E1.25-1.75bln of the 3.85% Oct-40 BTP (ISIN: IT0005635583)

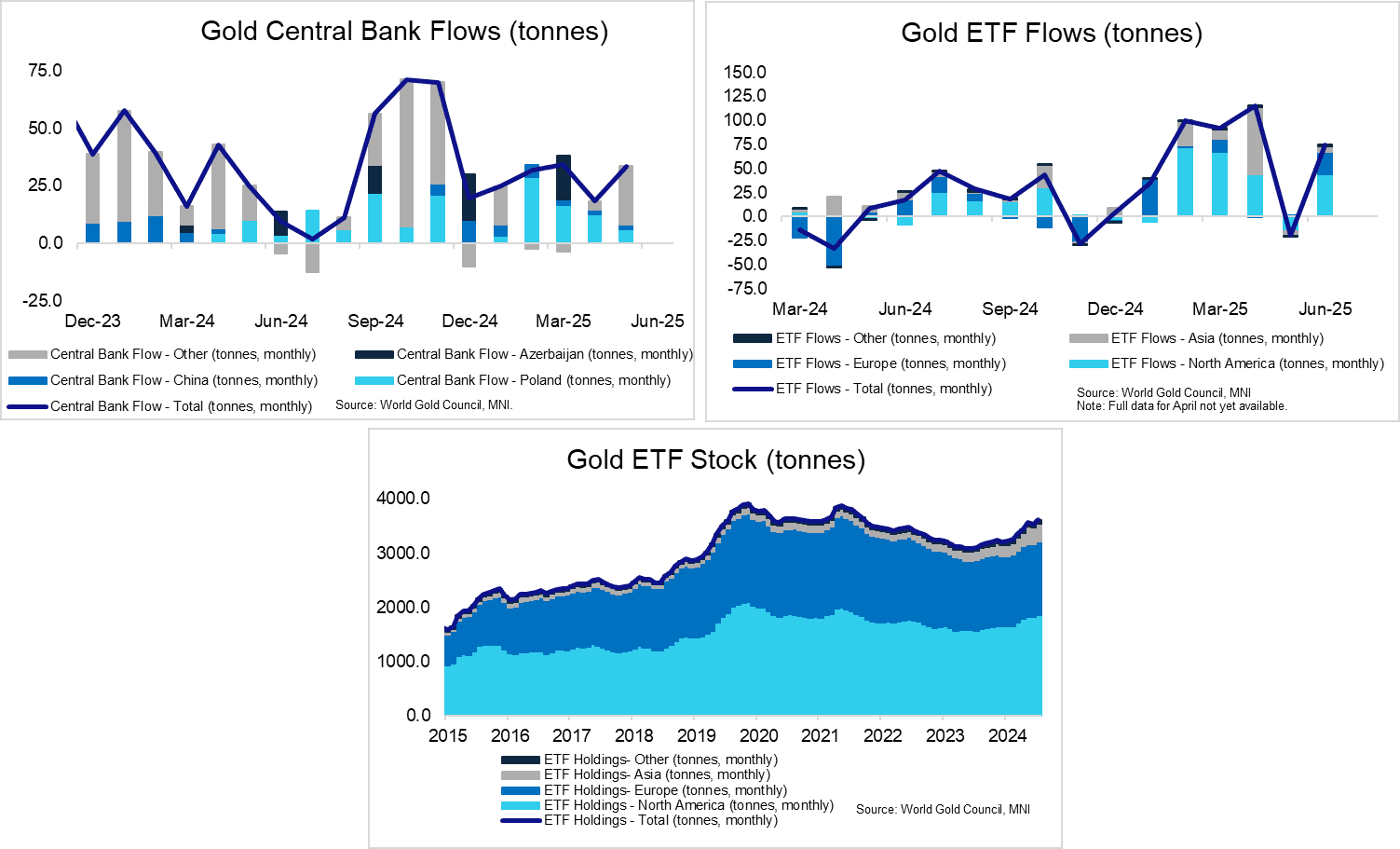

GOLD: Central Banks Still Buying; Strong ETF Inflows In June

Demand data from the World Gold Council (WGC) has been updated for June (ETFs) and May (central banks). While investor flows will be sensitive to economic/geopolitical developments and price/technicals, central banks are considered to have more inelastic demand. Latest data indicates another month of strong central bank purchases in May, a trend which should provide structural support to spot prices even if the technical picture has turned less bullish.

- There were ETF inflows equivalent to 74.6 tonnes in June, spearheaded by the US (44.3 tonnes) and Europe (23.1 tonnes). Asian ETFs, which saw huge inflows of 69.3 tonnes in April, saw a more modest 5.3 tonne inflow in June (after a 4.8 tonne outflow in May).

- The stock of gold in Asian ETFs is still substantially smaller than the US and Europe, but the 321 tonnes held in June 2025 is almost double that of a year ago (179 tonnes).

- Central Banks purchased 33.5 tonnes of gold in May, according to WGC data. There were familiar inflows from Poland (6.2 tonnes, though smaller than Feb-Apr purchases), alongside notable purchases from Kazakhstan and Turkey.

- China reported purchases of 1.9 tonnes in May, and more recent reserves data indicates another 2.2 tonnes were added in June. As always, there will be speculation that these figures could be underreporting actual PBOC purchases.