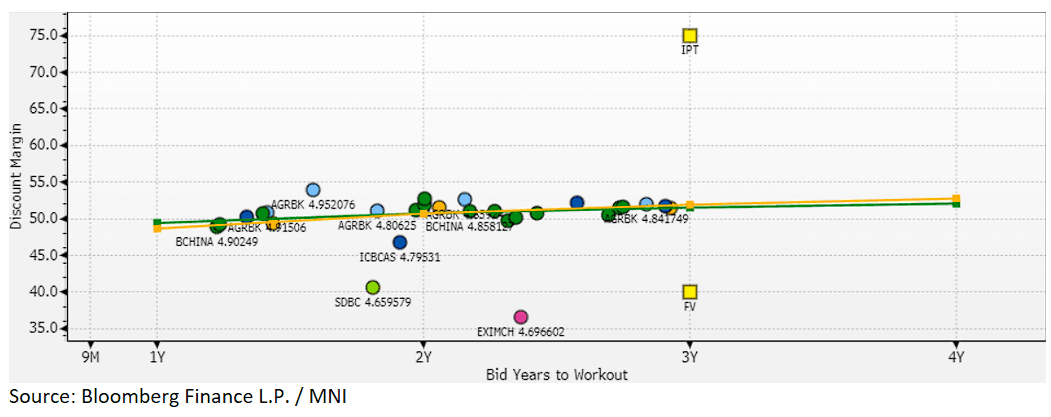

EM CREDIT SUPPLY: China Development Bank: New $ frn FV

(SDBC, A1neg/A+/-)

New Issue: $benchmark 3y FRN

IPT: SOFR +75bp area

FV: SOFR +40bp area

In terms of fair value, we focus on China Development Bank (SDBC) and Export-Import Bank China (EXIMCH) bonds. The issuers are both fully government owned and similarly rated (A1/A+).

We also introduce the Bank of China (BCHINA, A1/A), China Construction Bank (CCB, A1/-), Agricultural Bank of China (AGRBK, A1/-) and the Industrial & Commercial Bank of China (ICBCAS, A1/-) as a guide on the curve.

We see fair value close to the more recent EXIMCH $ 11/27 bond, give or take a couple of bp, as curves are relatively flat.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M5) Rallies off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.40 @ 15:42 GMT May 23

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows and for now, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.

US FISCAL: Total Tariff Income Jumping In May As New Rates Hit

Treasury reported a record $16.5B in customs/excise taxes on May 22, reflecting the large increase in tariff rates that went into effect in April.

- Today's report is important because it represents the largest tariff collections of the month which are typically on a due date around the 22nd, when most corporate importers make their payments.

- Thursday's one-day collection is a record, and the month has already set a new record. Tariff revenues have totaled $22.3B so far in May, and are came in at $17.4B in April (after averaging $8.1B/month in 2024).

- For the fiscal year as a whole so far, customs duties have totaled just under $93B, per the Treasury Daily Statement.

US FISCAL: Extraordinary Measures Continue To Dissipate Alongside Treasury Cash

Treasury's latest estimate of the size of "extraordinary measures" available to use "in order to prevent the United States from defaulting on its obligations as Congress deliberate[s] on increasing the debt limit" is down to $67B on May 21 (of an available $299B), vs $82B a week earlier.

- The amount hit the 2nd lowest level since the debt limit impasse started, at $46B, on May 20 (the low was $34B on Feb 24).

- With $476B in cash in the Treasury General Account on May 21, that left the total resources available to Treasury at $543B, the least since April 14 - the day before the annual April 15 tax deadline.

- Treasury Sec Bessent warned Congress earlier this month that "there is a reasonable probability that the federal government's cash and extraordinary measures will be exhausted in August while Congress is scheduled to be in recess. Therefore, I respectfully urge Congress to increase or suspend the debt limit by mid-July".