EM ASIA CREDIT: China (CHINA): Chip Incentives

"*CHINA PREPARES AS MUCH AS $70 BILLION IN CHIP SECTOR INCENTIVES" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY T-BILL AUCTION RESULTS: 12-month BOT Results

| Type | 12-month BOT |

| Maturity | Nov 13, 2026 |

| Amount | E8.5bln |

| Target | E8.5bln |

| Previous | E9bln |

| Avg yield | 2.06% |

| Previous | 2.05% |

| Bid-to-cover | 1.41x |

| Previous | 1.46x |

| Previous date | Oct 10, 2025 |

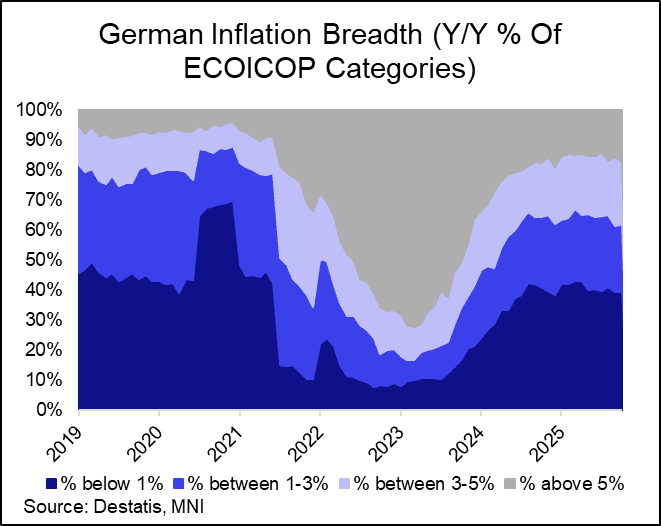

EUROPEAN INFLATION: German October Breadth Shows Move Up In Higher Cats [2/2]

MNI's inflation breadth tracker for Germany shows moderate moves to the upside in the higher-end of the spectrum, while for the low-inflation categories, developments were very limited in magnitude:

- Looking at the high-inflation categories, the percentage of ECOICOP items (a standardized category split) printing above 5% Y/Y was a little higher at 17.0% (from 15.7%), taking away from the number of categories printing in between 3% - 5%, which stood at 21.1% in October (23.1% prior).

- The low-inflation categories meanwhile remained materially unchanged last month, with 39.3% of categories printing below 1% Y/Y (39.2% prior), and 22.6% between 1% - 3% (22.0% prior).

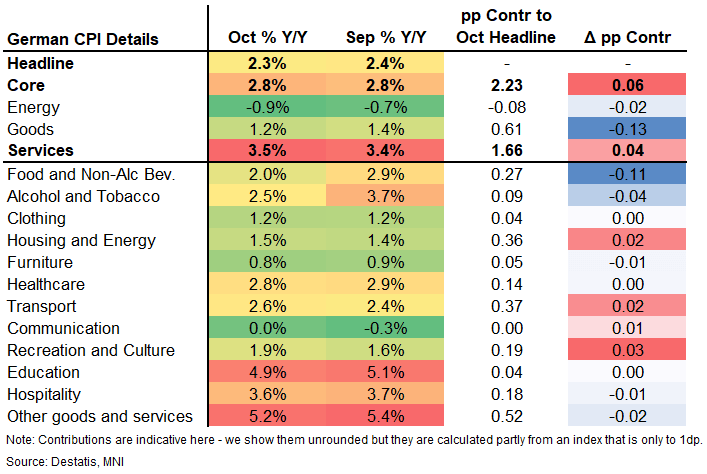

EUROPEAN INFLATION: German Services ex-Airfares CPI Contribution Shrinks [1/2]

German final October HICP was unrevised from the flash readings at 2.3 Y/Y (2.4% in Sep) and 0.3% M/M. The final reading to CPI was also unrevised at 2.3% Y/Y (2.4% in Aug) and 0.3% M/M whilst core CPI remained at 2.8% Y/Y. Details point towards the services upside surprise in the country being airfares-driven, taking away from its relevance for the ECB.

- Services accelerated to 3.5% Y/Y (confirming the flash reading) for its highest rate since April, adding 0.04pp to headline inflation in October. Goods inflation meanwhile more than negated that, with a 0.13pp lower contribution to headline, mostly on the back of both lower food and energy Y/Y.

- As we projected after the state level data ahead of the national-level flash release, airfares were a strongly positive driver, and indeed excluding their contribution the services category would have slowed vs September (airfares added 0.05pp alone, printing 3.1% Y/Y after -4.9% Sep while analysts saw a deceleration in the category).

- This is relevant because the October final inflation figures are likely the final input for the ECB's December projections and President Lagarde in her October meeting press conference again hinted that the persistence of services inflation drivers are important. Today's data confirms the ECB may likely look through the German (and as a function of that, also at least parts of the Eurozone) services upside surprise in October.

- The remainder of the services categories were mostly lower, meanwhile: Healthcare was 2.8% Y/Y vs 2.9% Sep (2.8% MNI tracking), communication 0.0% vs 0.3% Sep (0.0% MNI tracking), hospitality 3.6% vs 3.7% Sep (3.4-3.5% MNI tracking), and education was 4.9% (5.1% Sep, 4.8% MNI tracking). However, recreation and culture accelerated to 1.9% (1.6% Sep; volatile package holidays had a limited effect here; 1.9% MNI tracking).

- Non-core categories were lower across the board, meanwhile: Food (incl. non-alc beverages) was 2.0% Y/Y (2.9% Sep; 2.0-2.1% MNI tracking), while energy moved further into deflationary territory (-0.9% vs -0.7% Sep; no MNI tracking but we did project a fall in the Y/Y rate).

[See the disclaimer below the table on using the changes in contributions with caution]