EQUITIES: China & HK Equities Jump As Policy Conference Wraps Up

Hong Kong and Chinese have rallied heading into the lunch break as investors awaited the conclusion of China’s economic work conference for insights on 2025 fiscal and monetary strategies. Retail stocks in China surged on news of voucher programs to boost consumption.

- Tech stocks are benefitting from a rally overnight in the US, with the NASDAQ closing 1.90% higher. The HSTech Index is currently 2.00% higher, with Tongcheng Travel up 8.50%, Trip.com up 4.35% and Bilibili is 5.20% higher. Elsewhere property stocks are trading higher, with the Mainland Property Index up 1.20%, while the HSI is up 1.45%

- China mainland equities are also trading well with all sectors in the green. The CSI 300 is up 0.85%, outperforming smaller-cap indices.

- The Chinese economic policy meeting is expected to wrap up shortly with investors hopeful for supportive measures that could reveal what measures Beijing might use next year to combat deflation and the impact of potentially higher US tariffs.

- The data calendar is light on for the rest of the week, with focus turning to Industrial Production, Retail Sales on Monday,

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

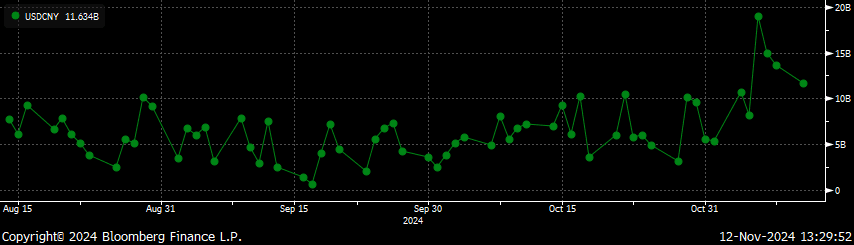

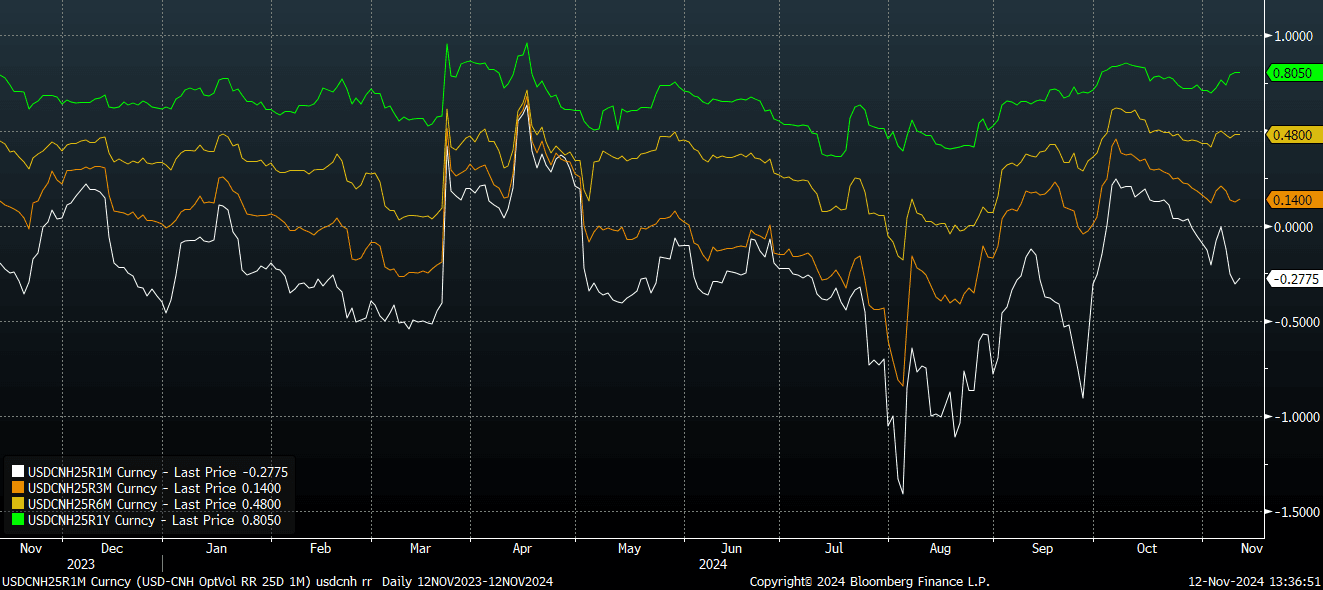

CNH: CNY FX Option Volumes Elevated, USD/CNH 12mth RR Close To Cycle Highs

USD/CNH is steady around the 7.2400 level in latest dealings. Earlier highs were at 7.2454, levels last seen in early August. Spot USD/CNY has gravitated higher as well, but found some selling resistance above 7.2300. The earlier BBG report on potential lower taxes to aid property sentiment hasn't had a lasting positive impact on equity sentiment, with headline indices back to around flat or slightly weaker. Hong Kong's HSI is down over 1%.

- In the FX option space, CNY volumes are dominating Tuesday trade so far. The chart below shows the trend shift higher in USD/CNY volumes since the US election, per DTCC (BBG). Today CNY has accounted for around 31% of total volumes, followed by JPY with 17%.

- For USD/CNH risk reversals, we have a positive skew the longer the tenor. The second chart shows USD/CNH risks reversals for the 1 month, 3 month, 6 month and 12 month tenors. This is typically always the case, although trends have diverged somewhat in the past week, with the 1 month RR tracking lower, while the 12 month is close to cycle highs.

Fig 1: USDCNY Options Volumes, Firmer Since Early Nov

Source: MNI - Market News/Bloomberg

Fig 2: USD/CNH Risk Reversals

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Closed Cheaper, H/H Spending Up Again

NZGBs closed 1-3bps cheaper across benchmarks, aligning with cash US tsys, which are also flat to 3bps cheaper in the Asia-Pac session today with a flattening bias. US tsys reopened today after being closed for the Veterans Day holiday yesterday.

- NZ retail card spending posted a third consecutive monthly rise in October up 0.6% m/m after 0.1%. Total spending rose 0.4% m/m after 0.3% and is now slightly positive on a year ago. The start of easing in August appears to have allowed households to begin to spend again.

- Westpac sees the October data as “encouraging” and that there should be further rises once past and future rate cuts are fully felt. Westpac observes that “most mortgages have not come up for refixing yet. In addition, further cuts from the RBNZ are expected over the coming months (we’re forecasting another 50bp cut at the upcoming November meeting).”

- Swap rates closed 1-3bps higher, with a flattening bias.

- RBNZ dated OIS pricing closed 3-8bps firmer across 2025 meetings. A cumulative 89bps of easing is priced by February, with 52bps by year-end.

- Tomorrow, the local calendar will see Net Migration data, ahead of REINZ House Sales and Food Prices on Thursday.

OIL: Crude Holds Onto Losses As Supply/Demand In Focus

After falling over 2.5% on Monday, oil prices are down a bit further during APAC trading today as demand concerns, especially from China, persist. There is also the risk of additional US supply under the Trump administration. Brent is down 0.15% to $71.72/bbl, off the $71.62 low. WTI is 0.1% lower at $67.96/bbl having broken below $68 to make a trough of $67.84. Continued greenback strength continues to weigh on dollar-denominated crude with the USD BBDXY index up another 0.1%.

- There will be further information on the current demand/supply position and the outlook later today with US industry-produced inventory data for last week and OPEC’s monthly report. The EIA’s short-term energy outlook is out tomorrow and the IEA’s report on Thursday.

- Prompt spreads continue to point to a tight oil market but it is easing with the gap between the two nearest contracts narrowing, according to Bloomberg.

- Later the Fed’s Waller, Barkin, Kashkari and Harker speak and the Senior Loan Officer Survey is published. US October small business optimism and NY Fed 1-yr inflation expectations plus UK labour market data and euro area November ZEW print. ECB’s Cipollone and BoE’s Pill appear.