FED: Chicago's Goolsbee Sounds Increasingly Cautious, Auguring Later Cuts (1/2)

Chicago Fed Pres Goolsbee (2025 FOMC voter, most dovish Committee member per MNI's Hawk-Dove Spectrum) on CNBC makes the first Fed commentary after the March meeting, and he doesn't sound at all like he's pushing hard for rate cuts anytime soon: "At the end of the day, I still think that the Fed needs to be the steady hand and take the long view. I understand why the market wants to get the information as rapidly as possible and wants to know by Monday morning or by the end of today, what's going to be the path for rates, for tariffs, for fiscal policy for the entire rest of the year, but it's not realistic at this moment. The markets go up, the markets go down, they got a lot of short run, volatility, if you take the longer view I still think that there's a lot of strength in the hard numbers on the economy."

- His growth/rate outlook again seems to temper his previous expectations that rates would be "a fair bit" lower in 12-18 months: "I still think the economy is resilient, and if we get past this bumpy period of some uncertainty, I still think that there is - when the unemployment rate and the job market are settled in at what looks like full employment - if we can continue to make progress on inflation over the long run, I believe that rates 12 to 18 months from now, will be lower than where they are today."

- But he adds that he expects those cuts to be back-loaded: "waiting isn't free in that you gain information, but you lose the ability to move gradually. So I think the longer you wait, the cuts when they come are going to be back loaded, and so that's why I say 12 to 18 months from now I think rates are lower, but in this period right now, we just have to wait."

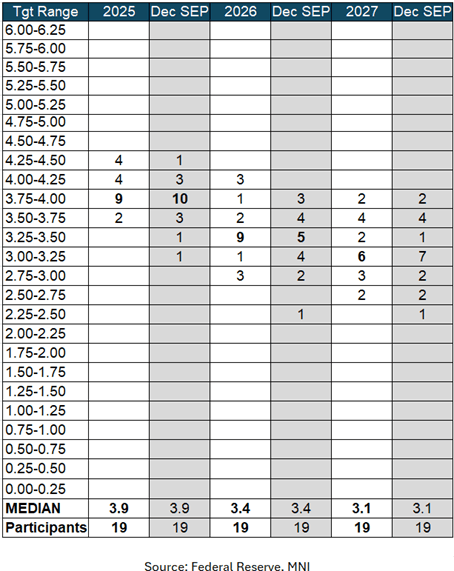

- To contextualize Goolsbee's comments: we know from the Dot Plot that he saw at most 3 cuts this year (the lowest 2 Dots of 19 had 3.6% at end-2025, vs a committee median of 3.9%), and it's a decent bet he also sees another 3x cuts in 2026 (the lowest 3 of 19 were at 2.9%, vs a Committee median of 3.4%). But judging from his comments this morning, those 2025 cuts will be "back loaded". Now, he may no longer be the Committee's biggest dove - he's been changing his tone since tariff etc policy shifts started coming into view - but we take this as a sign that FOMC participants aren't close to cutting rates.

- Goolsbee wasn't explicit about his exact rate path but if it's truly back-loaded, with 3 cuts in the last 3 meetings of the year, that would suggest the earliest meeting that is seriously being eyed by the Committee for a cut is September (compared to market expectations of 2x cuts through September), unless there are clear signs of recession in the "hard data".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: ERU5 97.875/97.750/97.625 Put Ladder Sold

ERU5 97.875/97.750/97.625 put ladder 10K given at -0.25.

EGBS: 10-year BTP/Bund Spread Off Highs As Equities Find A Base

The 10-year BTP/Bund spread has moved away from intraday highs as European equities find a short-term base, but remains 2.5bps wider at 108bps.

- This morning’s equity-led spread widening was exacerbated by ECB Executive Board member Schnabel’s hawkish interview with the FT (even as Schnabel’s comments were in line with her usual stance).

- The spread briefly marked below 104bps yesterday. The prospect of increased joint EU issuance to fund defence spending may have contributed to Monday/Tuesday’s tightening, alongside broader German fiscal risks ahead of Sunday’s election.

- MNI’s German election preview is here.

EUROZONE DATA: Flash Vacancy Rate Steady At 2.5% In Q4

The Eurozone seasonally adjusted flash Q4 vacancy rate was 2.5%, unchanged across the last six quarters and down from a peak of 3.3% in Q2 2022. This suggests little scope for further easing of labour market conditions on the demand side, with further loosening (if any) likely to come via the unemployment rate. Unemployment remains close to historical lows at 6.3% as of December.

- The EC’s expected employment index ticked up to 98.8 in January (vs 97.2 prior), but remains below the 2000-2019 average of 99.5.

- Meanwhile, Eurozone business economy flash Q4 labour costs - also released today - eased to 4.1% Y/Y (vs 4.6% prior) for the lowest since Q3 2022. This is consistent with the ECB’s expectations for decelerating compensation growth, which should eventually feed through into services inflation.

- However, we caveat that Eurostat has to estimate multiple components (e.g. compensation, hours worked) using partial/preliminary data from member states to calculate the flash labour cost data, which makes it prone to revisions in the final release.