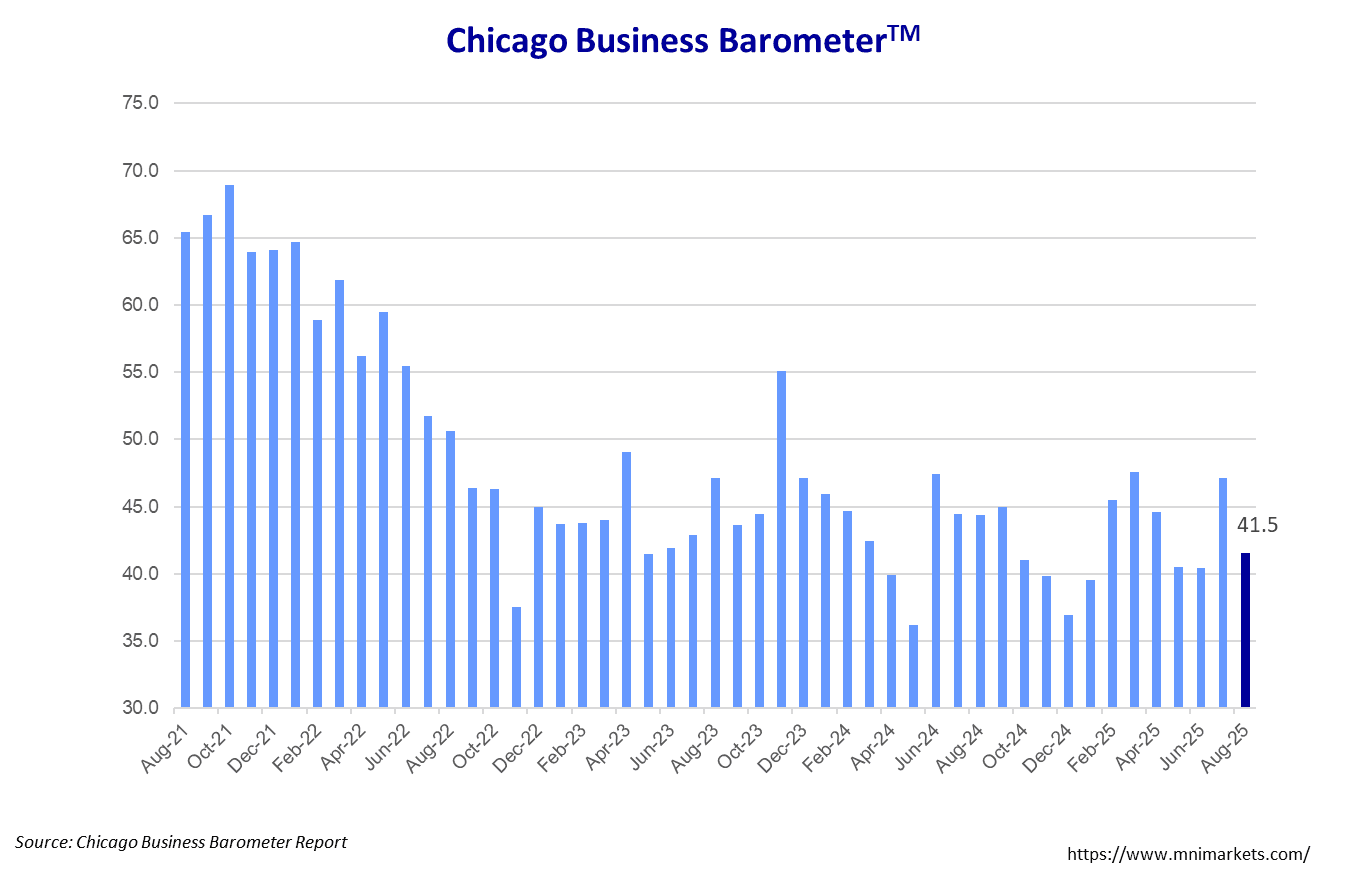

US DATA: Chicago Business Barometer™ - Slows To 41.5 In August

The Chicago Business Barometer™, produced with MNI slowed 5.6 points to 41.5 in August. This almost fully unwinds the rise seen in July. The index has now been below 50 for twenty-one consecutive months.

- The decline was driven by a sharp pullback in New Orders, alongside falls in Employment, Production and Order Backlogs. This was partly offset by a rise in Supplier Deliveries.

- New Orders dropped 10.8 points. This was the largest fall since September 2023, and was driven by a decrease in the proportion of respondents reporting more new orders and an increase in the proportion reporting fewer new orders.

- Employment compressed 5.9 points to the lowest since June 2020. The index has now more than unwound the 8.3-point increase seen in May.

- Production softened 3.6 points to the weakest level since December 2024. This marks the fifth consecutive decline in Production.

- Order Backlogs eased 1.4 points.

- Supplier Deliveries increased 5.8 points. For the second month this year, no respondents reported faster supplier deliveries.

- Prices Paid contracted 8.3 points for the second consecutive month. However, the index remains above the 2024 average.

- Inventories weakened 2.3 points.

- The survey ran from August 1 to August 11.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Links To Rate Decision, With Hold Clearly Expected

Markets are pricing in under 10% probability of a rate cut at the upcoming 9:45ET BOC decision (hold at 2.75% is unanimous analyst expectation) - 16bp of cuts are currently priced through year-end.

- BOC Links to go live at that time:

- Rate announcement

- Press conference opening statement

- Monetary Policy Report

| Meeting | Current | Post-June Meeting (Jun 05) | Change since then | Cumulative Change From Current Rate (bp) | Incremental Chg (bp) |

| Jul 30 2025 | 2.73 | 2.65 | 8.1 | -2.0 | -2.0 |

| Sep 17 2025 | 2.69 | 2.54 | 15.0 | -6.3 | -4.3 |

| Oct 29 2025 | 2.64 | 2.46 | 18.0 | -11.6 | -5.3 |

| Dec 10 2025 | 2.60 | 2.41 | 18.9 | -15.8 | -4.2 |

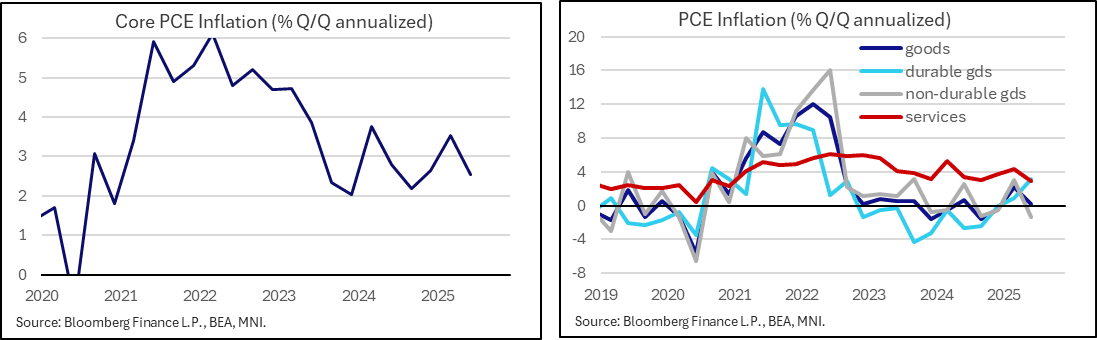

US DATA: Mixed Inflation Figures In Q2 Flash

The price side of the advance Q2 national accounts release was mixed, with the GDP deflator on the soft side whilst, more notably, core PCE inflation moderated by less than expected. The upside surprise suggests some scope for a surprise in June’s core PCE print tomorrow (previous unrounded estimates were averaging around 0.28% M/M) although our bias is that most of this Q2 surprise will be seen earlier in the quarter after revisions.

- The GDP deflator surprised softer with a 2.0% annualized increase (cons 2.2) in Q2 after 3.8% in Q1.

- There was widespread moderation here, with personal consumption easing from 3.7% to 2.1%, private domestic investment from 1.2% to 0.6%, government consumption & investment from a strong 4.6% to 2.7% and a moderation in exports (from 5.3% to -1.2%) outpacing imports (from2.1% to -0.8%).

- Core PCE inflation meanwhile was surprisingly strong as it moderated by less than expected to 2.54% (cons 2.3) after 3.53% in Q1.

- We had seen unrounded analyst core PCE estimates average 0.28% M/M after the June round for CPI/PPI/import prices with a chance of a small upward revision for May judging by PPI. That estimate, assuming no revision, would have seen a 2.30% increase – we imagine the upward surprise was more likely concentrated earlier in the quarter.

- Looking within overall PCE inflation, an acceleration in durable goods inflation bucked the quarterly trend, accelerating from 2.9% o 3.1% annualized for its strongest since 1Q25, whilst nondurable goods inflation slowed to -1.3% after jumping 3.0% in Q1.

- PCE services inflation meanwhile eased from 4.3% to 2.9% for its softest since 4Q20.

US TSY FUTURES: BLOCK: Sep'25 30Y Ultra-Bond Buy

- +2,000 WNU5 117-02, post time offer at 0918:59ET, DV01 $380,000.

- The 30Y ultra contract trades 117-02last (-16)