OIL: Chevron Accelerates Tanker Loadings

Jan-08 20:42

Chevron is loading crude cargoes bound at the fastest pace in seven months, mostly bound for P66 and...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Macro Since Last FOMC - Growth: Solid ISM, Tepid Beige Book

Dec-09 20:41

- Various major business surveys, an important data source having not been disrupted by the government shutdown, also continue to point to generally robust activity.

- The November ISM services was stronger than expected in November as it surprisingly inched higher to 52.6 (+0.2pts) for its highest since February. The S&P Global US services PMI at 54.1 again offers a more optimistic assessment of current activity despite being revised down in its final November release, albeit with its smallest overshoot since April. More forward-looking implications are mixed though, with ISM services new orders slipping in November (but within a particularly volatile period that makes it hard to get a sense of trend) in contrast to the services PMI noting that activity was “supported by the firmest rise in new work of 2025 so far”.

- Somewhat countering this services resilience, the ISM manufacturing index was lower than expected in November as it fell to 48.2 (-0.5pts) vs expectations of some stabilization. It’s back at the low end a narrow range of 48.0-49.1 since March, having eased since Jan and Feb saw the first expansionary months above 50 since late 2022.

- Alternate anecdotal evidence points to more tepid activity, however. The Beige Book reported economic activity “was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth." The breadth of district responses did at least see a small improvement compared to the mid-October report.

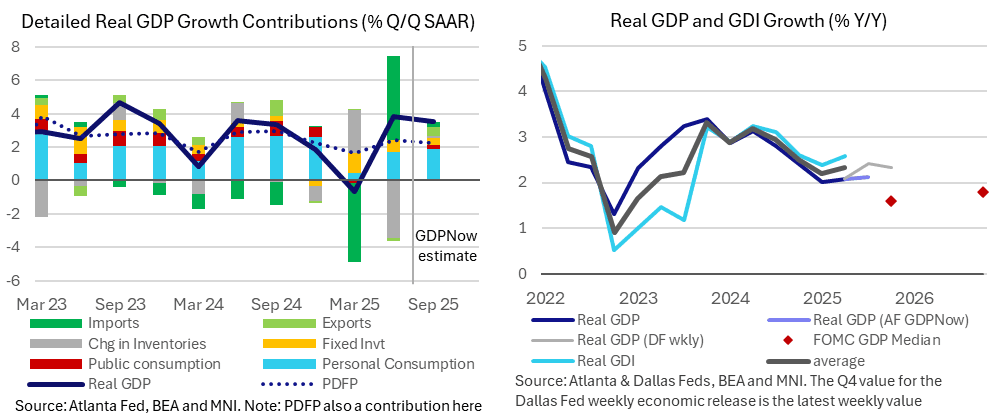

US OUTLOOK/OPINION: Macro Since Last FOMC - Growth: Robust Tracking

Dec-09 20:39

- Real GDP growth has likely been the main area where the FOMC has been surprised to the upside, especially since the last economic forecasts with the September SEP but also since the late October decision.

- The Atlanta Fed’s GDPNow extended estimate eyes real GDP growth of 3.5% annualized in Q3, a useful tracker having now missed two official releases for Q3 originally scheduled for Oct 30 and Nov 26. Instead, the BEA is going to combine these two reports with an “initial” release that will include the alternate Gross Domestic Income series on Dec 23.

- Assuming the Atlanta Fed estimate is accurate – and it has tended to outperform analysts in recent quarters – it paints a only a slightly softer picture than the 3.84% in Q2, with a similar story for private domestic final purchases estimated at ~2.6% annualized after 2.86% in Q2.

- As for a more timely update, the Dallas Fed weekly economic index currently points to further robust GDP growth into Q4, tracking a little above 2% Y/Y in late November estimates. Whilst that implies more of the same since the 2.1% Y/Y back in Q2, the median FOMC forecast from September had this cooling to 1.6% Y/Y in Q4.

AUDUSD TECHS: Northbound

Dec-09 20:30

- RES 4: 0.6723 High Oct 21 ‘24

- RES 3: 0.6707 High Sep 17 and a key resistance

- RES 2: 0.6660 High Sep 18

- RES 1: 0.6654 High Dec 12

- PRICE: 0.6652 @ 16:49 GMT Dec 9

- SUP 1: 0.6580/6551 High Nov 13 / 20-day EMA

- SUP 2: 0.6517 Low Nov 27

- SUP 3: 0.6466/21 Low Nov 26 / 21

- SUP 4: 0.6415 Low Aug 21 / 22 and a bear trigger

A strong impulsive bull wave in AUDUSD remains intact. Note that moving average studies have recently crossed and are in a bull-mode position, reinforcing current conditions. The pair has also printed 10 consecutive sessions of higher highs. 0.6640, 76.4% of the Sep 17 - Nov 21 bear leg, has been pierced This opens 0.6707, the Sep 17 high and key resistance. Key support to watch is at 0.6551, 20-day EMA.