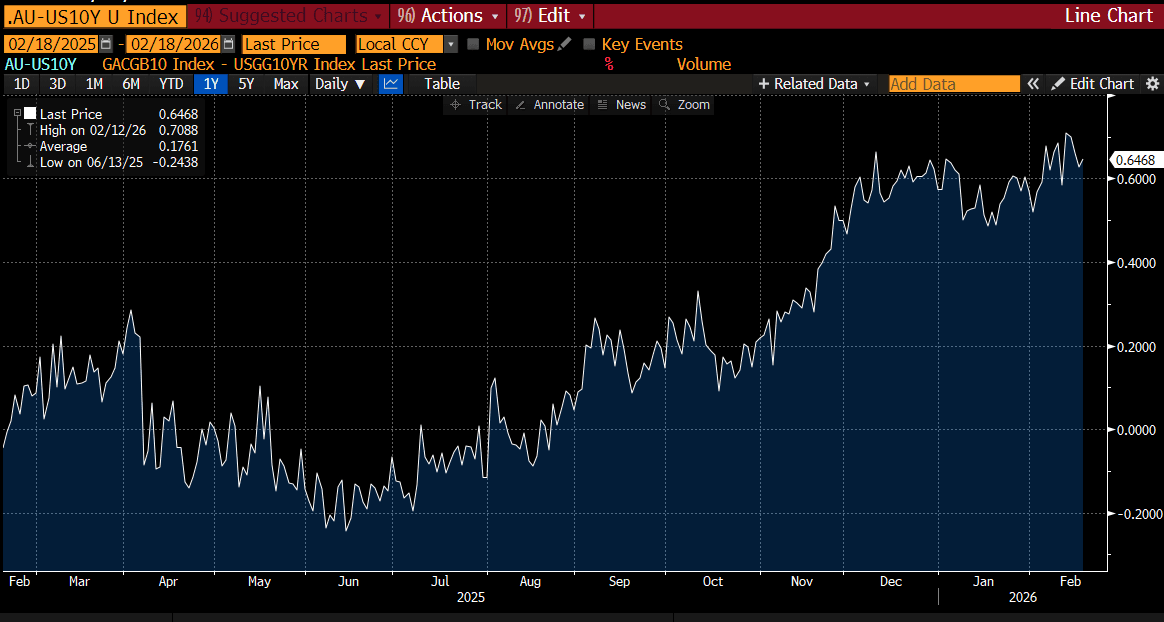

AUSSIE BONDS: Cheaper, US Tsys Mixed Close, WCI & Oct-36 Supply Due

ACGBs (YM -2.5 & XM -2.0) are weaker after US tsys finished slightly mixed, with a mild flattening.

- The Federal Reserve should keep interest rates on hold "for some time" until data show goods inflation receding and the job market staying stable, Fed Governor Michael Barr said Tuesday, adding the AI boom is unlikely to be a reason for lowering rates.

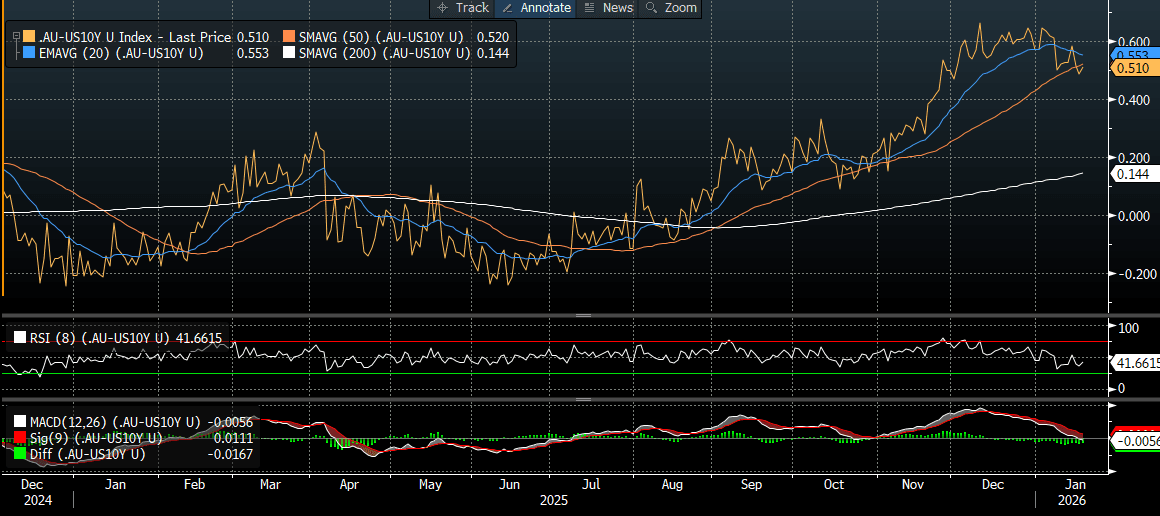

- Cash ACGBs are 2bps cheaper with the AU-US 10-year yield differential at +65bps.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 13% for March to 84% by June and 133% by December 2026.

- Today, the local calendar will see the Q4 Wage Cost Index, with the market expecting 0.8%q/q (3.4%y/y) wage outcome.

- Note the RBA forecast for Q4 was 3.4%y/y in its Statement On Monetary Policy. The central bank sees y/y wage momentum slowing over the forecast horizon to 3.1%y/y mid this year and then 3.0% by mid-2028. This is consistent with the RBA's unemployment rate outlook (steadily rising to 4.6% by mid-2028).

- The AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond today and A$800mn of the 3.25% 21 April 2029 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper In Early Trade, Cash US Tsys Out For MLK Holiday

ACGBs (YM -2.5 & XM -3.0) are weaker after cash US tsys finished 2-5bps cheaper on Friday.

- The coming holiday-shortened week (Monday is MLK Day) will be highlighted by legal intrigue on Tuesday and Thursday, with the US Supreme Court potentially releasing its ruling on the legality of the White House's IEEPA tariffs on its next scheduled opinion day on Tuesday, and oral arguments on Wednesday over whether President Trump is allowed to fire Fed Governor Lisa Cook.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at +51bps, near its lowest level since early December. Over the past month and a half, price action had effectively consolidated the differential’s breakout above the ±30bps range that had prevailed since November 2022. This widening has coincided with a steady lift in market-implied expectations for the RBA cash rate.

- The bills strip is -2 to -3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 28% for February to 91% by June and 147% by December 2026.

- Today, the local calendar will see Melbourne Institute Inflation Gauge.

- A new 21 October 2037 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).

Bloomberg Finance LP

TARIFFS: EU Leaders Seek To Negotiate On Tariff Threat, But Ready Measures

Earlier headlines crossed that the EU has no plans to deploy counter measures against the US, at this stage, following Trump's tariff plan. To recap, Trump announced on Saturday a 10% tariff on EU countries from Feb 1, which will then rise to 25% in June of this year, for those countries opposing US efforts to acquire/control Greenland. The countries impacted are Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands and Finland after they not only voiced their opposition but either sent troops or representatives to the island.

- EU leaders/ambassadors agreed to continue/intensify diplomat efforts to avoid US tariffs being implemented on February 1. Note that US President Trump is in Davos this Wednesday.

- News Wires are reporting that EU counter measures are being considered though: via RTRS: "The EU's options include a package of its own tariff on 93 billion euros of U.S. imports that was suspended for six months in early August and the range of measures under the Anti-Coercion Instrument that could hit U.S services trade or investments." This proposal was considered ahead of the US-EU reaching a trade agreement last year.

- US Tsy Secretary Bessent noted over the weekend: "Treasury Secretary Scott Bessent amplified President Donald Trump’s message to European allies that the US won’t back down on taking over Greenland, saying the continent is too weak to ensure its security." via BBG.

Economic Advisor Hassett stated: "“Right now it’s really a good time for cooler heads to prevail and for us to disregard the rhetoric and get to the table and see if there can’t be deal worked out that’s best for everybody,” Hassett said on Fox News’ The Sunday Briefing." via BBG as well.

BONDS: NZGBS: Heavy Open After Heavy Close By US Tsys On Friday

NZGBs are 2-3bps cheaper after US tsys finished last week on a heavy note, 2-5bps cheaper.

- After some massive US Block/buying in 5s (20k at 108-25.75) and 10s (+50k 111-28) buoyed rates in late morning trade – US futures extended lows in late in the session, more flow driven amid a lack of obvious headline triggers.

- Cash US tsys are closed on Monday for holiday. ADP Weekly NER Pulse and Philadelphia Fed Non-Manufacturing Activity is expected on Tuesday.

- The local data calendar is empty today. PM Luxon makes his State of the Nation speech on Monday at 1255 NZDT/1055 AEDT.

- Q4 CPI data print on Friday and are expected to show inflation returning to the 1-3% band. The RBNZ left the door open for another rate cut at its 18 February meeting but a higher-than-expected inflation print towards to the top of target and activity continuing to recover are likely to mean that it is on hold.

- Bloomberg consensus expects Q4 CPI to rise 0.4% q/q bringing the annual rate down to 2.9% from 3.0% above the RBNZ’s November forecast of 0.2% and 2.7%. Swap rates are

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while December 2026 assigns 37bps.