US DATA: Challenger Job Trends This Year Are Higher-Firing, Lower-Hiring

Oct-02 12:59

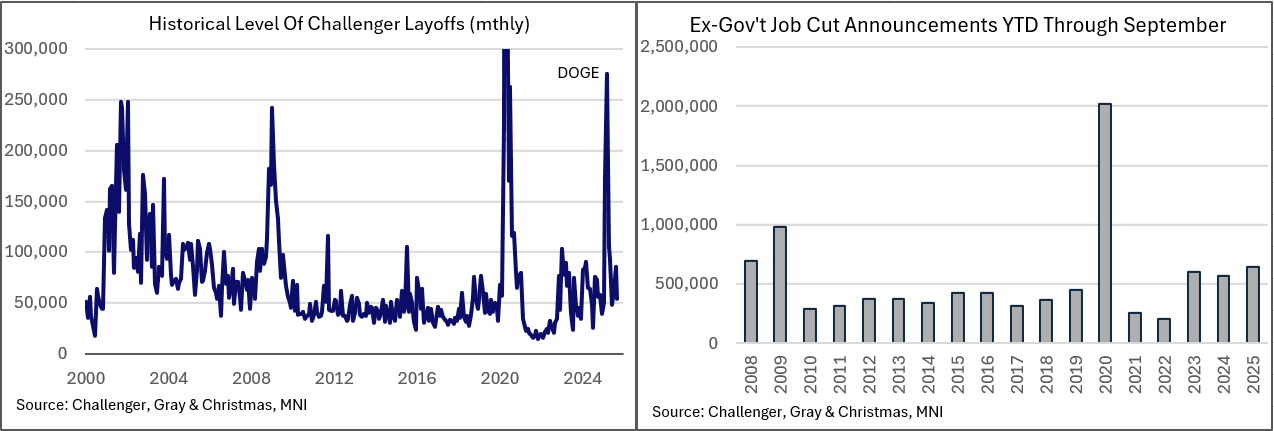

Challenger, Gray & Christmas reports job cut announcements fell 25.8% Y/Y in September, less severe than consensus which had expected a 13.3% rise. But the broader report was suggestive of a labor market at its most low-hiring and high-firing for a first 9 months of the year since the pandemic and before that, the Global Financial Crisis, with hiring in September itself looking unusually weak ahead of the key holiday season for retailers.

- It should first be acknowledged that public sector-related employment is the main driver of overall weakness: the government sector has announced 299,755 job cuts this year, all but about 10k of which were DOGE-impacted. (Similarly, the regional job cuts breakdown was heavily weighted to the East, the lion's share being reductions at federal agencies in Washington DC with cuts rising 759% to 298,901 from 34,788). A distant second sector-wise is Tech which has shed 107,878 jobs so far this year.

- Likewise, employers' reasoning for layoffs is DOGE-related: that is cited in 293,753 planned layoffs YTD. That's also seen an additional 20,976 cuts "attributed to DOGE Downstream Impact, such as the loss of funding to private non-profits and affiliated organizations."

- However, market/economic conditions were also cited for 208,227 cuts YTD, which "reflects employers’ continued response to economic uncertainty, inflation, tariffs, and shifting demand across sectors."

- And while the headline figures are exaggerated by DOGE effects, the non-government job market as reported by Challenger appears as weak as it has in the last 15 years (ex-pandemic).

- Ex-government job cuts were down 32% Y/Y on the month, but looking at the year-to-date, they totaled 646,671: this is up from 571,503 in 2024 and the most since 2020; before that the biggest 9-month cumulative ex-gov't job cut total was 2009 (981,306).

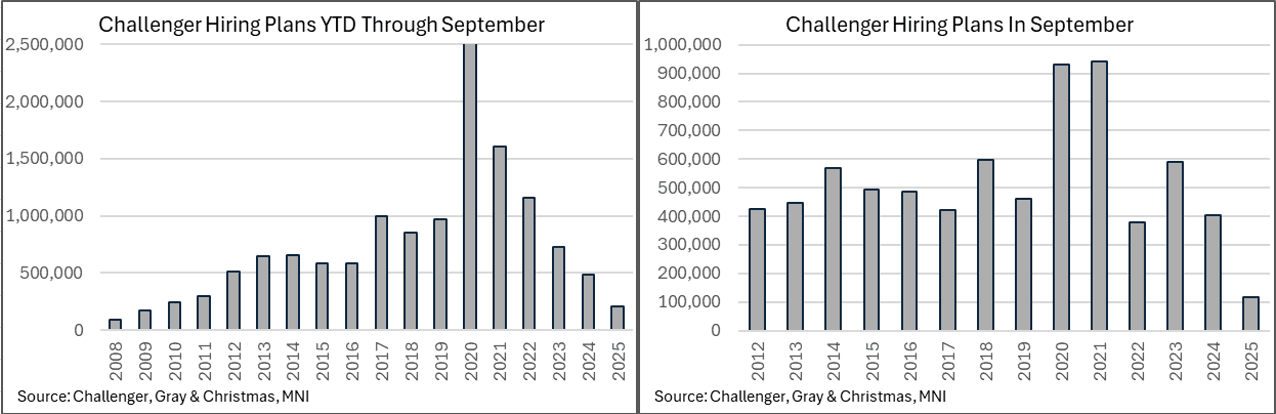

- And against this backdrop, hiring plans remain very soft: through September YTD the 204,939 hiring intentions are down 58% Y/Y for the lowest since 2009 at the depths of the Global Financial Crisis. For September itself, hiring plans were a post-2011 low 117,313 (as usual this was made up largely of retailers ahead of the holiday season, which totaled 96,450 - but this was well below the 403,893k prior).

- It's possible that a strong final quarter of the year, starting with seasonal hiring in October, boosts the underlying data enough to make it not as comparable to historical recession years, but so far it doesn't appear that way.

- “It’s very likely job cut plans are going to surpass a million for the first time since 2020 and for the ninth time in our series. Previous periods with this many job cuts occurred either during recessions or, as was the case in 2005 and 2006, during the first wave of automations that cost jobs in manufacturing and technology,” as the report quoted Andy Challenger, "Senior Vice President and labor expert for Challenger, Gray & Christmas." That refers to the 946,426 layoff intentions YTD vs 609,242 in 2024, which while exaggerated by government effects, also shows a weaker underlying private sector labor market.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USDJPY Extends Intra-Day Rally to 1.15%

Sep-02 12:55

- A combination of drivers have propelled USDJPY to a fresh one month high of 148.93 on Tuesday. On the topside, 149.12 is the next resistance (61.8% of the Aug 1 - 14 bear leg). However, should momentum continue to gather speed, investors will look to another retracement level at 149.81, followed by 150.92, the August 01 high and a key resistance.

- The initial impetus for the squeeze higher came from BOJ Deputy Governor Himino, who gave no guidance on the timing or pace of potential rate hikes, providing little confidence to yen longs.

- The dynamic of widening yield differentials underpinning the USDJPY rally was then exacerbated by a relief rally for JGB futures following a very solid 10-year auction (highest bid-to-cover since 2023) and the subsequent contrasting pressure on core fixed income that has seen US 10-year yields extend their rise to 7bp on the day.

- Political uncertainty also played its part in the yen sell-off, as a flurry of resignations from senior leadership positions within the governing LDP have followed an internal party meeting. It remains to be seen whether this proves a sufficient sacrifice to keep Japanese PM Ishiba in office.

MNI EXCLUSIVE: EU trade sources comment on Mercosur deal

Sep-02 12:52

EU trade sources comment on the probability of approval for a trade deal with Mercosur. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US TSY FUTURES: BLOCK: Dec'25 10Y Ultra Buy

Sep-02 12:52

- +6,800 UXYZ5 113-23, buy through 113-22.5 post time offer at 0836:13ET, DV01 $590,000.

- The 10Y Ultra contract trades 113-23.5 last (-21.5)