US DATA: Challenger Job Cut Announcements Ease Back To More Typical Levels

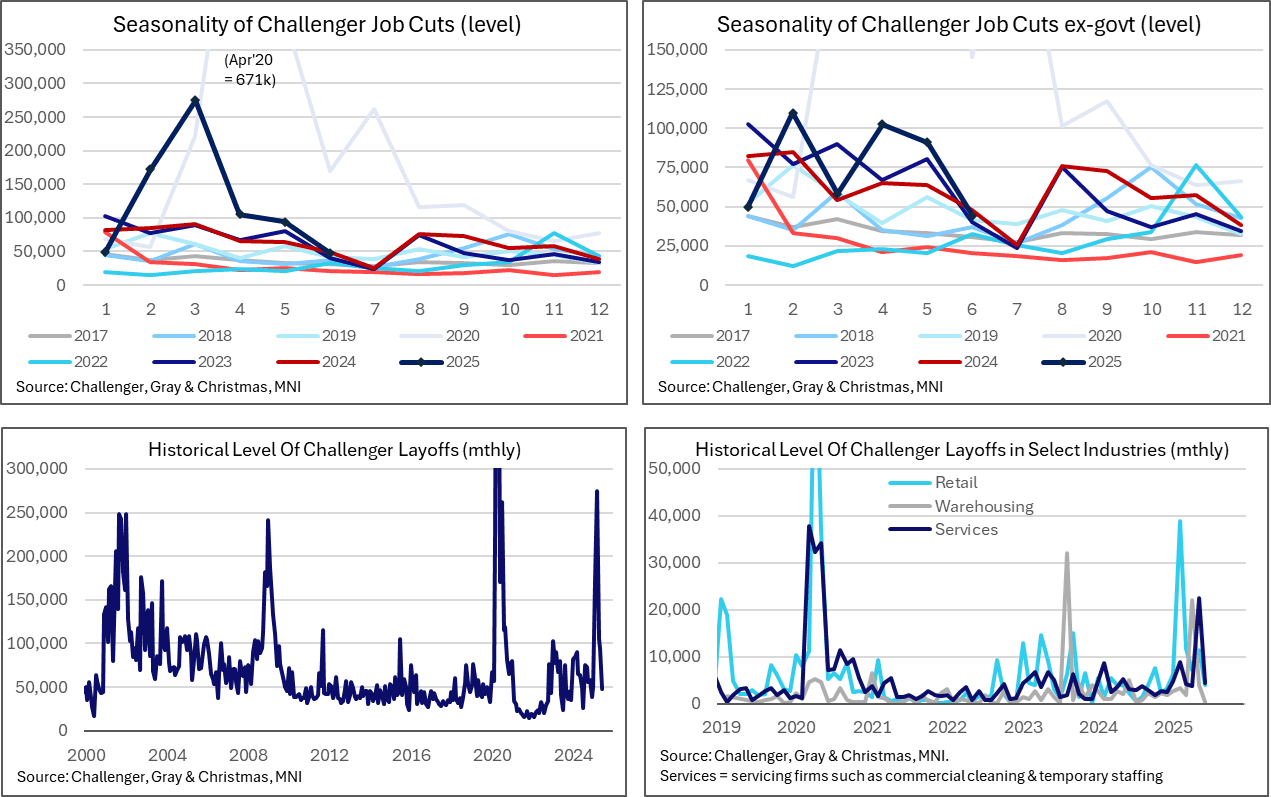

The Challenger, Gray & Christmas job cuts report showed a relatively benign June after some strong increases earlier in the year.

- Challenger job cut announcements amounted to 48k in June after 93.8k in May, for a -2% Y/Y decline after some elevated readings earlier this year that were driven by more than just direct DOGE effects.

- It follows a 47% Y/Y increase in May, 63% Y/Y in April and an average 90% Y/Y through Q1.

- Ex-government layoffs meanwhile were -8% Y/Y in June after 43% Y/Y in May, 58% in April and an average -1% Y/Y in Q1.

- From the press release: ““The bulk of companies cited economic conditions last month. We saw some DOGE activity and have tracked over 2,000 jobs directly attributed to tariffs this year, but for the most part it was a quiet June.”

- Consumer products saw the highest layoffs (9.5k) followed by services (4.5k). The latter is pulled back to somewhat more typical levels after an unusually high 22.5k in May (services includes “companies that service other companies such as commercial cleaning services and temporary staffing firms”).

- Retail, one of the areas most directly impacted by tariffs, still sees some large Y/Y increases even if the actual layoffs numbers are small: the 4.1k in June was a 85% Y/Y increase after 11.5k in May (184% Y/Y) and 7.2k in Apr (77% Y/Y).

- As for warehousing, one specific area watched for implications from inventory builds earlier in the year on tariff front-running, layoff announcements were tiny at 0.3k after 3.9k in May and a large 22k in April.

- By specific reason for the 744k of layoffs in the ytd, DOGE actions still top the list with 287k (plus 12k from downstream impact) followed by market & economic conditions at 154k (vs 131k in last month’s report) and closures at 107k (vs 94k last month).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUDUSD Rallies Back Towards 0.6500, Busy Calendar This Week

- Despite dented risk sentiment to start the week, the prevailing theme of USD weakness has provided AUDUSD with a 0.85% boost to start the week. Spot received support in the low 0.6400s last week keeping bullish trend signals intact.

- A continuation higher would open 0.6550, a Fibonacci retracement, and the November 25 high. Above here, the key medium-term focus is on the US election related highs at 0.6688.

- Westpac recently wrote they still see merit in sticking patiently with a core AUDUSD long, looking for an eventual break beyond the 0.6500/15 area on a 1-3mth horizon. Westpac believe the outlook still favours an appreciation profile for the pair, albeit one that is a choppy, low- intensity grind, with the USD doing most of the leg work driving periodic discrete bullish resetting of ranges.

- Notably, CFTC Data shows asset managers pared back their shorts ever so slightly, however, the leveraged community added to their shorts quite aggressively over the week.

- We have a busy calendar this week in Australia, with the RBA minutes, first quarter GDP and April trade balance data the highlights. The RBA is likely to deliver two more 25bp cuts this year coinciding with updated forecast publications, former staffers recently told MNI, arguing that the RBA’s concerns over labour market tightness means that the market’s expectation for the cash rate to reach 3.1% by Dec was likely overblown.

BUNDS: Futures Retrace Half Of Early Selloff As NY Desks Filter In

Bund futures have retraced around 50% of the selloff since the EGB cash open, now -21 ticks at 131.00 after reaching a session low of 130.72 earlier. No obvious trigger for the broader reversal in core FI over the past few hours, with NY desks seemingly opting to fade this morning’s weakness as the US session gets underway.

- The passing of this morning’s triple-line EU-bond auction at 1030BST will have removed an additional intraday headwind to Bunds, but the recovery is still notable given Brent Crude futures have continued to extend session highs.

- The German 2s10s curve remains up almost 2bp versus Friday’s close at 74bps, but additional steepening since the cash open has now unwound.

ECB: ECB Speak Wrap (May 27 – June 2)

See here for the full publication: 250602 - Weekly ECB Speak Wrap.pdf

The ECB has entered its pre-meeting quiet period ahead of Thursday’s decision, where a 25bp cut remains unanimously expected a fully priced by markets. MNI’s preview will be out later this week.

The MNI Policy Team’s latest sources piece headlines the past week’s ECBspeak. The ECB is likely to lower its inflation projection for 2026 to 1.7% or 1.8% in its June exercise, one or two tenths below the 1.9% seen in March, Eurosystem sources told MNI, adding that there could be a pause in rate cuts after a further 25-basis-point reduction next week. Despite this downward revision, this deviation below 2% will not be considered strong enough to automatically trigger an additional rate cut beyond the June meeting, as some of the drivers of this inflation revision could reverse course given uncertainty over international trade, sources said.

- This somewhat more cautious approach once rates reach 2.00% - the middle of the ECB’s heavily caveated neutral range – will likely be strongly advocated by hawkish leaning Governing Council members. On May 28, Knot said that “a monetary policy stance that is neither accommodative nor restrictive is in my view appropriate”.

- However, there is still scope for more cuts depending on the macroeconomic data and trade outlook. Speaking to the MNI Policy Team, acting Central Bank of Malta Governor Demarco (May 27) said that “if headline inflation in the medium term is expected to remain persistently well below 2% then it is more likely that there is room for interest rates to fall below 2%”.