US TSYS: Cash Open

Aug-21 00:06

TYU5 is trading 111-26+, down 0-01 from its close.

- The US 2-year yield opens around 3.75%.

- The US 10-year yield opens around 4.295%.

- "Fed’s Cook Says She Won’t be Bullied Into Stepping Down. Federal Reserve Governor Lisa Cook signaled her intention to remain at the central bank in defiance of calls for her resignation by President Donald Trump over allegations of mortgage fraud.“I have no intention of being bullied to step down from my position because of some questions raised in a tweet,” Cook said in a statement. “I do intend to take any questions about my financial history seriously as a member of the Federal Reserve and so I am gathering the accurate information to answer any legitimate questions and provide the facts.” - BBG

- US Director Of Federal Housing Pulte on X: “Write anything you or your attorneys want Miss Cook, you’ve been caught based on mortgage documents, not a tweet. It’s black and white. We go after people who commit mortgage fraud, and you signed the mortgage documents, no one else. And you did it within 14 days of each other.”

- Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area in 10-Year yields found solid demand capping the move higher for now, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- Data/Events: Initial Jobless Claims, Phil Fed Business Outlook, S&P US PMI’s, Leading Index, Existing HOme Sales

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Q2 Exports Fall As Shipments To US Normalise

Jul-21 23:45

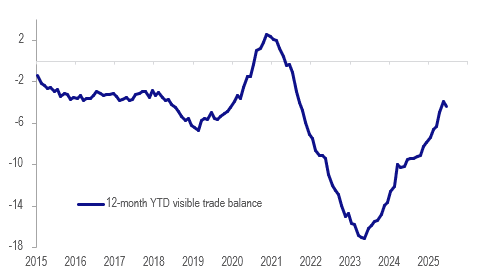

NZ posted a small merchandise trade surplus in June of $42mn, the fifth consecutive positive, after a downwardly-revised $1082mn. There was a rise in the 12-month YTD deficit to $4.37bn from $3.93bn but it is too early to say the trade improvement has stalled. Annual import growth rose sharply last month and was not as weak as exports in Q2.

NZ merchandise trade balance YTD $bn

Source: MNI - Market News/LSEG

- Statistics NZ reports that Q2 goods export values fell 3.7% q/q after rising 11% in Q1, while imports fell 0.3% q/q after -3.5%.

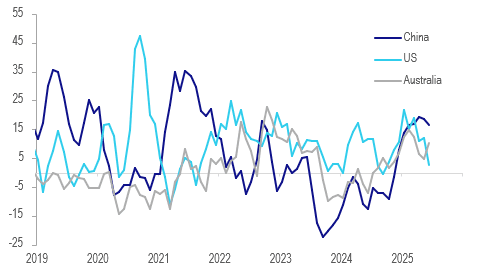

- Goods exports rose 10.2% y/y in June but were flat on the month seasonally adjusted. After peaking in March to beat US tariff deadlines, shipment levels to the US have been normalising. After rising 21.8% y/y in April, they fell 8.8% y/y in June.

- Exports to other major trading partners were generally robust rising 10.8% y/y to China, 15.5% y/y to Australia and 32.1% y/y to Europe. However, they fell 4.7% y/y to Japan.

- Higher dairy prices helped to support June exports.

- Imports rose 4.1% m/m in June bringing annual growth to 14.8% driven by a pickup in capital goods but also a 101% y/y increase in petroleum. Consumption goods rose 11.9% y/y, while plant & equipment +13.2% y/y and transport goods +18.6% y/y (there was a 436% increase in public transit vehicles).

NZ goods exports by country y/y%

Source: MNI - Market News/LSEG

JGBS: JGBS To Open After Long Weekend

Jul-21 23:42

JGBS will open for the first time today since the weekend’s elections.

- In post-Tokyo trade on Friday, JGB futures closed weaker, -31 compared to settlement levels.

- Overnight, multiple factors helped US tsys extend their rally into a 4th day. However, a survey of various desks suggested a specific catalyst couldn't really be identified, with no tier 1 data or FOMC speakers (pre-meeting blackout period) on the docket.

- A decline in oil prices helped bring breakevens lower, with reports of a potential Russia-Ukraine meeting applying downside pressure.

- Some cited reports of potential trade tension between the US and EU ahead of the White House-imposed Aug 1 deadline for a deal. This appeared to boost EGBs in early trade, and later US tsys may have benefited from a flight to quality, though the broader move couldn't quite be squared with the pickup in equities and the Euro.

- The Japanese House of Councillors Election had a roughly as-expected outcome, helping global core FI in a relief rally (though we will know more when Japanese bond markets return from holiday).

- Today, the local calendar will be empty, ahead of tomorrow’s 40-year supply.

AUSSIE BONDS: Moderately Richer With US Tsys, RBA Minutes Due

Jul-21 23:19

ACGBs (YM +1.5 & XM +2.5) are moderately stronger after US tsys finished Monday with gains.

- Multiple factors helped US tsys extend their rally into a 4th day. However, a survey of various desks suggested a specific catalyst couldn't really be identified, with no tier 1 data or FOMC speakers (pre-meeting blackout period) on the docket.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at -8bps.

- The bills strip is stronger, with pricing flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 65bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting tomorrow. Governor Bullock is speaking at the Anika Foundation lunch on Thursday. Both will be monitored for further information on what lies behind the unexpected decision to hold and the central bank's thinking following the disappointing June jobs data.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).