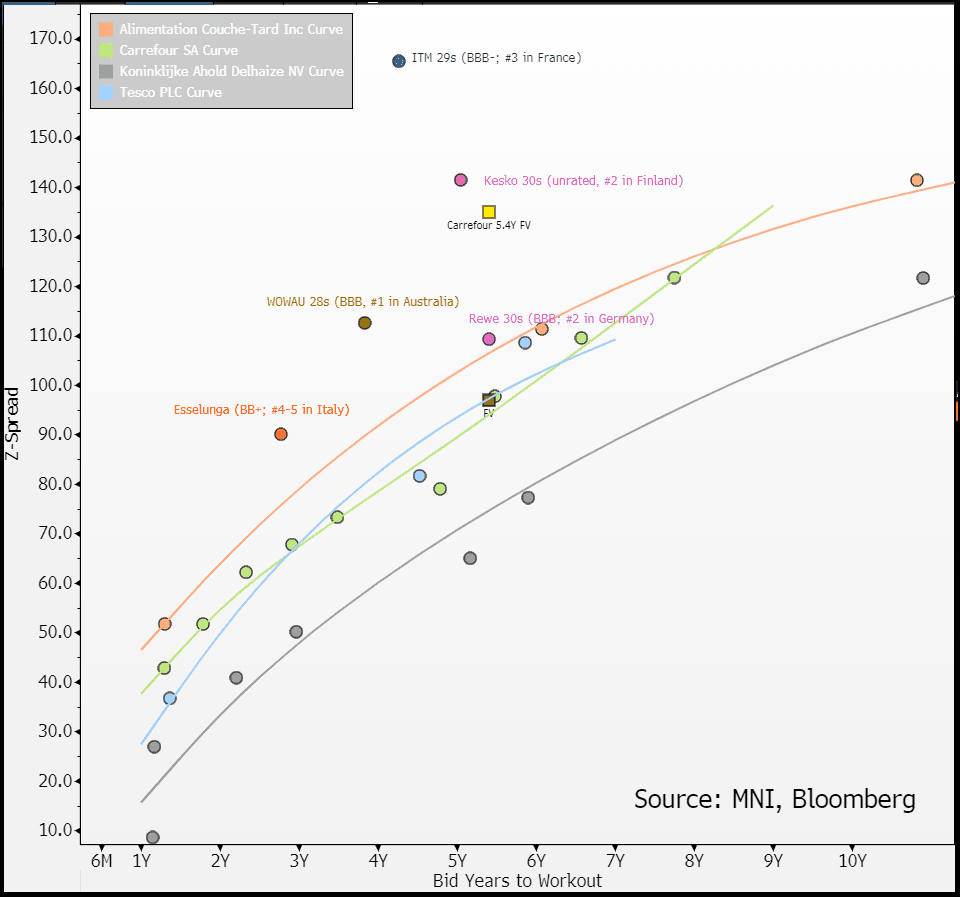

EU CONSUMER STAPLES: Carrefour; 5.4Y FV

Jan-17 10:33

(CAFP; NR/BBB)

- WNG €500m 5.4Y SLB IPT MS+135a vs. FV +97 (-38)

- FV is based on secondary. We do NOT see value at FV, rotate into Tesco 31s or REWEEG 30s for +10bps pick-up. Please note restructuring leaks below.

- FV is based on secondary. We do NOT see value at FV, rotate into Tesco 31s or REWEEG 30s for +10bps pick-up. Please note restructuring leaks below.

- Carrefour is France's 2nd largest grocer with a 22% market share (2nd to E.Leclerc at 24.4%). It is more diversified than Auchan re. store format; largest Hypermarkets are 50% of sales, supermarkets 30% and convenience stores 20%.

- France segment is only 45% of the group sales; 30% from Europe (half of this in Spain) and another 25% from LATAM (nearly entirely Brazil).

- The LATAM exposure is through a 68% stake in Carrefour Brasil but it is fully consolidated for financials. It is superior on margins contributing 40-45% of EBIT.

- Results YTD have been mixed; LATAM is doing fine while France is holding somewhat stable. Weakness YTD is Europe ex. France where EBIT has halved yoy (to a 0.7% margin). FY results come 19th of Feb

- Kantar will show market share gains in France (19.3% to start the year to 21.5% now) but this likely skewed higher by acquisition of Cora, Match & Casino stores.

- Note depreciation in Brazilian real and Argentine Peso will inflate LFL sales growth in LATAM. It seems to be managing the high-single digit (%) FX headwind fine (EBIT margins are still up in the region).

- A issue investors should be aware of is this article from Bloomberg {NSN SMHJOMT1UM0X } which leaks the company is looking at potential "asset divestments, growing through partnerships and acquisitions, or an operational reorganization".

- We assume this bond is being issued under the June 2024 Base Prospectus which has;

- no CoC

- re. sale of a "principal subsidiary" (>15% of "consolidated" sales OR >15% of consolidated assets), the Event of Default trigger through cessation of business sub-clause will not be triggered if IG ratings are maintained by S&P pro-forma. Given BBB ratings arguably this may act as protection for significant asset sales.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Under Pressure As Modest CPI Rally Gives Way

Dec-18 10:33

{GB} GILTS: Gilts fade the initial CPI-driven bid, as bearish technicals reassert themselves and oil ticks higher.

- Gilt futures through round number support at 93.00, last 92.90.

- Next support at a Fibonacci projection (92.78).

- Yields 0.5bp lower to 2bp higher, curve twist steepens.

- 30s consolidating the recent break break above 5.00%. Benchmark still ~15bp below ’23 highs, last 5.06%.

- 10s last 4.54%, November 14 high (4.566%) still untested.

- Early outperformance vs. Bunds fades, spread now only 0.5bp narrower on the day at 228.7bp. Yesterday saw the highest close for the spread since 1990.

- SONIA Dec ’25 BoE dated OIS/SFIZ5 futures operate around recent hawkish extremes with today’s inline to marginally softer-than-expected CPI data having little lasting impact, likely as the “surprises” within the data shouldn’t have too much of a bearing on monetary policy.

- BoE-dated OIS prices 55bp of cuts through ’25.

- SFIZ5 a little above triple bottom support that was printed in early to mid-November.

- Macro and cross-market cues set to dominate during the remainder of the day.

- Final ’24 BoE decision due tomorrow, click for our full preview.

ECB: Lane: Eurosystem Won't Run Scenarios On Trade Frictions Yet

Dec-18 10:22

Q: The Bundesbank last week in its forecast sketched out an impact on the German economy of a tariff scenario, which would tip it into a slight contraction. How do you see that for the Eurozone?

- Lane: This is why we made these observations in the monetary policy statement. Most of the time, it will be a downside for GDP, so we are clear on that. For inflation, there are many ancillary assumptions you have to make, so the impact is uncertain. The Bundesbank report makes a set of assumptions there.

- We have a good machine to run many scenarios, but it is not productive to work on that now. Once we have a clearer picture, we can assess the scenario in concrete and incorporate it into our assessment.

Q: In the event of increased tariffs, would the ECB welcome a depreciation in the Euro to increase competitiveness

- Lane: We will assess this on the impact it has on price stability. We take a general equilibrium view of the exchange rate. It is important to think about trade-weighted exchange rates rather than e.g. EURUSD. It matters quite a lot about how firms everywhere make pass-through decisions.

USD: AUD and NZD are extending losses

Dec-18 10:20

- AUD and the Kiwi are still the worst performers in G10s against the Dollar, and both Currencies are extending further lows, a continuation from the Overnight session into the European hours.

- While the moves aren't too fast and more of a 1 pip at a time drag, AUDUSD now look to test the next immediate hurdle at 0.6300.

- EURAUD also targets the Immediate September high situated at 1.6647, and further upside momentum will open to 1.6682.

- NZD still eye 0.5700 next, so far only managed a 0.5723 low.