EMISSIONS: Carbon Summary at European Close: EUAs, UKAs Edge Down

EUAs December 2026 are edging lower, holding just below Tuesday’s high of €88.88/ton CO2e. EUAs gradually increased in recent weeks with the anticipation of lower supplies in 2026, while the correlation with EU gas prices has weakened. UKAs Dec26 are also edging down, holding near the highest since April 2023 with optimism over the UK-EU ETS linkage.

- EUA DEC 26 down 0.4% at 88.15 EUR/MT

- UKA DEC26 down 0.6% at 67.5 GBP/MT

- NBP Gas JAN 26 up 1.1% at 73.92 GBp/therm

- TTF Gas JAN 26 up 1.1% at 28.045 EUR/MWh

- Investment funds increased net long positions in EU ETS futures on the ICE exchange for the fourth consecutive session to a new record high, according to the latest CoT data as of 19 December.

- Investment funds raised net long positions in UK ETS futures on the ICE exchange as of 19 December to the highest since late October, according to the latest COT data.

- European gas prices edge higher on Wednesday against a colder weather backdrop.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY: Moody's Upgrade Expected, Growth Outlook Key For Further Positive Action

Moody’s upgraded Italy’s credit rating to Baa2 (Outlook Stable) on Friday, in line with our expectations. Further positive ratings action is possible next year, contingent on “continued fiscal consolidation resulting from further improvements in the quality of revenue and spending” and “faster progress in addressing structural challenges related to the labour market and innovation capacity, together with stronger private investment than we currently assume”

- We’ve previously argued that growth dynamics, rather than primary balance consolidation, presents the main risk to the Italian fiscal/ratings outlook. Worse-than-expected growth outturns may limit narrowing momentum in BTP/XXX spreads in the coming years.

- Analysts expect a cyclical rebound in Italian growth, from 0.5% Y/Y in 2025 to 0.7% in 2026 and 0.9% in 2027. These are broadly in line with the EC’s latest projections (0.8% in both 2026 and 2027).

- Private consumption is expected to be supported by low unemployment rates and positive real wage growth. Meanwhile, non-residential investment growth should continue to be aided by EU RRP disbursements.

- The key cyclical questions ahead will be if middle-class tax cuts announced in the 2026 budget spur additional consumption, and whether private investment can fill the gap left by RRP funds once that programme ends.

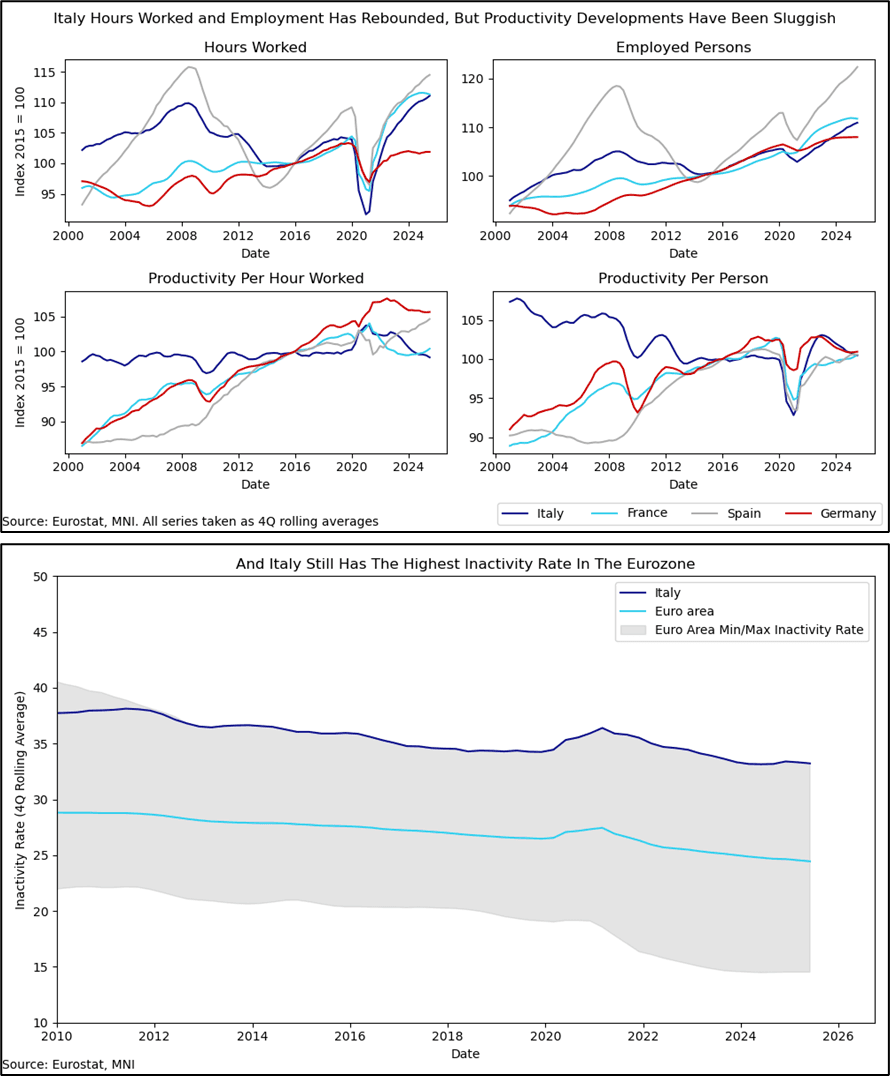

- Meanwhile, the outlook for potential output remains bleak. Although employment and hours worked have rebounded solidly post covid, sluggish growth metrics have implied poor productivity outturns. Meanwhile, Italy still has the highest inactivity rate across the Eurozone. Coupled with an ageing population, this presents a key structural headwind that government policy will need to address.

US TSY FUTURES: December'25-March'26 Roll Update

The latest December'25 to March'26 Tsy quarterly futures roll volumes are outlined below, percentage complete running at/near 50% ahead this Friday's "First Notice" date: Current roll details:

- TUZ5/TUH6 appr 159,500 from -6.25 to -5.87, -6.0 last; 50% complete

- FVZ5/FVH6 appr 259,000 from -3.0 to -2.75, -3.0 last; 52% complete

- TYZ5/TYH6 appr 222,600 from 1.5 to 2.0, 1.5 last; 49% complete

- UXYZ5/UXYH6 191,700 from 4.25 to 4.75, 4.25 last; 44% complete

- USZ5/USH6 54,200 from 11.75 to 12.75, 12.0 last; 47% complete

- WNZ5/WNH6 appr 108,300 from 9.75 to 10.25, 10.0 last; 46% complete

- Reminder, Dec'25 futures don't expire until next month: 10s, 30s and Ultras on December 19, 2s and 5s on December 31. Meanwhile, Dec'25 Tsy options expired last Friday, November 21.

US TSYS: Slow Bull Flattening; Chicago Fed U/E Rate Nowcast and 2Y Supply Ahead

Treasuries have slowly bull flattened since the late cash open after a Japan holiday, starting the Thanksgiving-trimmed week on a cautious note. Volumes are heavily boosted by the quarterly roll whilst today’s docket should see the Chicago Fed’s unemployment rate advance nowcast for November in data focus before 2Y supply later on.

- Cash yields are 0-2.5bp lower, with curves flattening away from last week’s recent steeps including 5s30s at 107.4bps off a high of 110.4bp.

- TYZ5 has edged higher to 113-09+ (+01+) overnight, holding off Friday’s latest high of 113-14. Volumes look elevated at 435k but we estimate more than half of that is roll-related.

- Last week’s gains reinforced a bullish theme with scope for a climb to 113-18+ (Oct 28 high) after which lies 113-29 (Oct 22 high). Key support to watch meanwhile is 112-06 (Sep 25 low) with first support at 112-11+ (100-dma).

- Data: Chicago Fed labor indicators Nov advance (0830ET), Dallas Fed mfg Nov (1030ET), Annual revisions to IP (1200ET)

- Fedspeak: None scheduled

- Coupon issuance: US Tsy $69B 2Y Note auction - 91282CPL9 (1300ET). Last month’s 2Y auction almost came in on the screws whilst bid-to-cover firmed from 2.51 to 2.59.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump signs Executive Order (1600ET)