JGBS: Bull-Flattener After BOJ Noguchi's Speech & Issuance Headlines

At the Tokyo lunch break, JGB futures are stronger, +20 compared to settlement levels, and at session highs.

- Headlines from BoJ Board Member Noguchi's speech have crossed. Noguchi spoke about the need to get rate hike timing rate, as hiking too early or too late can cause problems. He stated that hiking too early risks derailing the wage/price cycle and sustainably hitting the 2% inflation target, while raising rates too slowly will risk destabilizing price and activity trends (presumably as policy rates have to rise rapidly to bring down inflation).

- His comments don't give a hint on timing around rate hikes. Presumably, a Dec or Jan hike wouldn't alter the medium-term trends much from Noguchi's perspective.

- Cash US tsys are closed for the Thanksgiving Day Holiday.

- Cash JGBs are flat to 3bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 1.7bps lower at 1.792% versus the cycle high of 1.845%.

- Earlier, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance is expected to rise by around ¥100bn each for the 2-year and 5-year tenors. Reuters also noted that there are no changes to the planned issuance for 10–40-year tenors.

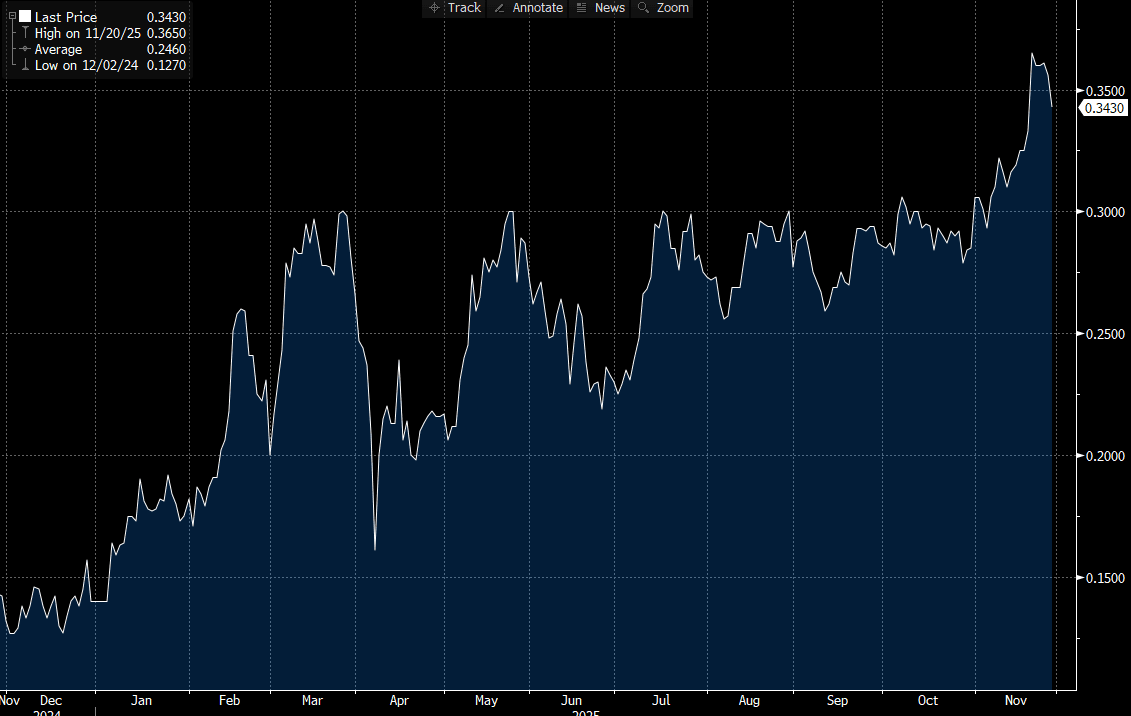

- The recent steepening of the 2/5 yield curve is consistent with today's headlines. (see chart)

- Swap rates are little changed.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: Higher Core CPI Could Drive RBA Pause In November & Await More Data

The RBA August projections had another 25bp of easing in Q4 based on market pricing. This still allowed underlying inflation to settle close to the 2.5% band mid-point over 2026. Wednesday’s Q3 CPI data will be important for how it impacts the RBA’s inflation outlook which will be key for the 4 November decision. A pause at the November meeting is likely to leave the December meeting live though. Market pricing reflects a good degree of uncertainty around November.

- The AUD OIS is currently not sure with 10bp priced in for November and 17bp by year end but this could move sharply with Q3 CPI.

- Key watch points for CPI tomorrow are as follows: Bloomberg consensus expects trimmed mean to print at 0.8% q/q & 2.7% y/y, which would see a pickup in the 2q/2q annualised rate to 2.8% from 2.6%. This outcome could argue for a hold or a cut dependent on the revised outlook and services inflation result.

- Contained services, core around 2.6-2.7% y/y or below would likely drive further easing, but even 2.8% could see another hold in November as the Board waits for more data, especially given it sees “signs that private demand is recovering”.

- Bullock said the Board was concerned about the rise in some of monthly CPI components, especially services. She noted that it has been sticky overseas and so the change in Q3 market services prices will be monitored. It moderated to 2.9% y/y in Q2 from 3.3%.

- This week Bullock reiterated that labour data are volatile and while the 0.2pp rise in the September unemployment rate to 4.5% was surprising, it could fall again in October. Thus she would like more information. The Board also looks at the 3-month averages and the Q3 unemployment rate only rose 0.1pp to 4.3% while underemployment fell 0.2pp to 5.8%.

- There are a lot of key data before the December meeting which could drive a November pause to wait and see, including surveys but also October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.

AUSTRALIA: Q3 Trimmed Mean Forecast To Stabilise At 2.7% Y/Y But Q/Q To Rise

Q3 CPI data are released 29 October and are likely to be a key input into the next RBA decision on 4 November. The focus will remain on the trimmed mean which Bloomberg consensus is forecasting to rise 0.8% q/q and remain at 2.7% y/y. In August the RBA expected it to moderate to 2.6% y/y by Q4 2025 and signs that there are upside risks to underlying inflation returning to the 2.5% band mid-point as expected may drive a prolonged pause in easing to allow more information to be gathered.

- Forecasts for Q3 underlying trimmed mean are between 0.7% and 1.0% q/q & 2.5% and 2.8% y/y. CBA and Westpac are in line with consensus while ANZ and NAB are slightly higher at 0.9% & 2.8% expecting a pickup in core inflation.

- In the Bloomberg October survey, Westpac has a Q4 2025 rate cut, while ANZ, NAB and CBA don’t expect the next move to be until H1 2026.

- Bloomberg consensus expects Q3 headline CPI to rise 1.1% q/q to be up 3.0% y/y after Q2’s 0.7% q/q & 2.1% y/y. This series continues to be distorted by government electricity rebates.

- Consensus estimates range from 0.7% to 1.0% q/q and 2.6% to 3.1% y/y with local banks CBA, NAB and Westpac all at consensus but ANZ expecting slightly higher at 1.2% q/q & 3.1%.

- September headline inflation is projected to pick up to 3.1% y/y from August’s 3.0% with forecasts between 2.9% and 3.3%. NAB and Westpac are in line with consensus, while ANZ is higher at 3.2%. Goldman Sachs expects 3.3%.

CHINA PRESS: SAFE To Promote Higher-level Opening Up

The State Administration of Foreign Exchange will introduce nine measures soon to facilitate cross-border trade, including expanding the scope of the pilot high-level opening of cross-border trade and the types of netting settlement services, Securities Daily reported citing Zhu Hexin, head of SAFE. Authorities will also coordinate the promotion of yuan internationalisation and high-quality opening of capital accounts, and deepen foreign-exchange management reforms in key areas such as direct investment, cross-border financing, and securities investment, said Zhu, noting that near-term policy introductions will also include implementing the integrated domestic and foreign currency fund pools for multinational corporations and the fund management for overseas listings of domestic enterprises.