GBPUSD TECHS: Bull Cycle Intact

- RES 4: 1.3661 High Sep 18

- RES 3: 1.3607 2.764 proj of the Nov 4 - 13 - 20 price swing

- RES 2: 1.3557 76.4% retracement of the Sep 17 - Nov 4 bear leg

- RES 1: 1.3537 High Dec 25

- PRICE: 1.3462 @ 05:45 GMT Dec 31

- SUP 1: 1.3450 Low Dec 30

- SUP 2: 1.3409/3348 20- and 50-day EMA values

- SUP 3: 1.3288 Low Dec 9

- SUP 4: 1.3180 Low Dec 2

The trend condition in GBPUSD remains bullish and recent gains reinforce current conditions. The latest pause appears to be a flag formation - a bullish continuation pattern. Note that moving average studies have recently crossed and are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.3557, a Fibonacci retracement. Firm support lies at 1.3348, the 50-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Bonds Weak; Long End Underperforming : 10-Yr Consolidates Above 4%

US bond futures were all lower today with the 10-Yr down -03 to 113-08. The 10-Yr retains its position above the 20-day EMA of 113-01+ as markets are set to start the trading week after the dis-jointed week last week due to holidays.

Cash was weak today with the long end underperforming.

- The 2-Yr is up +0.2bps at 3.496%

- The 5-Yr up +1.2bps at 3.61%

- The 10-Yr up +2.5bps at 4.044%

- The 30-Yr up +3.5bps at 4.701%

This week markets will look for any key messages from :

- Jerome H. Powell - Chair of the Fed - is slated to speak Monday at a panel discussion at Stanford.

- Michelle W. Bowman - Vice Chair for Supervision - is scheduled to give a speech this week (on bank supervision/regulation).

As the data flow continues, looking at the week ahead, the bond market will eye key data releases for potential further guidance on the upcoming rates decisions, specifically:

- Monday, December 1: ISM Manufacturing PMI, Construction Spending, and S&P Global Manufacturing PMI.

- Wednesday, December 3: ADP Employment Change, Industrial Production, Capacity Utilization, and ISM Services PMI.

- Thursday, December 4: Initial Jobless Claims and Continuing Jobless Claims.

- Friday, December 5: Personal Consumption Expenditures (PCE) price index, Personal Income, Personal Spending, and Michigan Consumer Sentiment.

For the issuance calendar overnight the focus for Monday will be Bill issuance with a 6-week maturity.

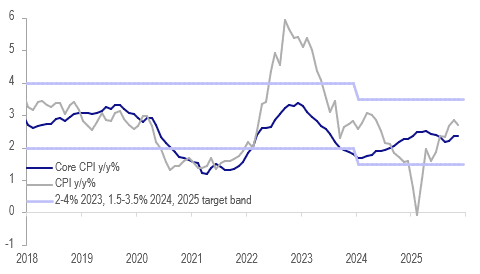

INDONESIA: BI Looking To Cut Again, Inflation Stable But Need Stronger IDR

Headline inflation moderated 0.2pp to 2.7% y/y as volatile fresh food inflation eased 1.1pp to 5.5% y/y in November. Core held steady at 2.4% y/y, which was slightly more than consensus forecast. Bank Indonesia Governor said today there is room for further easing and that it just depends on timing and the stabilisation in inflation should allow it to cut rates again when it is confident that the rupiah has stabilised.

- USDIDR is down 0.5% to 16,661 since the 19 November BI decision to keep rates unchanged but this has been helped by a weaker US dollar as Fed rate cut expectations have increased. The BIS IDR NEER was flat in November which is a step in the right direction towards FX stability.

- The S&P Global November PMI reported that cost pressures increased in Indonesia due to the weaker IDR and raw materials and were passed on resulting in highest selling inflation in more than 18 months. This is a trend that will be monitored.

- In October a large jump in personal care & others inflation to 11.9% y/y from 9.9% drove the increase in core inflation. The rise was due to higher global gold prices. They were up almost another 6% over November and so it is not surprising that personal care & others picked up further to 12.5% y/y keeping underlying inflation at 2.4%. Other components saw steady rates.

- The drop in fresh food inflation fed into lower price changes for dining out and general food & drinks components.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

ASIA STOCKS: UEDA Spooks Japanese Stocks; Korea and Taiwan Follow Suit

Global rate expectations continue to impact investor optimism with risk appetite strong in most major bourses today. Whilst US rate sensitive markets continue to position for a rate cut in the US, markets are seeing a potential BOJ rate hike in December, which has caused the yen to firm and the Nikkei to fall. Governor Kazuo Ueda has indicated the bank will consider the pros and cons of an increase. In India, stronger than expected GDP results came ahead of this week's Reserve Bank of India's decision on rates which is widely expected to see a rate cut to stem the decline in inflation. The focus on AI tech remains a key thematic with names like TSMC's fall today a key driver to the decline of the TAIEX in what local press are suggesting is profit taking. This is likely to be an ongoing theme into year end given the extraordinary run up in recent months of AI / Tech names like TSMC and key equities in Korea and Japan.

- UEDA's comments wasn't well received by the NIKKEI with it starting the month and the week off with a fall of -1.8%, dragging the KOSPI with it with falls of -0.16%.

- China's major bourses are all up with the Hang Seng leading the way with gains of +0.80%, followed by the CSI 300 up +0.75%

- The TAIEX in Taiwan is down modestly by -0.44% with risk sentiment looking less robust into year end.

- The NIFTY 50 was buoyed by the better than expected GDP and talk of a rate cut this week sees it start Monday up +0.28% to a new high of 26,278

- SE Asia' s bourses are starting the month off strongly with the FTSE Malay KLCI leading the way up +1.1% following better than expected Manufacturing PMIs.