ASIA STOCKS: Broadly Positive Day on Light Volumes

Most Asian equity bourses advanced today, driven by strong overnight performance on Wall Street and a rally in commodity prices. The US economy grew at an annualized rate of 4.3% in the third quarter—faster than expected and the fastest pace in two years—boosting investor confidence in the global economic outlook. This news pushed the S&P 500 to a new record high, setting a positive tone for Asian markets today. The US's ongoing focus on Venezuela gave oil a boost with gold, silver copper near to new highs also. Tech / AI stocks are again in focus after a positive lead in from US tech overnight. All of this came despite FED rate cut expectations being pushed out given the strength of GDP.

- The NIKKEI is up flat today on light volumes. Month to date gains remain modest as the NIKKEI at 50,475 remains near to the 20-day EMA of 50,023.

- The KOSPI also is doing very little, barely above where it started the day as focus in Korea remains on the Won and efforts to stem its ongoing weakness.

- China's major bourses are mixed with the Hang Seng up +0.17%, the CSI 300 down -0.12%, Shanghai up +0.24% and Shenzhen up +0.60% with the technology sector led the advance today, spurred by reports of potential delays in US tariffs on Chinese semiconductors, easing immediate trade tension concerns.

- The NIFTY 50 is up +0.14% in early trade, nearing 26,211 and approaching the November high of 26,215.

- SE Asia's major bourses are mixed today, on light volumes. The SE Thai has barely moved today, whilst the Jakarta Composite is down -0.15% and the FTSE Malay KLCI is up a mere +0.06%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Steady Start, Futures Near Recent Lows, All Eyes On CPI on Wed

Aussie bond futures are little changed in a quiet start to the week, with Japan markets out (and no cash US Tsy trading) impacting. 3yr (YM) was last 96.22, no change from end Friday levels. 10yr futures (XM) were at 95.54, a touch higher for the session (+1.5bps). Both benchmarks remain close to recent lows. (96.135 from Nov 13 for the 3yr, and 95.485 (Nov 20) for the 10yr.

- The main focus this week domestically will be Wednesday's inflation data. This reference period for Oct, which will be the first complete release of full month CPI. A partial basket has been published for a while but the focus remained on the quarterly series as they contained updates for all components. RBA Governor Bullock said that the Board will continue to concentrate on quarterly CPI for now as it assesses the trends in the new monthly CPI and allows time for seasonal factors to emerge for the trimmed mean.

- In the cash ACGB yield space there is some slight softness, but outside of the 10yr yield (just under 4.45%), yield losses have been under 1bps. The 3yr is around 3.74% in latest dealings.

- The 3/10s curve is slightly flatter, last near +70bps.

- The local data calendar is empty until Wednesday's inflation print.

GOLD: Gold Slightly Lower As Monitors US Economic Developments

Gold is moderately lower during today’s APAC session as the market continues to watch US developments closely ahead of the 10 December meeting. There is little information released today to change market Fed cut pricing, which rose significantly following NY Fed Williams dovish comments, but there will be important data before Thanksgiving including PPI and retail sales. The US dollar is slightly higher Monday.

- Stronger risk appetite has also pressured gold with prices down 0.3% to $4051.0/oz off the intraday low of $4040.84. Silver is flat at $50.02 after falling to $49.720.

- Bullion may also react to Ukraine-Russia developments. US, Ukraine, Europe talks continue on Monday in Switzerland. The White House said earlier today that Ukraine’s concerns with its plan have been addressed.

- Equities are generally higher with the S&P e-mini up 0.5% and Hang Seng +1.4% but CSI 300 down 0.6%. Oil prices are little changed with WTI around $58.05/bbl. Copper is down 0.2%.

- No Fed speakers are scheduled so far this week and the meeting blackout starts on 29 November. November Fed Dallas manufacturing and German November Ifo survey print later. The ECB’s Lagarde, Elderson and Cipollone speak Monday.

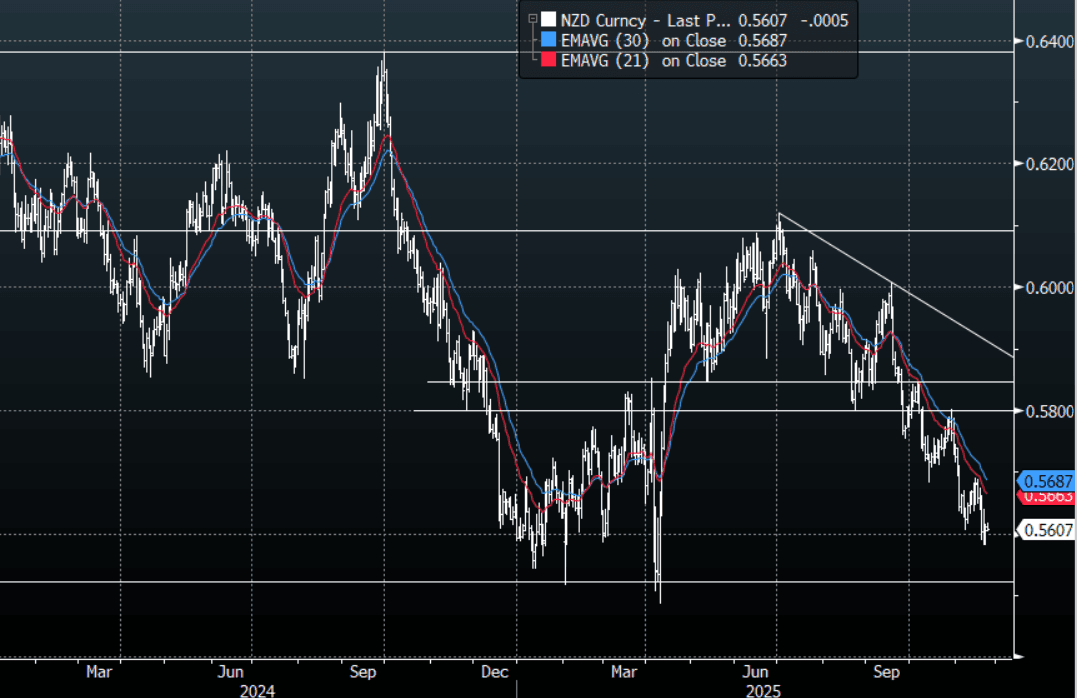

NZD: NZD/USD - Drifts Lower In A Quiet Session

The NZD/USD had a range today of 0.5603 - 0.5617 in the Asia-Pac session, going into the London open trading around 0.5610, -0.05%. The NZD/USD drifted sideways in a quiet Asian session with Japan out. Crypto has had a good bounce over the weekend indicating we might see a constructive open for risk, I would still be wary considering the price action we had last week. The NZD move lower stalled below 0.5600 and should risk build on this positive open we could potentially see it drift higher. The RBNZ this week will be important as they start to approach neutral, there is a risk the RBNZ is not dovish enough for a short market. I suspect the NZD will need global risk to come under pressure again this week to continue its move lower.

- "NZ Treasury Says Economy Yet to See Broad-based Momentum. New Zealand’s economy has yet to see broad-based momentum across sectors even as economic indicators improve, the Treasury Department says in its Fortnightly Economic Update." via BBG. NSN T67HOOKIUPSV <GO>

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5670(NZD788m Nov 26), 0.5720(NZD646m Nov 25) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P