EUROPEAN INFLATION: Broad-based Services Easing In German Final Feb HICP

Germany final February HICP inflation was 2.6 % Y/Y (vs 2.8% in Jan), two tenths below the flash release. We note that at the time of the flash prints, consensus expectations for German HICP was 2.7% Y/Y, so in effect the data has ex-post come in softer than expected. The monthly reading was revised a tenth lower on a rounded basis to 0.5% M/M.

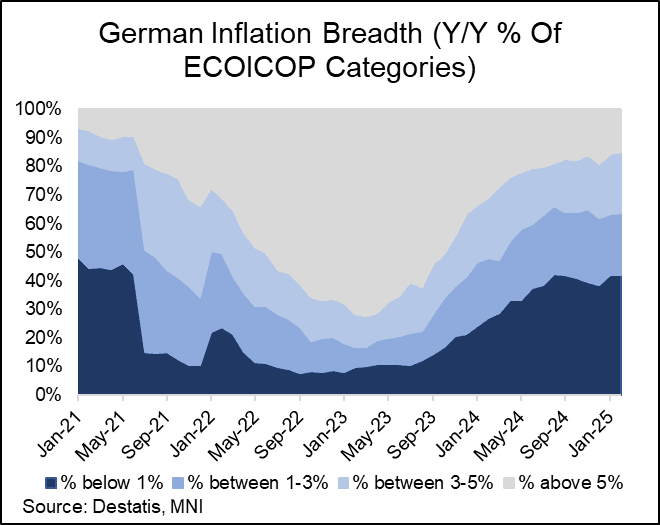

- Destatis doesn’t publish aggregate breakdowns of the HICP print (e.g. core, services, goods) in the flash or final releases (that will need to wait for the Eurostat update next week). However, looking at the component-level details, there was a broad-based easing of services components in February which will be encouraging to the ECB:

- Hospital services eased to 6.5% Y/Y (vs 7.9% prior).

- Transport services fell to 7.0% Y/Y (vs 8.2% prior), though the volatile international flights category will have contributed here (6.5% Y/Y vs 13.7% prior).

- Communication dipped to -1.5% Y/Y (vs -1.2% prior).

- Recreation and culture decelerated to 3.2% Y/Y (vs 4.4% prior) – not impacted by package holidays, which remained steady at 7.8% Y/Y.

- Restaurants and hotels fell to 4.1% Y/Y (vs 4.4% prior), driven by catering services.

- Insurance was 9.1% Y/Y (vs 9.4% in January and 15.7% in February).

- On the core goods side, clothing and footwear fell sharply to 0.4% Y/Y (vs 2.8% prior), while furnishing and household equipment was steady at -0.7% Y/Y. Medical equipment also eased.

- The proportion of HICP sub-components with annual inflation rates between 1-3% Y/Y ticked up to 21.8% (vs 21.5% prior).

- CPI inflation was in line with the flash readings at 2.3% Y/Y (2.29% unrounded vs 2.30% prior). Core CPI (excluding energy and unprocessed foods) was 2.73% Y/Y (vs 2.92% prior; flash 2.6%), driven by a deceleration in services inflation to 3.76% Y/Y (vs 3.96% prior; flash 3.8%). Goods inflation was steady at 0.88% Y/Y (vs 0.89% prior; flash 0.9%). Within the non-core components, energy CPI fell to -1.62% Y/Y (vs -1.56% prior; flash -1.8%). Meanwhile, food inflation was 2.4% Y/Y (vs 0.8% prior; flash 2.4%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 1.51bn at 1.0390/1.0405.

USDJPY 1.65bn at 153.50/153.75.

AUDUSD 1.04bn at 0.6200 (a bit far).

EURUSD 2.3bn at 1.0375/1.0400 (thu).

EURUSD 3.29bn at 1.0400 (fri).

USDJPY 1.7bn at 153.85/154.00 (fri).

AUDUSD ~1bn at 0.6300 (fri).

USDCNY 2.16bn at 7.3000 (fri).

EURUSD 1.69bn at 1.0300 (tue).

- EURUSD: 1.0300 (1.9bn), 1.0305 (209mln), 1.0325 (1.04bn), 1.0340 (754mln), 1.0350 (239mln), 1.0375 (200mln), 1.0380 (280mln), 1.0390 (318mln), 1.0400 (850mln), 1.0405 (343mln).

- GBPUSD: 1.2450 (430mln).

- USDJPY: 153.15 (531mln), 153.50 (840mln), 153.70 (589mln), 153.75 (225mln).

- AUDUSD: 0.6200 (1.04bn), 0.6300 (283mln).

- AUDNZD: 1.1100 (295mln).

BONDS: Off Lows As Oil Ticks Lower

The downtick in crude oil is probably providing some background support for core global FI markets after the initial supply-/equity-induced pressure, with major bond markets edging away from session lows in recent trade.

- Little in the way of fresh fundamental news flow to report.

- Presence of long end supply from Germany and the equity uptick leaves EGB spreads to Bunds little changed to ~1bp tighter on the day, although the long end OAT syndication, as well as Portuguese and Greek issuance is also eyed.

EURIBOR OPTIONS: Call Condor buyer

- ERM5 97.875/98.00/98.125/98.25c condor, bought for 4.75 in 2k.

Last Week saw some similar interest buying of the same Condor vs the 97.75/97.625ps, they were paying 2 for that condor vs ps structure.