US DATA: Broad-Based Jump In ISM Services Comes With Cooling Prices

Mar-04 15:28

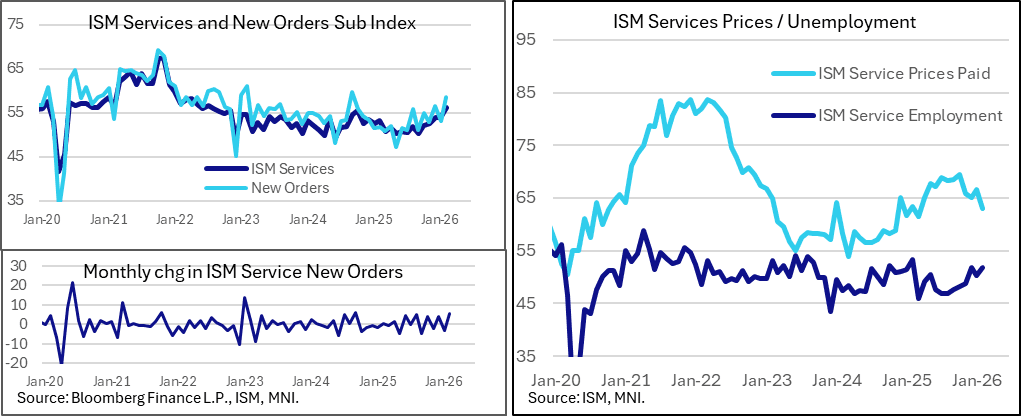

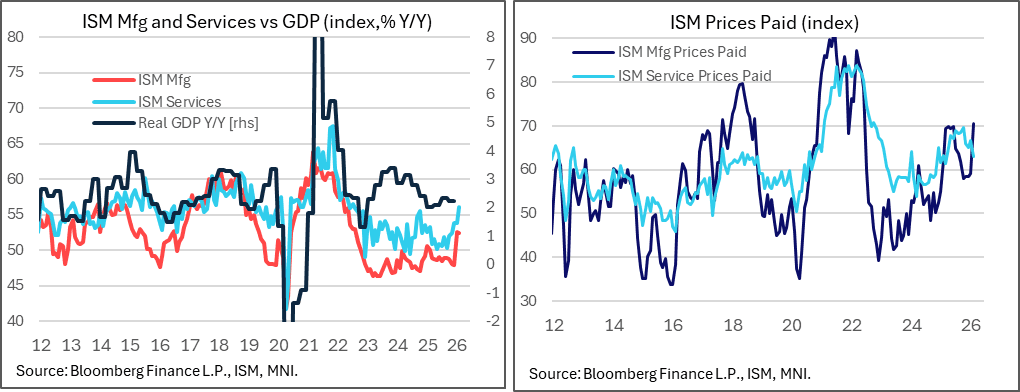

February's ISM Services report was much stronger than expected in almost all respects, with the headline PMI index rising to 56.1 (53.5 expected, 53.8 prior) for the best reading since July 2022. Combined with a positive Manufacturing reading for a second consecutive month (52.4, as reported earlier this week), the ISM reports are starting off 2026 signaling an acceleration in economic activity.

- While the details underlying the PMI index were anticipated to be solid despite an overall anticipated downtick, the subindices still managed to easily impress.

- New Orders jumped 5.5 points to a 17-month best 58.6 (53.5 expected), with Employment rising 1.5 points to a 12-month high 51.8 (50.6 expected). The Business Activity gauge rose 2.5 points to 59.9 for a 21-month high. The Supplier Deliveries index was the one component of the PMI that saw a pullback, dropping 0.3 points to 53.9, indicating less-slow deliveries.

- All that said, the data also impressed in terms of breadth. The report notes this is the 3rd consecutive month in which all of those 4 PMI subindices rose, and even more impressively, all 10 subindices were in positive territory for the first time since March 2021.

- And the report nots, "Fourteen industries reported growth in February, three more than in January, and the number reporting contraction shrank to three. "

- Also heartening was that the Prices Paid gauge fell 3.6 points to 63.0, defying expectations for a 1.7 point rise to 68.3 for an 11-month low (though a diminishment had been flagged by regional Fed surveys)..

- Confusingly this was the exact opposite signal to that sent from the ISM Manufacturing report earlier in the week, which saw an 11.5 point jump to 70.5 for the highest since Jun 2022, even before the Middle East conflict pushed up energy prices.

- Elsewhere, Backlog of Orders expanded for the first time since February 2025 (55.9, up 11.9 points) with New Export Orders and Imports also back in expansionary territory (respectively: 57.2, up 12.2 / 51.8, up 3.6). Inventories jumped 11.3 points to 56.4 with Inventory Sentiment up 1.0 to 55.3.

- The anecdotes were slightly more cautionary than the effusive data though we took note of the sector's reported adaptation to tariff uncertainty: "Commentary on trade uncertainty increased, with respondents commenting that tariffs impacts have stabilized and are now embedded in supply chain costs. Although there were several comments on tariff uncertainty regarding the U.S. Supreme Court decision, there was no alarm regarding supply chain performance, suggesting that services companies have developed capabilities to routinely address shifts in tariff policies."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Large Apr'26 2Y Call Buy

Feb-02 15:26

- +36,000 TUJ6 106.37 calls, 0.5 ref 104-07.5

US TSY FUTURES: BLOCK: Mar'26 30Y Ultra Pre-Data Sale

Feb-02 15:06

- -1,500 WNH6 117-06, sell through 117-07 post time bid at 0957:00ET, DV01 $271,700.

- The Ultra-Bond contract trades 116-30 last (-16)

US TSYS: Post-ISM React

Feb-02 15:02

- Treasuries retreat, extend lows after higher than expected ISM data.

- TYH6 currently -7 at 111-19.5 (111-19.5 low / 112-02 high). Curves flatter: 2s10s -.889 at 70.008; 5s30s -1.892 at 106.377.

- Cross-asset update: Bbg US$ index firmer (BBDXY +3.26 at 1191.55), stocks firmer (SPX eminis +13.0 at 6979.0).