BRAZIL: BRL Buoyed By Hawkish Copom, As Near-Term Rate Cut Prospects Fade

Dec-11 13:59

- Last night’s hawkish lean by the BCB and today's firmer-than-expected retail sales has provided some support to the BRL on Thursday, as expected, with USDBRL dipping 0.8% in early trade. Despite the move, the pair remains more than 2% above levels prior to Flavio Bolsonaro’s election announcement last week. After rising sharply following the announcement, long-end DI swap rates have also edged lower today, despite the hawkish tone from the BCB last night.

- As noted, there was little change to the Copom’s forward guidance, which reiterated a willingness to resume rate hikes, if necessary. As a result, a rate cut as soon as the January meeting looks unlikely at this juncture. However, the BCB is still expected to start an easing cycle later in the quarter, perhaps with a 50bp cut, given the continued decline of inflation. The hawkish stance should help to anchor the BRL for now, although continued political and fiscal concerns will still provide a headwind.

- Despite the jump in volatility over the past week, BBVA notes that it remains low on a historical basis and further weakening may be needed to fully derail the BRL carry trade and trigger even larger unwinds. At this stage, they believe the first recalibration of BRL weakness after Flavio Bolsonaro’s candidacy is close to done, but more meaningful rebounds to recent highs are also less likely.

- For USDBRL, key resistance is 5.5214, the Oct 10 high, a break of which would open 5.60, an important medium-term pivot for the pair. Key support remains at 5.2638, the Nov 11 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

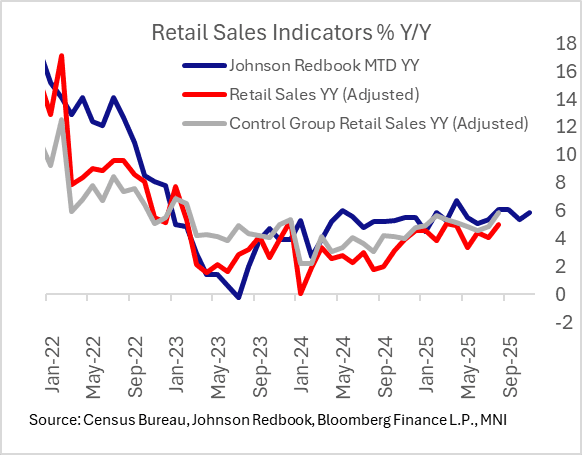

US DATA: Redbook Retail Sales Maintain Solid Pace In Early November

Nov-11 13:57

Retail sales rose 5.9% Y/Y in the first week of November (to Nov 8), per the latest Johnson Redbook Retail Sales Index release. It's still early in the month but that's a slight uptick from 5.4% in October.

- We almost certainly won't be getting October retail sales data out as scheduled Friday (we still await the September report which was postponed due to the government shutdown). Between Chicago Fed CARTS (final est for Oct due out Thursday) and Redbook, though, it appears as though retail sales were broadly solid in October at least in nominal terms.

- That said, between politics and persistent inflation, consumer sentiment was subdued in the latest week, per the report: "Business was slow as people focused on the election, which is a common trend. Additionally, the federal government shutdown is creating challenges for some families. Persistent inflation and tariffs are also having a negative impact on the economy. November marks the official start of the holiday season, which begins in the last week of the month. This period serves as a transition for retailers, who take the opportunity to clear unsold merchandise and prepare for the holiday rush. While some stores are starting to promote holiday items earlier than usual, others may not be fully stocked until the day after Thanksgiving."

MNI: US REDBOOK: NOV STORE SALES +5.9% V YR AGO MO

Nov-11 13:55

- MNI: US REDBOOK: NOV STORE SALES +5.9% V YR AGO MO

- US REDBOOK: STORE SALES +5.9% WK ENDED NOV 08 V YR AGO WK

US TSYS: Early SOFR/Treasury Option Roundup: Post-ADP SOFR Calls

Nov-11 13:53

SOFR options saw better downside put trade prior to the release of weekly ADP employ data - turning to upside calls (Treasury option volumes rather modest so far). Underlying futures extended highs after the ADP showed a decline in jobs (TYZ5 +9 at 112-31), while projected rate cut gains vs late Monday levels (*): Dec'25 at -17.1bp (-15.5bp), Jan'26 at -27.9bp (-25.1bp), Mar'26 at -38.1bp (-35.2bp), Apr'26 at -44.9bp (-41.3bp).

- SOFR Options: (Note Nov options expire Friday)

- +20,000 SFRF6 96.62/96.75/97.00 2x3x1 call flys, 2.25-2.5 vs. 96.435/0.09%

- -3,000 SFRX5 96.50 calls, 1.5 ref 96.25

- +4,000 SFRZ5 96.43/96.50, 0.5 vs. 96.28/0.05%

- Block, +5,000 0QH6 96.25/96.50 put spds, 3.5 ref 96.895

- 1,300 SFRX5 96.18/96.25 box

- Block, -10,000 SFRZ5 96.50/96.62 call spds, 0.25

- Block/screen, 4,000 SFRG6 96.68/96.81/96.87/97.00 call condors, 0.75

- 4,000 SFRZ5 96.37/96.56 call spds vs. SFRF6 96.56/96.75 call spds, 2.5 net/Jan bought over

- +4,000 SFRZ6 96.12/96.50/96.75 broken put flys, 2.5

- -2,000 SFRX5 96.18/96.31 strangles, 0.5

- 9,350 SFRX 96.18 puts, .25-0.50 total volume over 17,500

- over 8,300 SFRX5 96.25 puts

- -6,500 SFRZ5 96.43/96.68 call spds, 0.25-0.50

- Treasury Options:

- 2,000 TYZ5 111.5/112 put spds, 1

- -3,500 TYZ5 112.75 calls, 24 vs. 112-23.5/0.47%

- +2,500 Wednesday weekly TY 112.5 puts, 1 vs. 112-26/0.28%

- +2,500 Wednesday weekly TY 112.75 calls, 21 vs. 112-24/0.45%