EM LATAM CREDIT: Braskem: S&P Downgrade to B+, O/L Neg - Negative

(BRASKM; B2neg/B+Neg/BB-*-)

Concerns about cash burn persisted at the rating agency, leading to a downgrade of the rating to a level more commensurate with their expectations of continued very high leverage.

We expect some sort of corporate restructuring involving Petrobras as there are synergies that can be exploited with the govt-controlled energy company who already has a 47% stake and would like a much larger say in decision making at the chemical company. Higher EBITDA from better management over time should lead to better leverage.

There is also the potential for govt tax breaks that could aid Braskem. Meanwhile, we agree that the ratings move makes sense given the persistent negative cash flow and very high leverage.

S&P mentioned the benefits of possible anti-dumping legislation which could be supportive for profit margins but still believed it would not be enough to bring leverage below 7x debt to EBITDA for 2025 and 2026.

Refinancing risk was also noted as negative free cash flow eats away at liquidity over time, though not a near term concern with low short-term debt maturities.

S&P addressed Braskem's Mexico JV with Idesa as well, saying that since the bonds of Braskem Idesa (BAKIDE; NR/CCC*-/CCC+) were non-recourse to Braskem the ratings are not linked. The company announced it had hired advisors for a potential debt restructuring for BAKIDE and S&P does not expect Braskem to contribute any cash to the JV.

BRASKM 34s were last quoted 65.53, down .16 today and down 14 points since June 30th.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

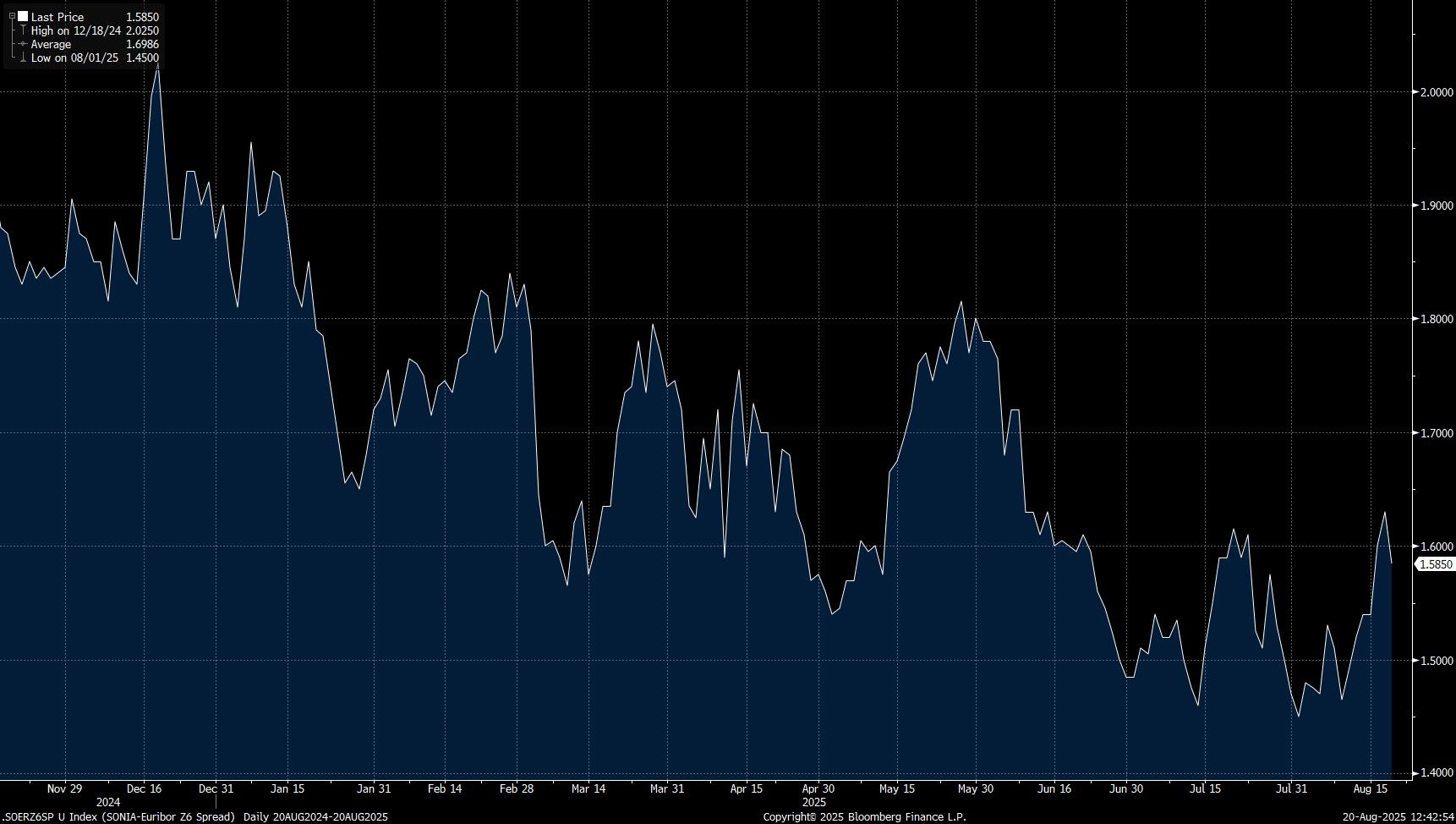

STIR: SONIA/Euribor Dec '26 Spread Away From Multi-Week Highs

Dovish ’26 BoE pricing moves have pulled the SONIA/Euribor Dec ’26 (Z6) spread off yesterday’s multi-week closing highs.

- We suggested that the data wasn’t much of a gamechanger for near-term BoE meeting pricing in the immediate aftermath of the release and that seems to have played out, with the initial hawkish reaction in the front contracts countered.

- The recent run of UK data had resulted in ~18bp of spread widening since August 1, as of yesterday’s close.

- The spread is mainly being driven by the UK leg, with Euribor pricing more stagnant since the July ECB decision.

- The main development since the ECB's July decision has been the EU-U.S. trade agreement. While the agreement reduced near-term trade policy uncertainty, the level of tariffs is more onerous than assumed in the ECB's baseline scenario.

- That said, ECB President Lagarde noted this morning that the agreement is "well below" the June MPR projection severe scenario". How the agreement is incorporated into the September forecast round will be a key focus as we move forwards.

- A reminder that the ECB adopted a less dovish round of rhetoric after its most recent cut.

- Euribor futures start to price chances of a hiking cycle in H226, after leaning towards one further cut in the current cycle.

Fig. 1: SONIA/Euribor Dec’26 Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

STIR: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.33% (-0.01), volume: $2.760T

- Broad General Collateral Rate (BGCR): 4.31% (-0.02), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.31% (-0.02), volume: $1.118T

- (rate, volume levels reflect prior session)

US TSY FUTURES: September'25-December'25 Roll Update

Latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Pace is rising slowly ahead the "First Notice" date on August 29. Current roll details:

- TUU5/TUZ5 appr 88,900 from -8.12 to -7.88, -8.0 last; 6% complete

- FVU5/FVZ5 appr 32,700 from -5.0 to -4.5, -4.75 last; 10% complete

- TYU5/TYZ5 appr 28,700 from -0.5 to +0.0, -0.25 last; 5% complete

- UXYU5/UXYZ5 under 6,900 from 0.5 to 1.0, 0.5 last; 3% complete

- USU5/USZ5 appr 500 from 13.25 to 13.75, 13.25 last; 8% complete

- WNU5/WNZ5 appr 3,600 from 8.0 to 8.5, 8.25 last; 4% complete

- Reminder, Sep futures don't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30. Meanwhile, Sep'25 Tsy options will expire this Friday, August 22.