EM LATAM CREDIT: Braskem: Revolver Loan Creditors - Neutral

Oct-31 19:27

(Caa3neg/CCC-neg/CCC+)

" A group of banks is hiring FTI Consulting Inc as an adviser amid concerns that Braskem SA’s debt talks will affect payments on a revolver loan " - Bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Taking Delayed/Suspended Data In Stride As Shutdown Gets Underway

Oct-01 19:25

- Treasuries look to finish higher - off first half highs after September's ISM Manufacturing Report showed a slight if uneven improvement in sectoral activity. Rates initially gapped higher after much lower than estimated private ADP employment numbers.

- The ADP release for September was weak, showing the biggest private payrolls drop (-32k) since March 2023 and before that, Jun 2020. And the prior 54k was revised down to -3k, so the first back-to-back drops since the pandemic. This was a significant miss for private payrolls versus +51k expected.

- ADP was re-benchmarked, however, resulting in a reduction of 43,000 jobs in September compared to pre-benchmarked data. The trend was unchanged; job creation continued to lose momentum across most sectors."

- Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- Thursday's scheduled economic data largely delayed/suspended due to the shutdown - weekly jobless/continuing claims as well as Factory New Orders will not be released

- In other news: Supreme Court rejects Pres Trump's firing of Fed Gov Cook - until at least an oral argument on the case is heard in January 2026. VP Vance expects federal layoffs to start in the next one to two days.

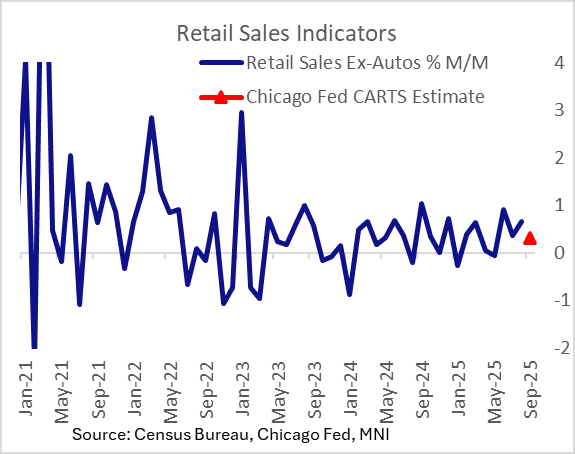

US DATA: Chicago Fed Eyes Solid Ex-Auto September Retail Sales

Oct-01 19:23

The Chicago Fed's Advance Retail Trade Summary (CARTS)'s preliminary estimate for September Retail sales ex-auto is 0.3% M/M.

- Coming after 0.7% M/M gains in this retail sales aggregate in August, this would be a 3-month low, but still suggest that underlying strength remains after a strong few months: it would translate into 6.1% 3M/3M annualized growth for this category, the fastest since November 2023.

- There is not yet consensus for the September retail sales report and not even certainty we will get one on Oct 16 as scheduled from the Census Bureau given the federal government shutdown, but so far the indicators for September (including Redbook same-store sales) have pointed to relatively solid dynamics in the month.

- The final CARTS estimate is published on Oct 15.

- One last major piece of the puzzle is auto sales, for which we should get data from Wards Automotive later on Wednesday.

US TSYS: Late SOFR/Treasury Option Roundup: Better Calls on Net, Rate Cuts Rise

Oct-01 19:01

Better SOFR/Treasury call volumes on net Wednesday, some notable put spreads as well (+60k SFRZ5 96.06/96.12 put spd). Underlying futures climbing again after paring back from late morning highs. Projected rate cut pricing gaining vs. late Tuesday levels (*): Oct'25 at -25.3bp (-24.2bp), Dec'25 at -46.9bp (-44.2bp), Jan'26 at -58.8bp (-53.7bp), Mar'26 at -70.0bp (-64.7bp).

- SOFR Options:

- Block, 8,000 0QZ5 97.12/97.50 call spds vs. 3QZ5 96.87/97.25 call spd, 1.5 net - conditional curve steepener

- Block, 2,500 0QZ5 97.00/97.25 2x5 call spds, 3.5 net

- +10,000 0QZ5 96.25/96.56 2x1 put spds, 1.0 ref 96.955

- -6,000 0QZ5 96.37/96.62 2x1 put spds, 1.0 ref 96.955

- Block, 5,000 SFRZ5 96.56/96.68 call spds, 1.25 ref 96.355

- 3,000 SFRZ5 96.25/96.31/96.50/96.56 call condors

- 5,000 SFRH6 96.37/96.50 2x1 put spds ref 96.56

- over 7,400 SFRV5 96.43 calls, ref 96.355

- -7,000 SFRZ5 95.93/96.06/96.18/96.31 call condors, 3.25

- Block, 6,250 SFRZ5 96.50 calls, 3.75 ref 96.36

- over +59,000 SFRZ5 96.06/96.12 put spds, 0.75 ref 96.32/0.05%

- 3,800 SFRG6 96.75 calls ref 96.515

- +2,500 0QX5 96.75 puts, 5.0 vs. 96.92/0.29%

- +1,500 SFRZ5 96.25/96.37/96.50 call flys, 4.75 vs. 96.33/0.08%

- -1,500 0QZ5 96.87 straddles, 30.5

- +2,000 SFRZ5 96.25/96.31/96.50/96.56 call condors, 3.5 vs. 96.325/0.07%

- 5,200 SFRH6 96.12/96.25/96.50/96.75 call condors

- Treasury Options:

- 6,500 TUZ5 103.87/104.37/104.50/104.87 broken put flys ref 104-09.62

- 5,700 TYX5 112.5/TYZ5 112 put spds

- 2,500 TUX5 103.87/104.12 put spd vs. 104.5 calls ref 104-08.75

- 1,400 TYZ5 113 straddles, 1-47 ref 112-21

- 2,500 TYX5 112.75 straddles, 1-07 ref 112-21.5

- 1,200 FVZ5 109.25 straddles, 1-19 ref 109-11.5

- over 11,900 FVX5 109 puts, 12.5 ref 112-26

- 10,000 Wed wkly TU 104.37 calls, .5 (exp today)

- over 5,000 TYZ5 113/113.5/114 call trees (total volumes: 113 call over 9.3k, 114 call over 13.7k. Note: yesterday's continuation of low delta call buying: over 186k TYZ5 113 calls, OI +133,664; over 65.3k TYZ5 113.5 calls, OI +22,147; over 108k TYZ5 114 calls, OI +20,739)

- +2,000 TYX5 114/TYZ 114.5 call diagonal, 9 net/Dec over

- 2,000 TYX 114/114.5 call spds ref 112-20

- 5,500 FVX5 109.75 calls, 11 ref 109-07.25

- 5,500 TYX5 113 calls, 24 ref 112-16

- +1,500 TYZ5 113/114/115 call flys, 8 vs. 112-10/0.05%

- -2,000 FVX5 108/109 put spds, 14.5 vs. 109-08.25/0.08%

- 2,500 Wed wkly 112.75 calls, 2 ref 112-16 (expire today)