EM LATAM CREDIT: Braskem: Petrobras Contracts - Positive

Dec-19 17:55

(BRASKM; Caa3neg/CCC-neg/CCC+)

"Petrobras Signs New Long-Term Contracts With Braskem" - Bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: Preview 20Y Bond Auction

Nov-19 17:54

Tsy futures remain modestly firmer (TYZ5 +1 at 112-26 vs. 112-23 low) ahead of the $16B 20Y bond auction (912810UQ9) at 1300ET, WI is currently at 4.705%, 19.9bp cheap to last month's stop.

- October auction recap: Treasury futures gain slightly (TYZ5 113-24 +0.0) after $13B 20Y Bond auction re-open (912810UN6) stopped through - drawing a high yield of 4.506% vs 4.517% WI at the cutoff; 2.73x bid-to-cover vs. 2.74x prior.

- Peripheral stats: indirect take-up dips to 63.63% vs. 64.6% prior; direct bidder take-up 26.33% from 27.9% prior; primary dealer take-up rises to 10.04% vs. 7.5% prior.

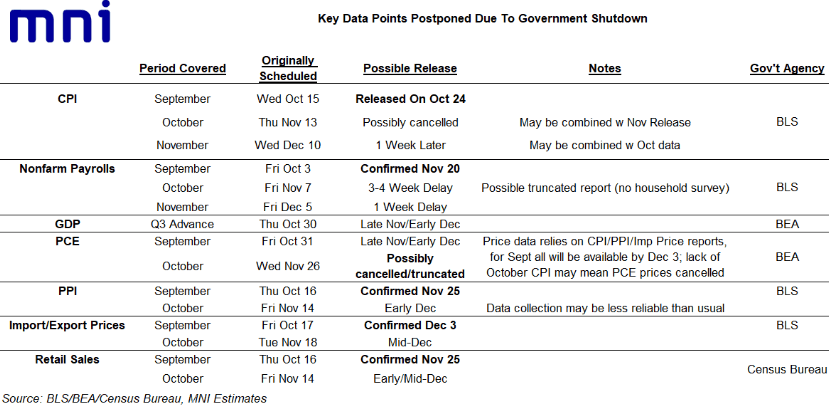

US DATA: The Latest Payrolls Data The FOMC Will See Is Tomorrow’s Sept Release

Nov-19 17:53

- Adding to the above on payrolls report scheduling, the decision to not publish the establishment survey figures for October until November’s release is a surprise to us.

- Whilst we have for a while seen a good chance there wouldn’t be a household survey release, subsequently supported by NEC’s Hassett, we had assumed the establishment figures would at least still be published to give the Fed better clarity at least on the jobs/hours/earnings side of the labor market.

- Further, our table, which we updated less than two hours ago, had pencilled in a one-week delay to the November report from its original publication date of Dec 5. This newly planned Dec 16 publication then takes it past the FOMC meeting on Dec 9-10.

- Combined, it leaves tomorrow’s delayed September report, which for avoidance of doubt will be published in full having been collected prior to the shutdown, as the last BLS payrolls report that the Fed will see before its next meeting (hence the sharp sell-off in front rates with various FOMC participants talking on the need for caution amidst data fog).

- If there’s one positive it’s that a longer collection period for November payrolls and household survey figures (per the BLS notice), should at least mean less scope for subsequent two-month revisions, but it’s a small positive.

- That’s something Fed Governor Waller discussed in Q&A on Monday: “It's not clear we're ever going to get a third revision or second revision to the September report. We might get some truncated first revision. Probably not going to get a second revision. First, the October report. We're not exactly sure what it's going to look like. How much was recorded? How much did we have? Are we going to get a second and third or a first revision second out of that data? I don't know. So that's going to be the tricky thing is without any revisions to the data, we don't really have a good idea of how accurate these numbers are going to be.”

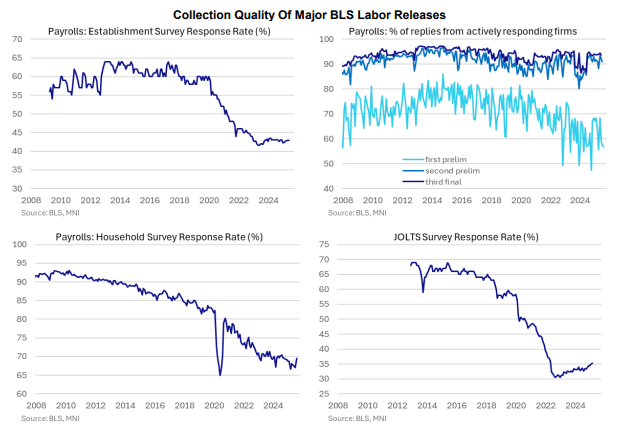

- We most recently touched on the low response rates in our methodology cheat sheet, here - see charts below.

OPTIONS: Notable Upside In Euribor For The Most Part

Nov-19 17:52

Wednesday's Europe rates/bond options flow included:

- DUZ5 107.10c, sold at 0.75 in 5.8k

- OEF6 117/118/119.5 call ladder sold at 24.75 in 2k (vs 02s (-1))

- RXZ5 129.00/128.50/128.00p ladder, sold at 22 in 3k

- RXF6 129/128/127p fly, bought for 20 in 3k.

- RXH6 132.50/134.00cs, bought for 12.5 in 2k

- ERM6 98.75/99.00/99.25c fly, bought for 0.25 in 7k

- ERU6 98.31/98.43cs, bought for 2 in 10k

- ERU6 98.12/98.25cs vs 97.87/97.75ps, bought the cs for 1 in 6k

- SFIZ5 96.30/96.15/96.05p fly, sold at 3 in 7.5k

- SFIZ5 96.25p, sold at 2.5 in 2k

- SFIH6 96.50/96.60/96.80broken c fly, bought for 1.25 in 3k

- SFIM6 96.70c vs SFIH6 96.55c, sold the June at 4.25 in 5k